I’ve moved back to NYC! To be more specific, the suburbs of NYC — but I think that still counts!

When Liza and I found out early last year that we were expecting a girl we knew we would have to make a decision about staying in the Bay Area or moving back east. After a bunch of conversations, we made the move in late February and have been settling in much more smoothly than I had expected.

With some time now to reflect, I’ve been thinking a ton about the differences between the two cities. For reference, I spent ~6 years in NYC (Brooklyn and Manhattan) and then ~6 years in SF. So I feel like I can credibly claim to have somewhat of a balanced view on the “great debate” of which is better. Unsurprisingly, as with many things, the truth is…it depends.

Much has been written of course about the demise of SF — homelessness, drug abuse, crime, commercial vacancies, etc. All of this is true and all of it quite sad. Each year I was in SF was more or less worse than the prior year, accelerated by the pandemic in a way that was hard to fathom at the time. But since I left, and have had some space to reflect, I find myself rooting for SF to make a comeback. And I think it will. The reality is, even now, there is no place on earth that has done more to advance technology and innovation than that ~50 miles between San Jose and the Golden Gate bridge. The talent network effects there run deep. The “builder mindset” second to none. And there are enough people still there who deeply care about the city and bringing it back to where it ought to be.

When I first started in venture in 2017 in SF, it was pretty common to take every first meeting with a founder in person. Some of my fondest memories of SF come from the hours spent walking all over Jackson Square, SOMA, FiDi and South Park between meetings to unearth opportunities. Back then the entrepreneurial community was so incredibly concentrated in a few of these neighborhoods that you could meet 50–75% of founders within a 20 min walk of Market St. There was something quaint, almost familial about the whole thing.

Of course the pandemic and ensuing years have broadened access beyond the Bay Area. And that is a very good thing as innovation should never be isolated to one area nor founders unable to access capital and resources purely based on where they live. Still, there is something very special about SF…not to mention it’s a city of immense natural beauty.

Everyone I know who left SF the last few years did so largely for “push” reasons. For us, there was certainly some of that. But deciding to move back to the NYC area had much more to do with personal “pull factors” than anything else: it’s the center of gravity for my wife’s side of the family (hooray for free child care!), the schools here are excellent, we’ve found there to be a strong sense of community, etc. And much of this is simply a stage of life thing. Having a child changed our outlook, including what we started to optimize for on location.

I’ve now been back in NYC for a little over 2 months. It’s been fun re-acclimating. As a fintech-focused investor, NYC is very clearly emerging as THE winner in financial services innovation. It’s not bigger than SF just yet in terms of outcomes, but the slope of the line, as defined by fintech startup formation and pace of growth, is incredibly steep.

When I first moved here more than 10 years ago, there was effectively one fintech company in the city that had some buzz: Betterment. There are now dozens of other examples and more forming each month. Many fintech founders are relocating from SF to NYC (or opening up a second office here). This week there are 3 major fintech-related conferences happening at the same time. It’s pretty wild.

Suffice to say I’m excited to get plugged back in here, reconnect with some old friends and make a few new ones. Looking forward to saying “hi” if you’re in the area.

As we head into the home stretch of ’22, startups around the world are beginning to build their budgets for next year. Top of mind for everyone right now, of course, is what will ’23 bring in terms of interest rates, capital markets and broader macro conditions. Nearly every Board will be pushing their founders to focus on efficient growth — where burn and runway are just as important as top-line growth.

Creating the top-line goal is the easy part. If you are a Series A or Series B B2B startup, you probably are shooting for something like 2–3x yoy growth. But it’s the supporting budget to attain that plan (and ensuing investments in OPEX) that is the real challenge to map out. Overspend and you could find yourself in a troubling cash position; in an environment punishing to high burn businesses no less.

I work mostly in fintech where transactional businesses models (e.g. payments, lending, last-mile logistics, etc) are common. If you are a founder with a transactional model, budgeting for next year will be even more tricky than what your SaaS peers have to do in their planning process for ‘23.

This post will explore why that is and what you can do about it. TLDR, if you want to skip over the why part and just go directly to the recommendations, here they are:

Build in monthly minimums where you can

Understand your customer ramp process

Allocate product and engineering resources to reducing costs

Hone your demand forecasting

Budget carefully with clear stage gates and monthly check points

Downplay months where you beat and sweat months you miss

Be strategic about the timing of your next round

Consider extending runway with alternatives to equity (but proceed with caution)

Implications of a Transactional Business Model

Transactional businesses have a variety of nuances that make them more challenging to budget for vs a business with a SaaS model. The first, and most obvious difference, is that planning out the top-line on a month-to-month basis for the transactional business is inherently harder.

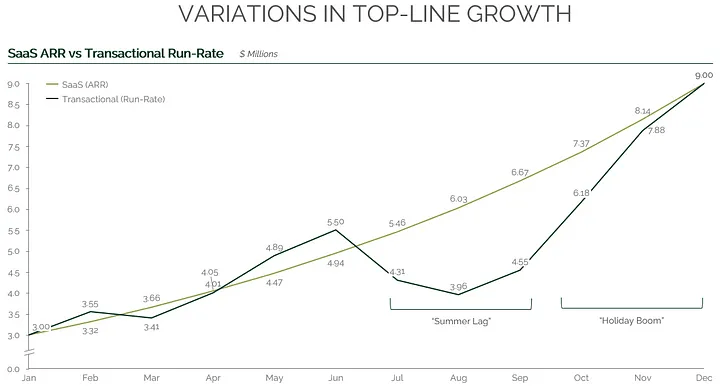

Let’s take two growth-stage Series B companies that want to 3x growth from ’22 to ’23. The SaaS business wants to go from 3M of ARR to 9M of ARR and the transactional business wants to go from 3M of revenue run-rate to 9M of revenue run-rate — enviable growth for any Series B company! (Please note there is a key distinction between “ARR” and “run rate,” see here.) The ’23 top-line plans of the two businesses could well look something like this:

Both companies go from 3M to 9M but getting there is quite different. The monthly growth for the SaaS business is mostly “smooth” and predictable. If the business is working, there can be a high degree of precision to monthly and quarterly forecasting. Every month net new ARR is added to the existing ARR base and the company scales as a function of more marketing and sales resourcing.

The transactional business is a bit “choppier” and a lot less predictable, as every month is, in a sense, completely unknown. The transactional business can’t necessarily bank on last month’s revenue (it’s not contractually recurring), in order to continue growth. There is also usually some form of seasonality with transactional businesses. In the payments/ ecommerce world, for example, that seasonality takes the form of a summer slowdown followed by a holiday boom.

Next, let’s look at the impact of the two models on burn and runway assuming both companies started with a similar starting cash position ($30M on Dec 31st ’22) and have the same OPEX budget plan (ie they plan to spend the same amount on hiring, G&A, etc.)

By the end of the year, the ending cash position of the transactional business is $2M less and the business has 5 months less of runway!

In this example, there are two reasons why the transactional business ends the year with 5 months less of runway, despite the two businesses budgeting for the same OPEX spend and achieving the same top-line goal:

1) The SaaS business will generate $0.5M more in GaaP revenue for ’23 than the transactional business (+10% more). This is mostly a result of the seasonal dip in Q3. Note that even though the transactional business has a faster growth rate in Q4, it generates 6% less revenue than the SaaS business in that quarter (“deeper hole to dig back from.”)

2) The SaaS business will generate $2M more of gross profit (+43% more). The transactional business has lower gross margins than the SaaS business. In this example, we have assumed typical 80% gross margins for the SaaS business vs 50% for the transactional business — transactional businesses almost always have higher COGS than SaaS businesses (e.g. processing fees, cost of capital, delivery costs, etc.)

The two points above mean the transactional business has fewer real dollars coming in than the SaaS business to offset the same amount of OPEX. Ceteris paribus, transactional business will almost always burn more than SaaS businesses.

The other challenge for the transactional business, as a result of the top-line volatility, is that the monthly burn is also much more variable. Continuing with our example, for the SaaS business, the OPEX scales each month along a predictable growth pattern allowing the burn to stay flat at 1M per month.

The transactional business, however, has burn that varies each month with months like August and September ~25% higher. And if one-month misses plan it can be hard to know what the next month will bring. You could end up being on a burn spiral with each month successively worse or, conversely, cut burn prematurely only to see growth spike and be unable to keep up with customer demand.

Here’s a view of the P&Ls of these two company’s budgets by month. For simplicity, I’ve assumed the negative EBITDA equates to burn in both examples.

What You can do About It

At this point you might be tempted to wish you could go back in time and start building a SaaS business (no doubt it was an incredible invention of the 2000s!) But don’t lose hope here, transactional founder, there are many great examples of successful transactional fintechs (e.g. Stripe, Square, Affirm, Adyen, Coinbase, etc.) All of which navigated the growth phases of scaling a transactional model before maturing into incredible companies.

Here are eight things to consider while building your budget for ’23 to avoid potential cash/ runway traps.

1) Build in monthly minimums where you can. Increasingly, transactional fintechs are using this as a tool to combat seasonality and runway issues. Typically, these are structured as a minimum “platform fee” with monthly overages. Having these monthly minimums creates some base-line revenue expectation from which to build the conservative budget case. Monthly minimums also have the added benefit of helping to mitigate against dollar-based churn (and probably logo churn as well given they require a real commitment from the customer.) The key here is to do this as early as possible in your evolution vs trying to get customers to sign up for minimums 2 years in.

2) Understand your customer ramp process. SaaS businesses often have a customer onboarding phase and may have some ramp time as well. But transactional businesses almost always have a longer and less predictable ramp period depending on timing of roll-out and the idiosyncrasies of end merchant or consumer dynamics. If you are a payments business for example and rolling out your payments offering to multiple store locations with a single brand, it will take time to roll out to all locations AND each location will take time to ramp to full utilization. Add the complexity of seasonality and there can be a ton of uncertainty when building next year’s budget. Understanding how (and when) your customers ramp can make this more straightforward.

3) Allocate product and engineering resources to reducing costs. Having a good grasp of your unit economics, whether you are a SaaS or transactional business is always really important. But transactional businesses have an even greater opportunity to use automation to reduce certain costs that impact their gross margins and profit margins than their SaaS peers. In the fintech world, as you scale your business, R&D resources could be used to automate areas that start of as very manual in the earlier stages. Areas like customer support, delivery routing, fraud prevention, collections recovery, order tracking, etc, can all be automated over time leading to reductions in COGS and OPEX that ultimately improve margins and lower burn.

4) Hone your demand forecasting. As seen in the example above, so much of the monthly burn depends on whether top-line objectives are accomplished or not. Transactional businesses have internal factors (e.g. sales rep productivity) that certainly matter but macro factors also play a big role (ecommerce/ consumer buying behavior, interest rates from debt providers, delivery-related costs like fuel, etc.) Having your account management/ customer success teams tracking the top-line results of your top 5–10 accounts is a particularly important indicator as churn or volume declines in that segment can really impact the ultimate burn numbers. Demand forecasts for transactional businesses need to pull in all of these relevant variables and adjust the models rapidly to changing environments.

5) Budget carefully with clear stage gates and monthly check points. Given the unpredictability of transactional businesses combined with today’s tepid fundraising environment, transactional businesses need to be even more conservative when allocating funding to teams and initiatives than their SaaS peers. Projects and hires all need to have very clear ROI and rational. And if your monthly top-line goals are not being realized, especially 2–3 months of successive 20%+ misses, freezing or scaling back on spending is likely the right move until you figure out why the results aren’t showing up. There is nothing worse than throwing precious equity dollars at a product or gtm motion that is fundamentally broken.

6) Downplay months where you beat and sweat months you miss. With transaction businesses, any month (or even set of months) should not be viewed as indicative of the next month. In fact, monthly performance should really be compared to the same month last year. So don’t up the spend just because one or two months came in favorable. It could be temporary and later months could underperform. Similarly, missed months should be viewed with a high degree of concern. As they rack up throughout the year, the burn will likewise rachet up as well and could be severe if the performance worsens further during expected boom months without cost rationalization.

7) Be strategic about the timing of your next round. Transactional businesses have periods with lulls (e.g. summer months) and booms (e.g. holiday season). Investors intrinsically know this, and it may seem silly that seasonality isn’t discounted or normalized. It may in fact be discounted, nonetheless, don’t underestimate the psychological impact of timing on the success of your raise (especially in this environment where you need every edge you can get!) The top-line optics for an ecommerce enablement raise, for example, typically look at lot better if that raise is done in January vs July. If you can, find ways to manage your cash and stretch out your runway such that you can raise right after more favorable time periods.

8) Consider extending runway with alternatives to equity (but proceed with caution). Runway extension beyond equity used to be challenging to find for non-SaaS businesses. However, this has changed in the last 3–5 years as venture debt lenders (both bank and non-bank) have increasingly warmed up to alternative business models. The revenue-based-financing space (companies like Clearco, Pipe, Capchase, etc) has also begun to offer an intriguing alternative for runway extension in the form of non-dilutive financing. Just remember debt must be repaid at some point and can come with plenty of strings attached.

Transactional businesses have the potential to build incredible products and generate tremendous amounts of enterprise value. But managing cash and building budgets that make financial sense is no easy task, particularly in the early stages of growth. With a little bit of foresight and a whole lot of sweating the details, you can ensure your 2023 budget leaves you in a very strong cash position to realize your company’s ultimate vision.

Some of the world’s biggest ecommerce enablers are starting to look a lot like fintech companies.

Millions of Amazon’s Indian customers, for instance, are now taking advantage of instant zero-interest and low-interest credit to pay for products weeks or even months after receiving them. Shopify saw its revenues jump 57% year-on-year after unveiling a new Shop Pay checkout tool. And in Indonesia, ecommerce giant Tokopedia merged with fintech innovator Gojek to create GoTo, a tech giant that contributes 2% to Indonesia’s GDP.

This “great convergence” between fintech and ecommerce is partly driven by the global pandemic, which compressed a decade’s worth of ecommerce growth into a few short months. Customer trust in fintech, perhaps out of necessity, skyrocketed as we worked and shopped from home, and consumers remain eager to use innovations like contactless payments in the post-pandemic era. That’s left fintech players looking to ride the ecommerce wave, and ecommerce companies seeking to tap new fintech revenue streams such as payments.

As investors, we’re never going to turn our noses up at this kind of unprecedented opportunity. But we believe this “great convergence” isn’t just about companies scrambling to grab market share and drive revenue. The reality is that this is one of those rare instances where 1 plus 1 really does add up to 3 — because when you bring the right ecommerce and fintech companies together, you wind up with something that’s much more than just the sum of its parts. And that can only be a good thing for both merchants and consumers.

For example, two members of the Oak HC/FT family — financing pioneer Clearco and ecommerce innovator Cart.com — recently joined forces to provide merchants with access to capital and an end-to-end suite of ecommerce tools to scale their businesses. Cart.com users can now access up to $10 million in instant financing via Clearco — and Clearco customers can use Cart.com’s unified console to quickly and effectively deploy the capital they’ve raised towards marketing, fulfillment operations or software capabilities.

That’s good for both companies, which benefit from reaching a shared customer pool representing over 8,000 top ecommerce brands. But it’s even more exciting because it isn’t just about the synergies that come from bringing together powerful fintech and ecommerce solutions. It’s also about the shared vision for what intelligent fintech integration can help founders and merchants to achieve.

More on this partnership below:

Both Clearco CEO Andrew D’Souza and Cart.com CEO Omair Tariq have witnessed the challenges that developed as ecommerce grew increasingly fragmented and over-complicated, leaving founders scrambling to manage a patchwork of third-party services and vendors. Both companies were founded on the belief that there is a better way, and that by creating streamlined financing and operational support systems it is possible to help more startups achieve success.

Seen through that lens, the Clearco-Cart.com partnership is more than just a smart business move. It’s the logical next step toward something bigger: a world in which ecommerce brands and fintech solutions operate seamlessly to give founders the tools they need to grow. By taking the friction out of entrepreneurship, Cart.com and Clearco are making it easier for ecommerce founders to execute their visions, scale their businesses, and achieve their dreams.

That kind of value-add is why the “great convergence” between ecommerce and fintech is such a big deal. But it also reminds us that the goal shouldn’t just be to add a fintech layer to an existing ecommerce product or platform. What’s needed, to make this convergence multiplicative rather than merely additive, is a real mission to empower the next wave of ecommerce merchants. The best players in this space aren’t just trying to bring ecommerce and fintech together. They’re using ecommerce and fintech purposefully — to create a more level playing field for every founder.

This piece was originally published in TechCrunch here.

There’s an old startup adage that goes: cash is king. I’m not sure that is true anymore.

In today’s cash rich environment, options are more valuable than cash. Founders have many guides on how to raise money, but not enough has been written about how to protect your startup’s option pool. As a founder, recruiting talent is the most important factor for success. In turn, managing your option pool may be the most effective action you can take to ensure you can recruit and retain talent.

That said, managing your option pool is no easy task. However, with some foresight and planning, it’s possible to take advantage of certain tools at your disposal and avoid common pitfalls.

In this piece, I’ll cover:

The mechanics of the option pool over multiple funding rounds.

Common pitfalls that trip up founders along the way.

What you can do to protect your option pool or to correct course if you made mistakes early on.

***

A mini-case study on option pool mechanics

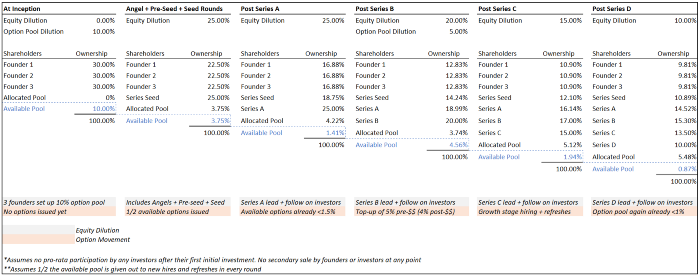

Let’s run through a quick case study that sets the stage before we dive deeper. In this example, there are three equal co-founders who decide to quit their jobs to become startup founders.

Since they know they need to hire talent, the trio gets going with a 10% option pool at inception. They then cobble together enough money across angel, pre-seed and seed rounds (with 25% cumulative dilution across those rounds) to achieve product-market fit (PMF). With PMF in the bag, they raise a Series A, which results in a further 25% dilution.

After hiring a few C-suite executives, they are now running low on options. So at the Series B, the company does a 5% option pool top-up pre-money — in addition to giving up 20% in equity related to the new cash injection. When the Series C and D rounds come by with dilutions of 15% and 10%, the company has hit its stride and has an imminent IPO in the works. Success!

For simplicity, I will assume a few things that don’t normally happen but will make illustrating the math here a bit easier:

No investor participates in their pro-rata after their initial investment.

Half the available pool is issued to new hires and/or used for refreshes every round.

Obviously, every situation is unique and your mileage may vary. But this is a close enough proxy to what happens to a lot of startups in practice. Here is what the available option pool will look like over time across rounds:

Note how quickly the pool thins out — especially early on. In the beginning, 10% sounds like a lot, but it’s hard to make the first few hires when you have nothing to show the world and no cash to pay salaries. In addition, early rounds don’t just dilute your equity as a founder, they dilute everyone’s — including your option pool (both allocated and unallocated). By the time the company raises its Series B, the available pool is already less than 1.5%.

While the option pool top-up (5% in this example) at the Series B helps to grow the unallocated pool, it is typically done so on a pre-money basis, meaning the new equity coming in as part of the round immediately dilutes the top-up. So, the resulting increase to the pool is closer to 4 percentage points than 5. The real dilution to everyone else on the cap table (founders, employees and investors) ends up being closer to 25% versus the 20% it would be if this was only an equity round with no top-up.

The company is again at less than 1% in available options at the Series D (two rounds after the top-up). This means further top-ups may be required, albeit at smaller amounts. The good news is that by the time of Series C and D rounds, 1% of equity can afford many more multiples of employees than 1% at the seed or Series A. Larger growth rounds also mean that cash compensation can become much more competitive, making up for smaller equity packages.

***

Common pitfalls

As you can see, even in this relatively “clean” scenario where the founders had the foresight to open with a 10% option pool, raised good up rounds (with stage-appropriate dilution), and only had one top-up round along the way, they were likely still managing/hiring on close to a shoestring budget. This is not a position you want to be in, especially in today’s competitive talent market.

The reality is that things can get much messier, leading to a thinner option pool earlier on that can impair your ability to hire great people. Here are a few common traps that can pop up and wreak havoc on your option pool:

Poor planning: You simply don’t have a sizable option pool right from the outset. You underestimate hiring needs or are overly sensitive about ownership. Many first-time founders make this mistake.

Co-founder departures: Your co-founder, who has material ownership, leaves after a year or two. While they only vested a quarter or half of their shares, that can be 5%-10% of dead weight on the cap table doing little for the company.

Giving out too much to early hires: You give out too much equity to early employees who are unqualified for their role or demand too much equity even after adjusting for stage risk. They then have to be replaced a few years in with a more seasoned hire, which makes you “double pay” in equity for that role.

Hiring execs at the wrong time: A derivative of the above is hiring senior leaders too early. For example, hiring an expensive CRO at the Series A stage, when you would be better off doing founder-led sales or hiring a few AEs. The CRO hire will be more impactful to the company by the time of the Series C and likely less costly on the equity front.

Not firing quickly enough: Failing to use the one-year cliff as a forcing function to make decisions on performance. If you let poor performers linger too long, you will almost always regret the equity that could have been used for an awesome hire. This needs to be balanced carefully with maintaining a healthy work environment and positive hiring dynamic.

Not using data/benchmarks: Making an equity offer on a whim/using your gut almost always ends badly. Either you end up overpaying and giving out too much equity, or you give out too little and turn away good candidates. Using benchmarks also makes negotiating offers with candidates easier, as it lends the perception of a competitive and fair offer.

***

OK, you made a mistake, but there’s still hope

If you have hit the growth/later stages and made mistakes similar to those above, you still have a few ways to correct course:

Create a bigger pool earlier on: The easiest way to ensure you don’t run out of options too quickly is simply to start with a bigger pool. As a founder, you might worry about more dilution from a bigger initial pool, and while that may be true in the short run, the flip side is that, with more options, you can hire faster and get better quality talent. That should translate to more progress, allowing you to raise competitive rounds with less dilution over time.

To use the example above: If you were to start with a 20% option pool instead of 10%, but then reduce dilution at each round by 5 percentage points, by the Series D you’d end up with higher ownership as a founder, more (and better incentivized) employees, and less heartache around pool management. Here’s a view of the end state by Series D in this scenario:

Hire slow, fire fast: Take the time to make sure you want to hire any individual. Especially early on or for senior roles, which tend to be the most expensive. And if it’s clearly not working, end the relationship as quickly as possible and certainly well before vesting starts to happen. This applies to co-founders, too.

Consider longer vest periods for founders/early employees: The co-founder departure scenario is a tough one, as founder equity tends to be significant and can result in lots of dead equity on the cap table. Consider lengthening vest periods to something beyond the standard four years, or make the vesting more back-ended — Amazon-style. If a departing co-founder has already vested equity, consider buying out their shares at a discount and put those shares back in the pool.

Hold budget/planning sessions on employee compensation each year: Forecasting key hires one or two years ahead can do wonders to help you think about the pace of option grant issuance and the trade-offs you have to make for each role/hire. At some point, usually in the mid-growth stages, it’s a good idea to establish a compensation committee, usually chaired by an independent board member, to review compensation each year and recommend decisions to the broader board.

Use benchmarking (and other) data tools to make offers: Startup compensation tools like Option Impact, Carta Total Comp and Pave are must-haves as you scale your company. They will make sure your offers are grounded in solid comps by stage, geography and title. More often than not, founders end up being too generous on the equity side. Using a compensation tool helps ground offers in data and prevents too much equity being granted too early on. You can also triangulate these benchmark tools with feedback from other founders and existing investors.

Tie refreshes and earn-outs closer to performance: As your company scales, consider tying refreshes and earn-outs closer to performance. This is particularly applicable for sales front, but can be useful even for marketing, product and GM-style roles that impact the acceleration of top-line growth. If performance leads to accelerated growth, everyone wins and such performance warrants additional equity.

Skew comp more toward cash in the later stages: As your company scales into the later stages, the risk decreases, and you have more cash to pay employees jumping on your rocket ship. 1% of equity in the later stages can be used to hire hundreds of employees; especially when you have the cash from growth rounds to pay higher bases + bonuses.

Utilize buybacks as a non-dilutive way to grow the pool: Buybacks can be used with angels, early investors and even employees, all of which may have made a nice return by the time of the Series C/D round, and may be willing to partially or fully exit, allowing you to use cash on the balance sheet to repurchase shares and put them back into the option pool.

One important concept to remember is the value of fundraising at milestones where you can minimize dilution. In the example above, we started with the notion that founders can manage to keep dilution to 25% before the Series A. However, this number often ends up closer to 30%-40% before the first major institutional round.

Future fundraises and option pool top-ups then end up diluting more, which can catch founders by surprise. Focusing on achieving clear milestones before raising capital prevents premature and heavily dilutive rounds.

Managing your option pool is key to the long-term success of your startup. In many ways, your option pool is the most important currency you have as a founder. With careful planning and some thought, you can turn your option pool into a powerful driver of growth and enterprise value.

***

As always, please reach out with any thoughts or suggestions (@MrAllenMiller.) I’d also like to thank Addie Lerner (@addielerner), Alex Kurland (@atkurland), Brian Murray (@murr) and Michael Sidgmore (@michaelsidgmore) for their help in reviewing early drafts of this and providing invaluable feedback.

My colleague, Tess Munsie and I, originally published this piece in TechCrunch here.

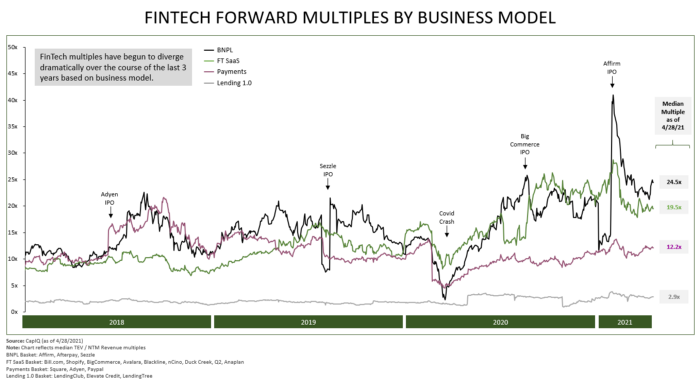

If there has ever been a golden age for fintech, it surely must be now. As of Q1 2021, the number of fintech startups in the U.S. crossed 10,000 for the first time ever — well more than double that if you include EMEA and APAC. There are now three fintech companies worth more than $100 billion (Paypal, Square and Shopify) with another three in the $50 billion-$100 billion club (Stripe, Adyen and Coinbase).

Yet, as fintech companies have begun to go public, there has been a fair amount of uncertainty as to how these companies will be valued on the public markets. This is a result of fintechs being relatively new to the IPO scene compared to their consumer internet or enterprise software counterparts. In addition, fintechs employ a wide variety of business models: Some are transactional, others are recurring or have hybrid business models.

In addition, fintechs now have a multitude of options in terms of how they choose to go public. They can take the traditional IPO route, pursue a direct listing or merge with a SPAC. Given the multitude of variables at play, valuing these companies and then predicting public market performance is anything but straightforward.

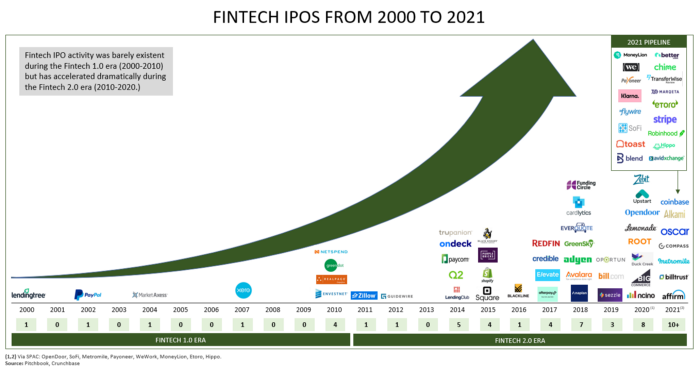

The fintech gold rush has arrived

For much of the past two decades, fintech as a category has been very quiet on the public markets. But that began to change considerably by the mid-2010s. Fintech had clearly arrived by 2015, with both Square and Shopify going public that year. Last year was a record one with eight fintech IPOs, and there has been no slowdown in 2021 — the first four months have already produced seven IPOs. By our estimates, there are more than 15 additional fintech companies that could IPO this year. The current record will almost certainly be shattered well before the end of the year.

Not all fintech is created equal

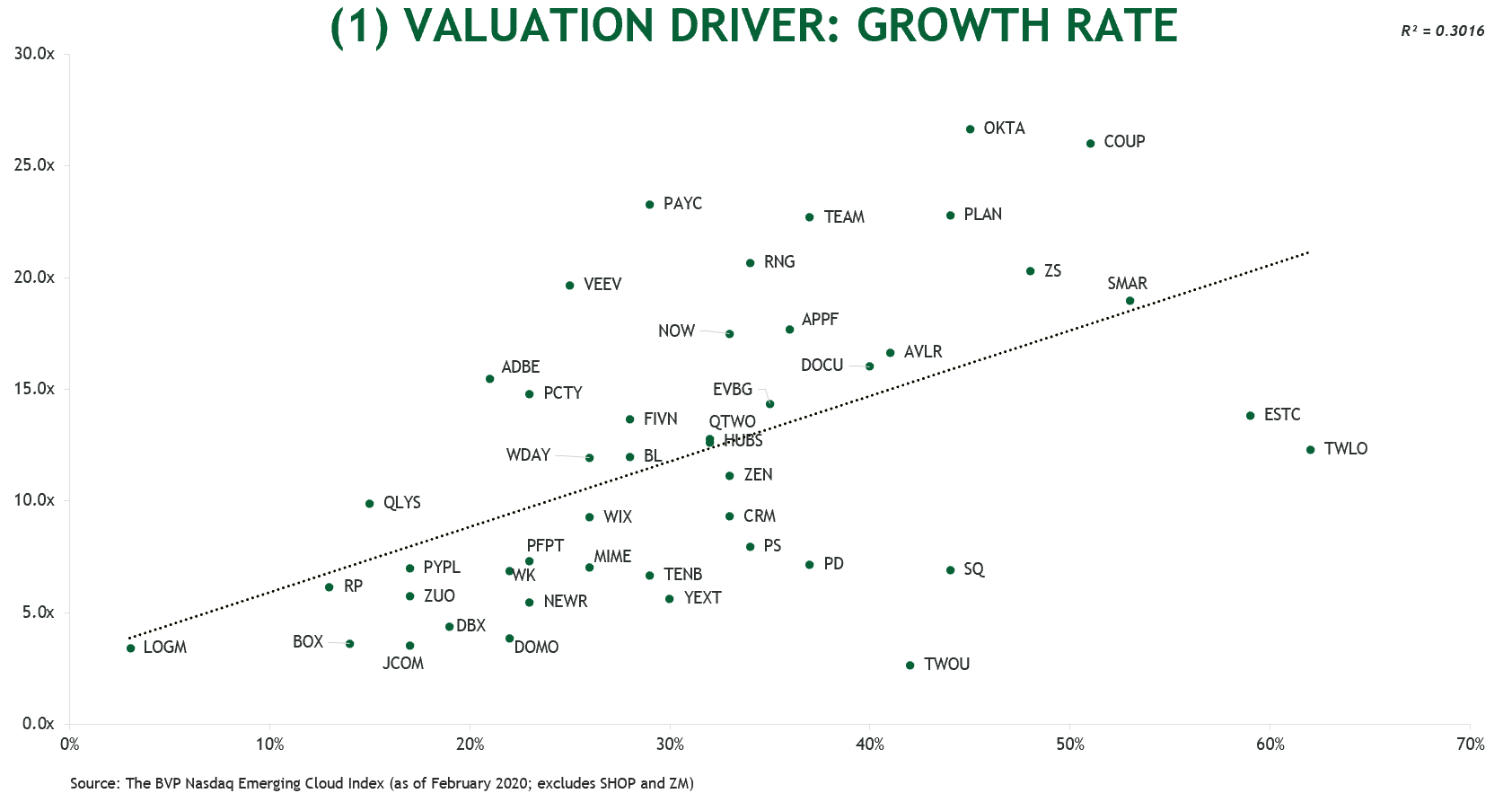

It is important to note that fintech is a complex category with many different types of players, and not all fintech is created equal. Nor will all fintech public valuations live up to the hype. To understand this more deeply, we need to examine the various business models that fintechs employ today and the revenue multiples these models can command on the public markets.

Broadly speaking, we can divide most fintech IPOs into four buckets: (1) Lending 1.0 (e.g., LendingClub), (2) Payments (e.g., Square), (3) fintech SaaS (e.g., Avalara), and (4) BNPL (e.g., Affirm). Just three years ago, all but Lending 1.0 coalesced at ~10x forward revenue, but the forward multiples (and valuations) of these companies have evolved substantially since — particularly in the year since COVID struck.

Lending 1.0

The first wave of lending companies has remained the lowest valued throughout this period at ~2x-3x forward revenue. This is despite recent favorable public market conditions for most tech companies. This low multiple is a reflection of overall deteriorating business characteristics (e.g., negative growth rates, high losses and challenged unit economics). Many of the Lending 1.0 players also served end customers like subprime consumers or brick-and-mortar SMBs that were heavily impacted by COVID.

We expect these Lending 1.0 companies to continue to trade at low, single-digit revenue multiples (likely around 3x). We have seen some consolidation in this space as well (OnDeck was acquired by Enova last year, for example), and suspect that there will be more M&A in the years ahead.

Payments

Payments has been the most consistently valued group of the four categories, rising modestly to ~12x during this three-year period (despite some fluctuations). This group includes scaled businesses like Square and Paypal generating billions of dollars in revenue at decent gross margins (40s-50s) and still growing at around 40%-50% year over year. As they mature and reach scale, many of these companies have diversified their product offerings and looked to inorganic channels for further growth.

We predict that this category will see slight valuation uplift in the coming years to ~13x-15x. This will mostly be a result of younger companies like Stripe and Toast entering the IPO pipeline in the next few years. With strong growth rates, these new entrants will receive higher multiples and raise the average multiple for the payments category.

Fintech SaaS

Like much of enterprise software, fintech SaaS was a very clear winner over the past 12 months, doubling forward multiples to ~20x. This was a result of positive COVID tailwinds, recurring revenue models, high gross margins (70%-80%+) and general business reliance on core financial software systems. Many of these companies also have very high net-dollar retention (in many cases >120%), perhaps the most important metric aside from growth.

That said, there is some potential that this category has experienced the most multiple inflation of the four categories. As we move into a post-COVID era, 20x revenue multiples may not be sustainable. We expect fintech SaaS companies to reset to a new “steady state” well above 10x, but likely in the 15x-20x range.

Buy-now-pay-later (BNPL)

BNPL is the newest and most fascinating basket of the bunch. Pre-COVID, this group quickly expanded up to trade at ~15x due to 100%+ growth rates, hyper network effects, enormous markets and consumer virality. At the start of COVID, these companies saw their multiples briefly dip almost down to Lending 1.0 levels before the market priced in the strength of these models and their enabling of e-commerce merchants (many of which were COVID-accelerated), all while seeing no material impact to loss ratios. While average multiples in this category briefly exploded to 30x+, with Affirm’s debut, we have seen them fall back to earth a bit.

Still, this category currently commands the highest multiples in all fintech at ~25x. Given we are still in the very early innings of e-commerce globally, we expect the near-term steady state for BNPL multiples to be somewhere in the 20x-25x range. We look forward to Klarna’s reception on the public markets later this year.

But what about insurtech and crypto?

Importantly, there are two additional categories (not pictured above) that have begun to emerge within fintech: insurtech (Root and Lemonade) and crypto (Coinbase). While the data is still limited in terms of number of IPOs and time on the public markets, we will eventually add these as their own categories to the chart above. As of the end of April, Root was trading at 6.6x, Lemonade was trading at 46.7x, and Coinbase was trading at 12.5x.

The return of the SPAC

One big caveat to our discussion on valuation and multiples is, of course, the return of the SPAC. In 2020, SPACs burst back onto the scene and have rapidly made an impact on the IPO landscape. Metromile was the first fintech to be taken public via SPAC this year, but there is a wave of additional SPAC IPOs on the horizon (e.g., SOFI, Hippo, Payoneer and MoneyLion) and plenty of demand from investors for SPAC IPOs — there are currently over 150 fintech or financial-oriented SPACs seeking targets.

SPACs represent the Wild West for fintech public valuations. SPACs targeting fintechs is a relatively new phenomenon, and many of these blank check companies are taking fintech targets public earlier than they otherwise would via a traditional IPO. How SPACs perform on the public markets and the impact they have on the fintech valuation story is perhaps the most interesting question for 2021.

That said, whether it be via SPAC, direct listing or traditional IPO, we are likely to see at least 10 to 15 fintechs go public this year — possibly more. That is nothing short of astounding. The spotlight will be bright this year on fintech IPOs as the gold rush continues.

***

You can access the data (including the underlying raw data) for the graphs above by clicking the link here.

As a growth stage SaaS founder with $5–10M in ARR, you have much to be proud of. You have made it to a point <1% of all startups make it to. You have achieved product-market fit, real customers find value in your software, investors believe in your vision and you have grown from a few founders sitting at a kitchen table into a rapidly scaling team with org charts, all-hands meetings, and maybe even (virtual) company retreats! Looking back at the last 3–4 years, you have accomplished a lot and avoided many “near-death” moments. There’s a lot to be excited about.

But in the back of your mind, there is the next big looming hurdle to get through — the so-called “Valley of Death” that many a great SaaS startup has succumbed too. Somewhere in that $10–50M ARR range, many good startups destined for greatness peter out. Many things can happen. Maybe it’s existential: the market you were building for is not ready for your product, turns out to be smaller than expected or you are only able to appeal to a small segment. Perhaps the unit economics are not holding as burn ramps. Or maybe it’s a people issue: a key founder quit, or the leadership team just can’t scale.

Most of the time, however, the failure point post $10M ARR occurs when the GTM machine stops working. This post, which draws on my time advising growth-stage startups as a consultant and now as an investor, examines why this happens and what you, as a founder, can do to avoid the Valley of Death.

Sales Efficiency as a Key Symptom

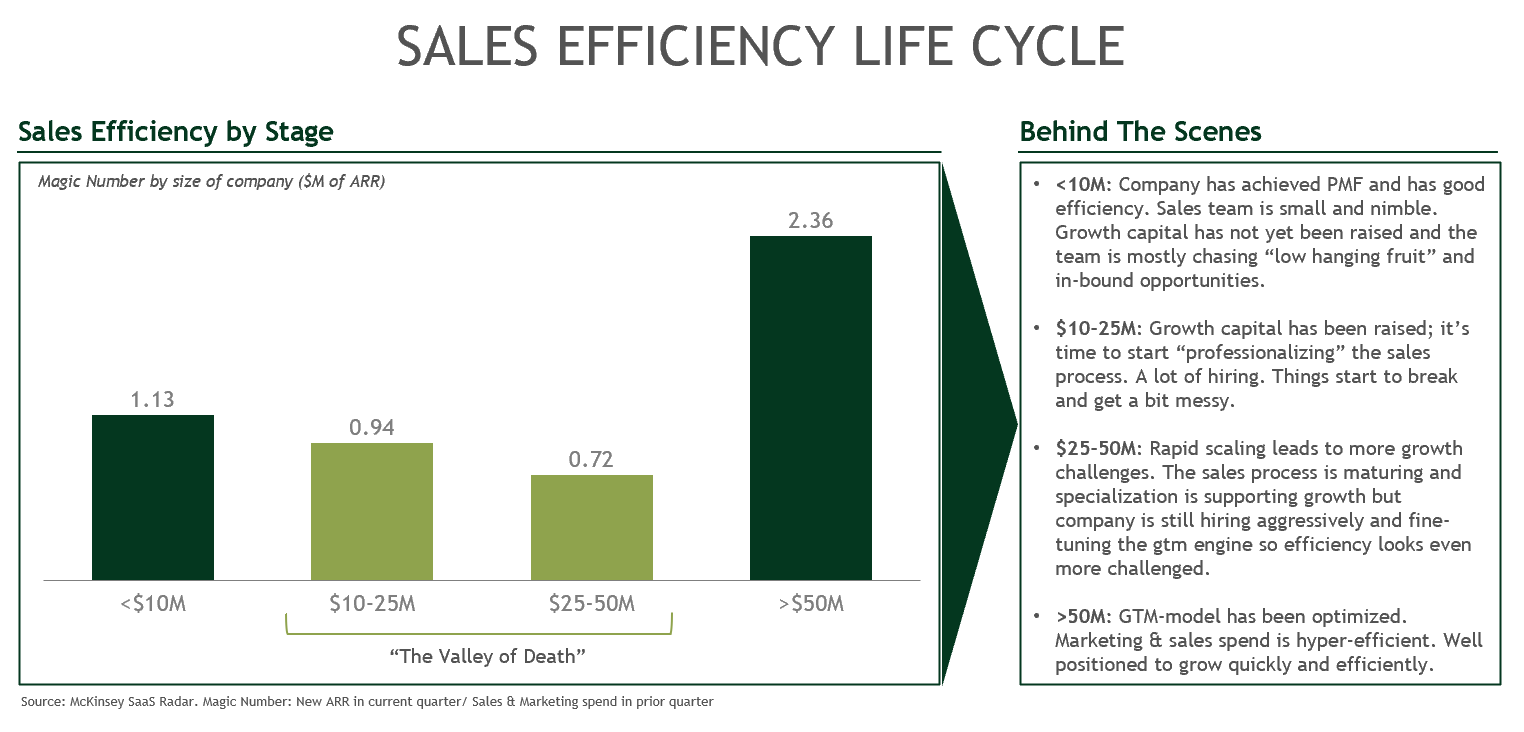

I have previously written about the importance of capital efficiency for SaaS businesses (see here.) More specifically, sales efficiency is the single most-telling operational metric for growth-stage SaaS businesses. To get through the Valley of Death, you need to maintain a high growth rate. Maintaining a high growth rate can’t happen without dollars spent leading directly to the new ARR. Sales efficiency (as measured via magic number), directly measures the ROI of sales and marketing spend on growth. McKinsey’s SaaS Radar has some great data on sales efficiency by ARR stage:

Let’s unpack what is going on here a bit further. In that “honeymoon” $5–10M ARR range, things are working very well on a micro-level. You are post-PMF and scaling efficiently for a few reasons. Your sales team is small and nimble; you are either doing founder-led sales or have a few reps who you have personally coached and have been there since Day 1. They are intimately familiar with the company and product and have high incentives to perform. Much of the opportunities you are hunting are new logos in that initial use case you designed the product for. It’s often a perfect match so the sales are easy; you may even have a fair amount of inbound based on referrals from early customers or people in your network. You have the normal startup twists and turns, but overall, things are peachy.

But somewhere around $10–25M in ARR, the sales efficiency starts to go down-hill. Part of this is a result of being in the “early growth stage” — you have raised that first growth round (see here on how to do it) and have started to invest in more sales and marketing headcount. New AEs take a quarter or two to ramp, you have to build out a real SDR program and you’re starting to think about investing in SalesOps to marry action with data. But other root causes behind this phase of growth are more troubling: perhaps that initial use case is starting to show limitations, maybe the product is hitting certain failure points thereby creating more churn, or perhaps the return on acquisition channels is worsening.

As the saying goes, it can often get worse before it gets better. The $25–50M ARR range can often look even more problematic from a sales efficiency perspective. Maybe the GTM and sales motion is starting to mature but the rapid hiring (ahead of growth) is masking the improvements. Maybe there is something external like new competitors or the TAM ends up proving to be more challenged. Regardless of the root cause, this can be a tough stage to be in — particularly since you have likely been focused on sales efficiency for at least a year or two and are not seeing the fruits of your labor.

The good news is that, if you are able to get through the $10–50M valley of death, things typically start to look a lot better on the other side of $50M in ARR. Companies that breakthrough this threshold are usually benefiting from a hyper-optimized sales & marketing engine and are able to grow quickly and efficiently. The magic number for companies that get here, on average, is greater than 2 — meaning for every dollar you are putting into marketing and sales, you are getting more than $2 in new ARR.

So the question then becomes: how do you navigate this valley of death to the hallowed lands of $50M+ in ARR? The key is to focus on high-potential levers that can improve sales efficiency.

5 Levers to Improve Sales Efficiency

There are many ways to improve sales efficiency in that $10–50M ARR range but the below 5 are likely the highest leverage actions you can take as a founder to increase sales efficiency.

(1) Hire an A+ VP of Sales/ CRO

The single highest leverage point you have as a founder to manage sales efficiency through the valley of death is to hire a strong VP of Sales or Chief Revenue Officer. Your headcount on the sales side is going to balloon and you will need a leader who can run a tight ship and work efficiently with other departments. In an ideal world, you would find someone who has all the attributes below:

He or she has lived through that $10–50M ARR window several times before and has built a career in your category or in a very close adjacent category (e.g. if you are a marketing SaaS startup, look for someone who was VP or SVP level at places like Hubspot, Marketo, Mailchimp, etc.) but is hungry to take on more ownership. This person would ideally have been a key leader in SaaS businesses that made it to $50M ARR, but if they were also with a company or two that failed to break-through that barrier that can also be useful in terms of lessons learned.

The sales leader also needs to have been responsible for building (not just managing) sales organizations from teams of 5–10 to 50+ in the past. They should know the traits needed in each role from SDR to AE to Manager and how to hire on the right cadence. If they can bring people with them from prior roles, that “followership” can help accelerate ramp time. Importantly, they should also have a healthy perspective on other key roles that could be used to support the front lines such as SalesOps and Account Management. Sales Ops, in particular, is an important data-driven role that every strong sales leader values and puts into place early.

The right VP of Sales/ CRO will also come in with a playbook on the sales process and the tooling required to build a robust GTM machine. They should know how to translate the product and sales knowledge living in your head into systematic policy and procedure that can be adopted by the broader organization. Beyond this, the sales leader should also have strong views on pipeline stage gating, pricing/ packaging, and people development.

Lastly, and perhaps most importantly, a good sales leader is a magnet for other top sales talent — be it sales managers, AEs, SDRs, etc. Attracting a high-quality sales leader can accelerate the overall talent pool and help you get where you are going faster and with fewer “people issues” along the way.

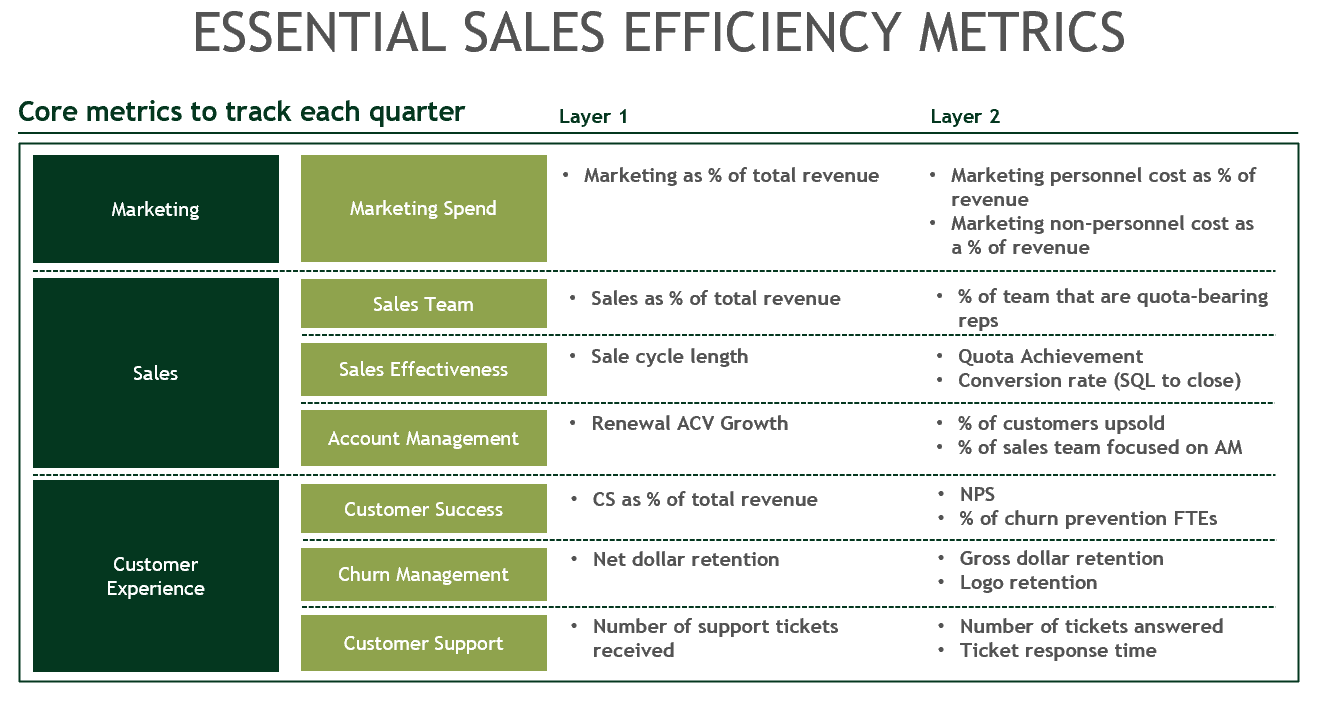

(2) Be religious about tracking core GTM metrics

Sales efficiency and more specifically magic number, in the end, is what you are trying to optimize. However, in order to do that, you really need to be tracking at least a few more layers beneath on a quarter-by-quarter basis. My suggestion is to break the GTM machine into its 3 primary orgs: marketing, sales, and customer experience. And then track at least 2–3 of the core metrics that impact sales efficiency (in addition to everything else you are tracking.)

You should also strongly consider investing in sales analytics software. Some of our portfolio companies have had great success with tools like People AI (revenue intelligence), Clari (RevOps) and Aviso (AI-powered selling.)

(3) Drive towards product-led growth + digital enabled sales

Long sales cycles, uncertain payback periods and choppy sales motions can impact sales efficiency negatively as they drive up sales and marketing costs without the benefit of incremental ARR. This can become especially magnified, early on, if you are selling to large enterprise customers, making it difficult to do other things like attract outside investors, decrease customer concentration risk and build a scalable/ repeatable playbook.

On the flip-side, if you have a bottoms-up motion, it will be pretty hard to accelerate through $50M in ARR without moving upmarket. Moving up-market works best if you have a land and expand motion (and typically with a freemium business model.) This allows the sales team to automate SMBs and move them to a self-serve/high-velocity motion (digital enablement) while refocusing the core sales team’s efforts upmarket. Nevertheless, never completely lose sight of the SMB segment as they are your growth engine and can help spur organic, word-of-mouth growth.

Regardless of where your customer base is today, every company should be focused on driving growth via product. Even the largest of enterprises, with their long sales cycles and complicated procurement processes, will accelerate their processes if they are seeing rapid adoption of their products “bottoms-up” by their employees. I saw this happen firsthand in my time at McKinsey where Slack and Box eventually upended decades-long relationships the firm had with IBM and Microsoft in the messaging and file-management categories. PLG can be a powerful force for overcoming inertia.

Digital enabled sales, which take a few different forms, can also lead to higher efficiency. Sometimes it’s a paired-down offering distributed on a self-service basis. In other situations, it is low-cost marketing and sales funnel that results in an inside sales motion. In both cases, digital sales can generate greater pipeline momentum than direct/ field sales as well as help you appeal to a broader customer base. This has never been more true than today in a post-covid world.

(4) Get as close to consumption-based pricing as possible

A close cousin of the PLG + digital-enabled sales strategy above is to push your pricing model towards consumption-based pricing. Consumption-based pricing, when done right, is the most efficient pricing model because it allows the customer to naturally expand as they consume more with very little incremental sales and marketing spend on your end. Consumption-based pricing is also the most value-based pricing scheme you can offer, which means the pricing levels tie closely with incremental value delivered. This allows for close alignment between you and your customers.

Some of the most sales efficient (and fastest-growing) SaaS companies employ consumption-based pricing. I’m including a few of my favorite examples of effective consumption-based pricing below:

Twilio: varies by product line but some examples are pricing based on the number of minutes to receive/make a call, number of SMS messages sent/received, etc.

Digital Ocean: pricing is based on the volume of data/bandwidth and the amount of time virtual machines are active

AWS: one of the original pioneers of consumption-based pricing, uses storage consumed (per GB) with volume discounts that come as you enter hire bands of data usage

Clearbit: all plans start with a $20K platform fee but thereafter pricing is based on CRM database size, web traffic, and monthly contact creation

Datadog: varies by product line but examples include per million log events, per 10k sessions, or per 10K test runs

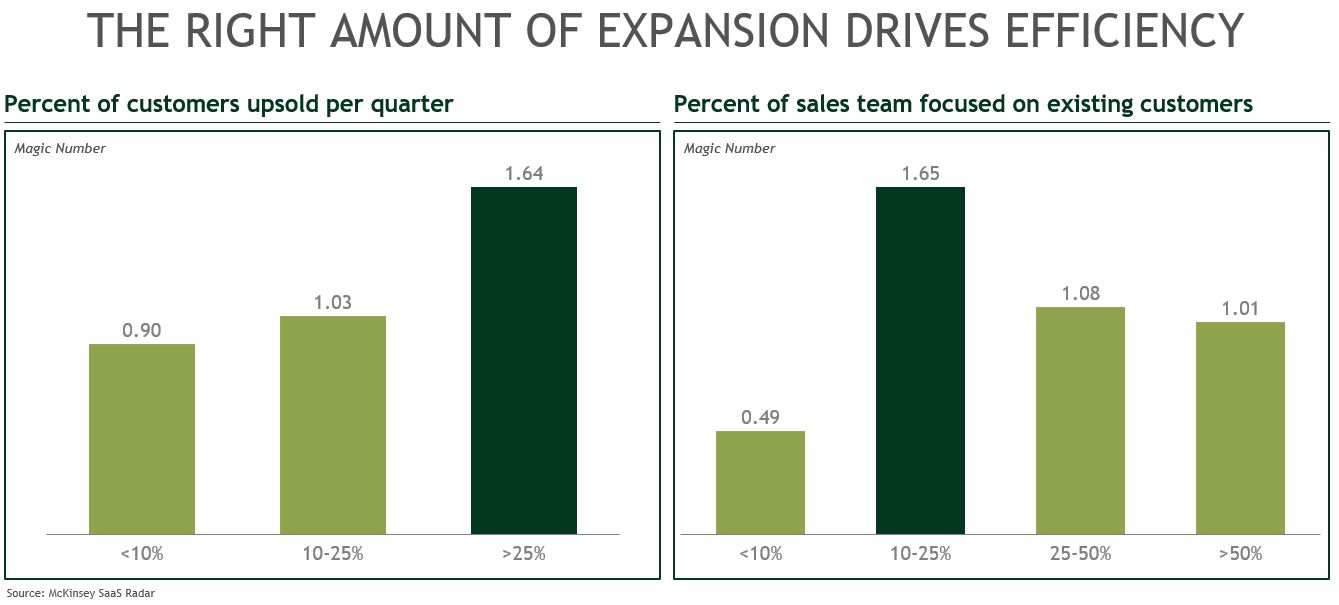

(5) Work the up-sell and cross-sell

The final strategy for improving sales efficiency is to mine existing customers. Generating incremental expansion dollars from your customer base is far less costly than acquiring a new logo. And the evidence shows that companies that expand >25% of their customers benefit from higher sales efficiency:

An important point here is that there is a “goldi-locks” level of attention that ought to be placed on the expansion of existing accounts — roughly 10–25% of your sales team should be focused on current customers. More than that and you will start to see diminishing returns and the effort is better spent on new logo acquisition.

Concluding Thoughts

Scaling through the valley of death and getting to 50M ARR is certainly no easy task. Very few SaaS businesses have made it through this phase of growth and the pitfalls that come with the territory. But hopefully, a sharp focus on sales efficiency, combined with the utilization of levers outlined above, will increase your chances of success.

As always, please reach out with any thoughts or suggestions (@MrAllenMiller). I’d also like to thank Kris Rudeegraap (@rudeegraap), Preeti Rathi (@preet1rathi), Sam East and Bill Macaitis (@bmacaitis) for their help in reviewing early drafts of this and providing invaluable feedback.

We originally published this piece in Forbes here.

Over the last few years, consumer fintech has been all the rage. And for good reason: consumer fintech startups have greatly improved the customer experience across many financial applications. This has led to a number of great outcomes including Intuit’s acquisition of Credit Karma for $7.1B earlier this year and Paypal’s acquisition of Honey for $4B at the end of ’19. And consumers are voting with their wallets: 14.2M Americans (6% of US adults with a checking account) now consider a challenger bank like Chime, Varo, etc to be their primary bank.

While the spotlight has long centered on consumer fintech, 2020 will mark the year that B2B fintech finally steals the show. Not only b/c of the recent exits we’ve seen (Plaid’s $5.3B sale to Visa, SoFi’s $1.2B acquisition of Galileo and nCino’s recent IPO) but also because of the ever expanding purview of B2B fintech. This begs the natural question: what is B2B fintech?

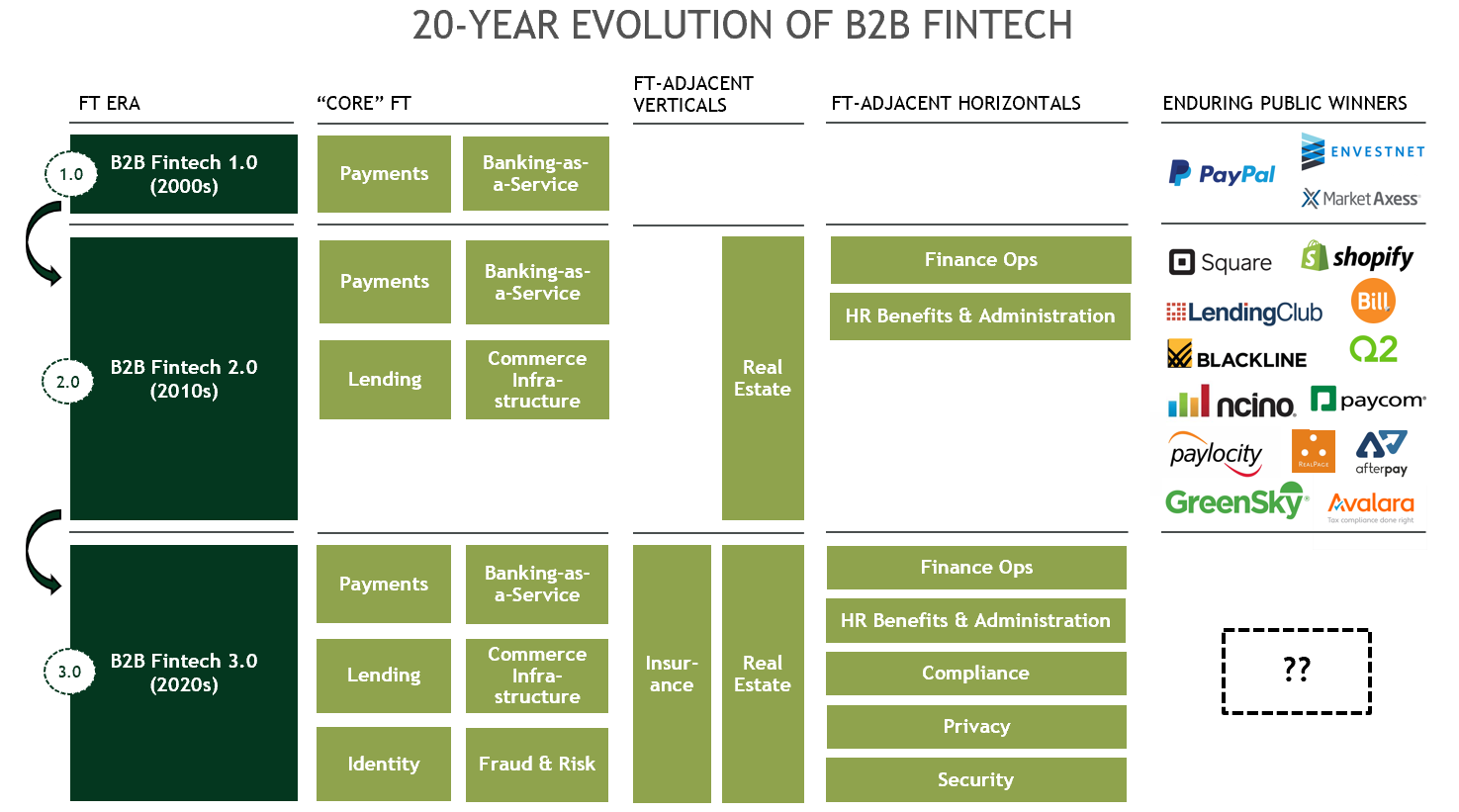

A 20-year Evolution

Defining B2B fintech requires going back in time a few decades. If we look at the evolution of B2B fintech, we are effectively on the cusp of a 3rd wave: fintech 3.0. The last 20 years have witnessed a widening of B2B fintech’s mandate and, as a result, a broader base of enduring public winners.

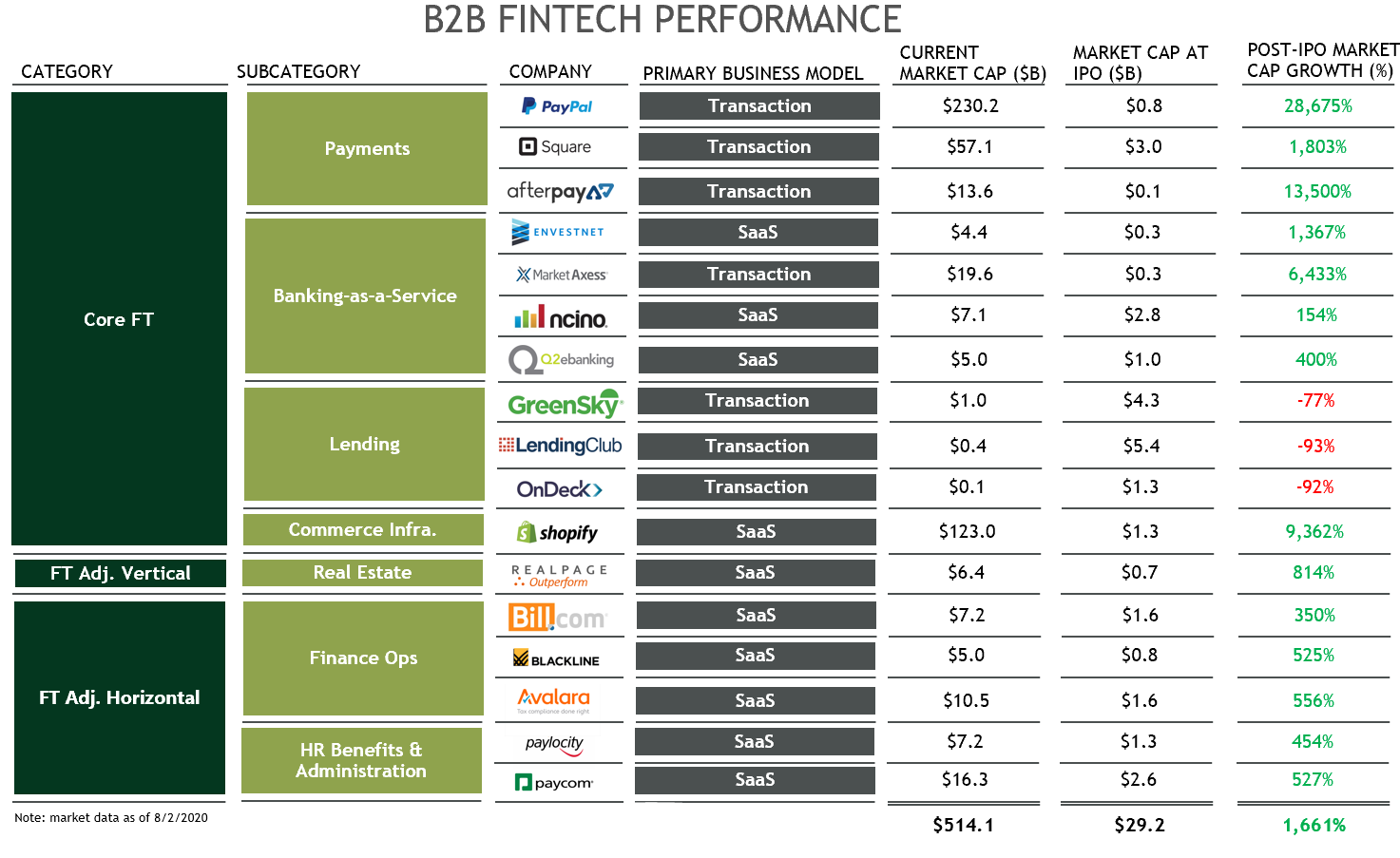

Modern B2B fintech first began in the early 2000s with companies focused on just two “core fintech” areas: payments and banking-as-a-service. The most notable company to come out of fintech 1.0 was of course Paypal. Founded at the dawn of the internet, Paypal actually operated via a B2B2C model, embedding at the point-of-sale with merchants and enabling consumers to transact with merchants effortlessly. Paypal now has a market cap of over $230B.

In the 2010s, fintech 2.0 emerged and the definition of B2B fintech began to expand. Within “core fintech,” we saw payments and banking-as-a-service continue to deliver big outcomes (e.g. Square, Afterpay and Q2.) But core fintech expanded with the rise of lending-focused companies (e.g. LendingClub, Greensky) as well as commerce infrastructure (e.g. Shopify.) We also saw the emergence of enterprise software/SaaS companies in fintech-adjacent verticals like real estate (e.g. RealPage) and horizontals like finance operations and HR benefits (e.g. Blackline, Bill.com, Paylocity.)

In the 2020s, we are sure to see fresh winners emerge in the fintech 1.0/2.0 categories. Many of these categories (like payments) are evergreen and continuously evolving. Others are still quite nascent in their overall development arc. But fintech 3.0 will continue to further fintech’s broadening mandate. Core fintech will expand to include winners in identity, fraud and risk (several of which are already in the making.) We are also likely to see additional winners in fintech-adjacent verticals like insurance and fintech-adjacent horizontals like compliance, privacy and security.

Historically Strong Performance

Fintech 3.0’s prospects are particularly exciting given just how well earlier generations of B2B fintech (1.0/2.0) have performed on the public markets. With the notable exception of the lending category, every other category has posted at minimum triple digit growth post-IPO. In fact, the aggregate market cap of this basket of B2B fintechs has increased 1,661% post-IPO and is now worth half a trillion dollars.

Themes & Building Blocks for Fintech 3.0

As we look towards the 2020s, fintech will continue to broaden in scope and mandate. We will see core fintech areas like payments, banking and lending continue to re-invent themselves again and again. We will also see a greater number of enterprise software/ SaaS entrants rising up across verticals and horizontals in adjacent areas to traditional fintech.

Perhaps even more intriguing will be the meshing of these fintech themes with the broader trends in technology, product functionality and commercialization. Many of the building blocks seen in other parts of the technology landscape will be expressed through these fintech 3.0 entrants. This will include, for example, the latest tools in machine learning, automation and open source. This will also include a myriad of gtm approaches (e.g. top-down, bottoms up, product-led-growth, etc.)

Suffice to say, the 2020s are going to be an incredibly exciting time to be building and investing in B2B fintech. The number of B2B fintechs that will be public in 10 years’ time will triple, generating well over $1T in total aggregate value. B2B Fintech has arrived and is not going anywhere anytime soon.

When I first landed in venture, it was with an early stage focus: predominantly Series A. The body of knowledge available to founders raising a Series A was pretty robust at the time thanks to investors demystifying a once opaque process via public blogs and forums. YC has since added even more transparency, creating a great Series A guide for founders looking to raise a Series A.

As I’ve move into a multi-stage environment (early + growth), I’ve been surprised by the dearth of information on fundraising for growth rounds, particularly that first growth round: the Series B. There are of course lots of good posts focused on metrics of all sorts, scaling in the growth stages, etc, but the existing literature doesn’t really cover how to raise a Series B — and certainly not in a tactical way.

This is particularly relevant in a post-covid world. If you look at the Pitchbook data from the last few quarters across stages, the story is quite interesting. Early stage deals (Series A) and late stage deals (Series D), saw a massive drop-off in dollars invested between Q4 ’19 and Q1 ’20 but then a decent sized recovery in Q2 ’20 (not all the way back but venture dollars returned 30%+ and the upward trend will likely continue into Q3 ’20.) Series Cs actually saw an acceleration through Covid.

The Series B round, however, while declining in a more measured way, continued a several quarter decline with almost no recovery from Q1 ’20 to Q2 ’20.

Source: Pitchbook

My hypothesis here is that the market is bifurcating around this new “ugly duckling” round — creating something like the Series A crunch of 2015. Why is that? At the Series A, investors can put in a relatively small check and get higher ownership to compensate for the risk taken. Not every Series A needs to work; high ownership in a few measured bets can return a fund making up for losses elsewhere.

In the later stage rounds (e.g. C and D), the winners start to become much clear and there is plenty of later stage capital ready to go to work into obvious winners. The returns in the later stages may not be as out-sized as at the A, from a multiple perspective, but a big check can return a sizable dollar amount at a decent IRR while ensuring investors are unlikely to take a 0 on any given investment.

But that first growth round (Series B) is becoming an increasingly difficult round for investors (and, consequently, for founders.) The company is perhaps somewhat de-risked from a PMF perspective but there are still substantial GTM and scaling questions that need to be answered. As such, Series B investors are forced to put fairly sizable checks to work ($20–$40M) without the ownership level of a Series A or the “certainty” of a later stage round. This becomes a bit more amplified in a post-covid world where there are even more unknowns.

This post is my attempt to shed some light on how to approach the Series B so that you can raise a successful first growth round.

A Quick Preface

Before we get started, because the letter of the alphabet can mean many different things to different people, I’ll begin by caveating what I mean when I say “Series B.” The profile for most companies going out to raise their first growth round (i.e. Series B) looks something like:

~$5–$10M ARR (though the range has become much wider on both ends)

To-date has raised anywhere from $5M to $25M (across angel, pre-seed/seed and A rounds)

Raising ~$20–$40M with a single lead or co-lead(s) doing the majority of the round

Has anywhere from ~2–4 years of financial history; company likely ~4–6 years old

Original founder(s) most likely still at the helm and running the day-to-day

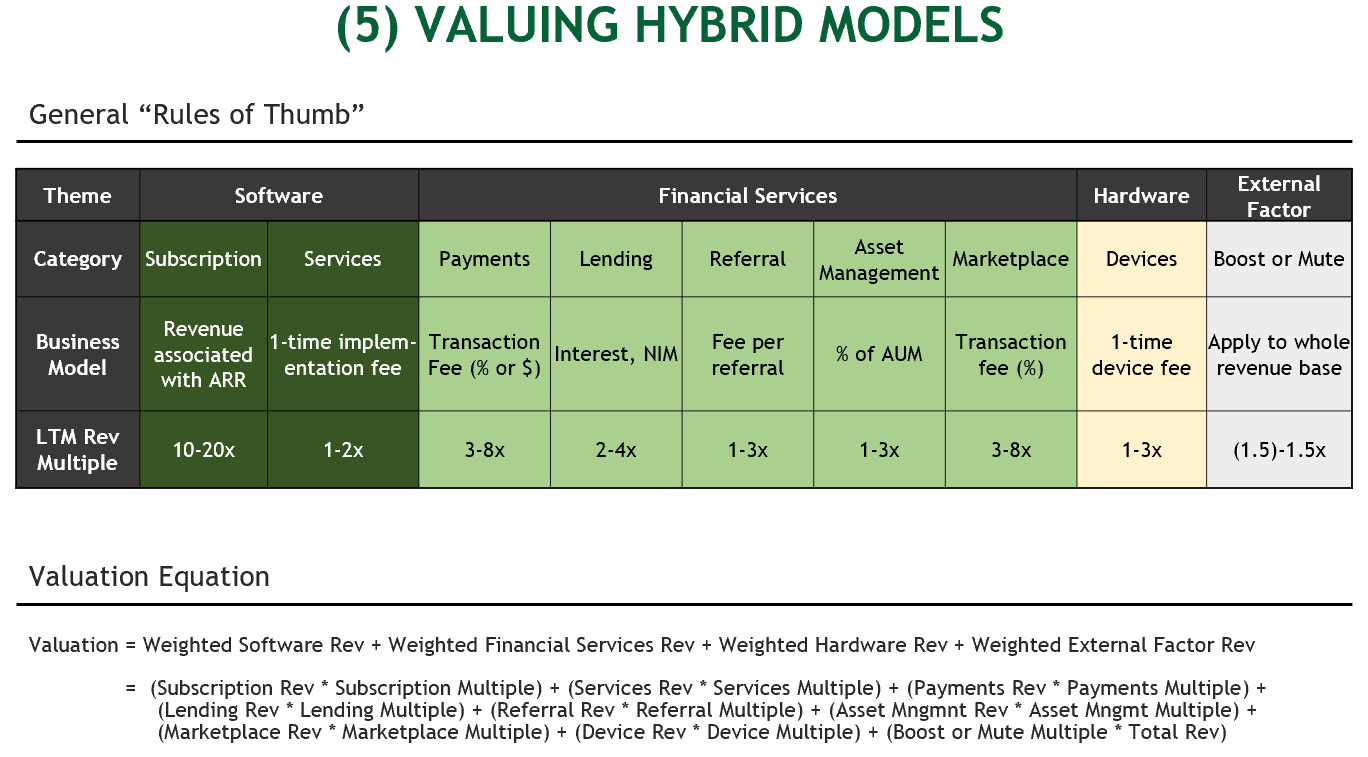

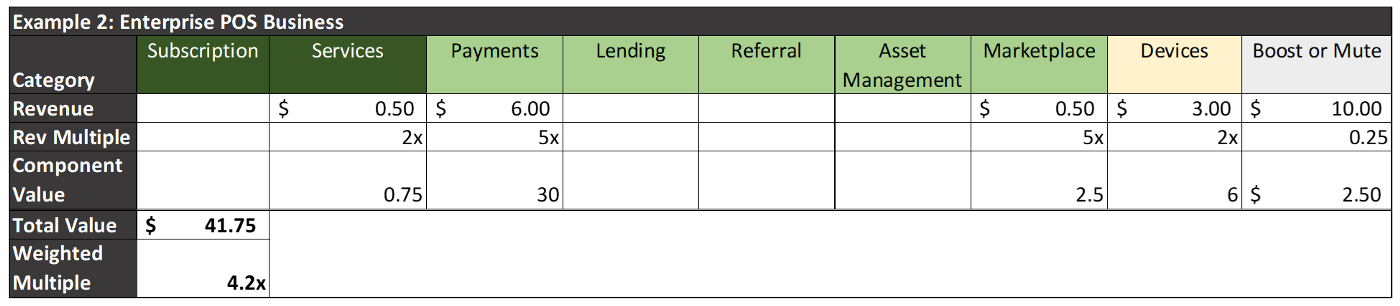

This is, of course, overly simplistic as Series B companies have a broader range of profiles (so bear with me!) I will also assume a SaaS business model (though the learnings could be extrapolated to other B2B models, including hybrid models, which I have previously written about here.) I’ll also briefly mention that many of the lessons discussed below for the Series B also extend into later-stage rounds (e.g. Series C, D, etc.)

Building on the A

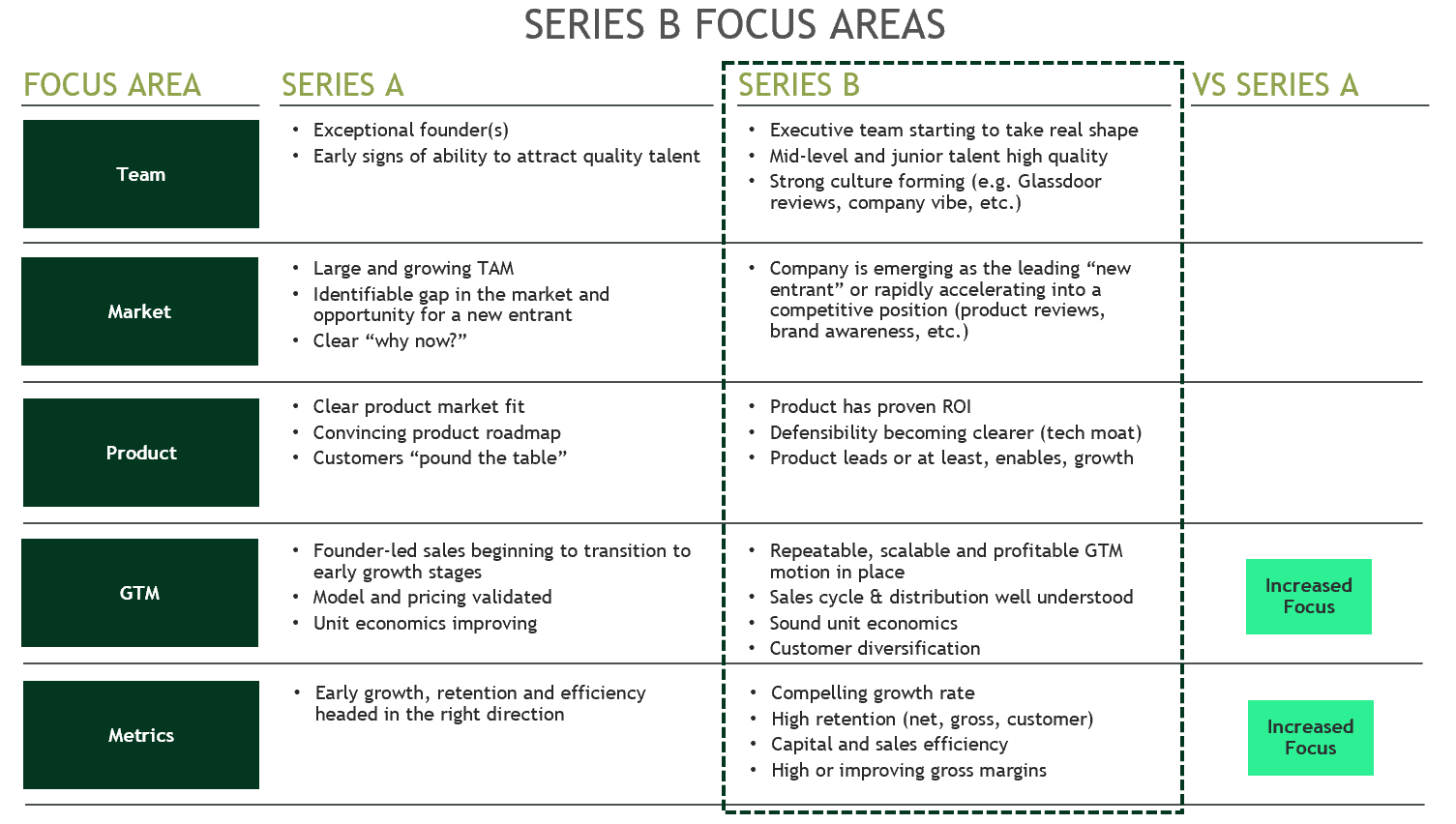

The best way to frame the Series B and how investors will evaluate your company is through the lens of “building on the A.” Most investors, generally speaking, focus on five key areas: (1) team, (2) market, (3) product, (4) GTM and (5) metrics. The first 3 have some additional features that build on what was established at the Series A while the latter two have a materially increased focus vs the Series A.

This is probably obvious: more time in the market means more data investors can analyze to assess whether a company has the potential to scale into an enduring brand. Let’s take a closer look at each of the 5 focus areas and how the Series B builds on the A.

Team

At the Series A, investors are looking for exceptional founders (passion, vision, grit, deep knowledge, charisma, etc.) There is a lot to unpack there but that is a separate post on its own! We are also often looking for early signs that the founders can attract high quality talent in the form of early team hires.

At the Series B, much more attention is paid to the broader executive team and how it is starting to shape up. In addition to assessing your ability to recruit great functional leaders, who have their own strong follower-ship, investors tend to start thinking in terms of “gaps that need to be filled” as part of the post-B phase of growth. Maybe you are at the point where you need a VP of Sales to lead GTM. Maybe the founder needs to transition product to a VP of Product to focus on other areas. Or maybe it is everyone’s favorite: time to hire that seasoned COO to support the young first-time founder!

The other area Series B investors will start to focus on is culture. Often by the B a distinct “cultural ethos” has started to form. Investors will try to glean what sort of vibe your startup has and how it is perceived in the market. This can be accomplished by spending time on-site at the office, looking closely at employee NPS and digging around to see what can be found “outside-in” via channels like Glassdoor. In a post-covid world, where in-person visits are now much harder, a company’s digital footprint will likely matter even more. Investors will also spend more time 1:1 with key executive leaders over video.

Market

When raising the Series A, the market story needs to be one of a large ($10B+) and growing (5%+ CAGR) TAM. There also needs to be some story around a gap in the market or a greenfield opportunity enabled by sleepy incumbents underserving some portion of the market (e.g. SMBs, developers, a new function like SalesOps, etc.) Articulating a clear “why now?” is also a very important part of the fundraise story.

At the Series B, investors will look for validation of the story you told at the Series A and whether the early momentum backs up that story. It is most compelling if your company is very clearly emerging as the market-leading new entrant. Investors will validate that by speaking with customers, reading product reviews from G2 and digging around on sources like Pitchbook and Google trends, to understand brand awareness and signal.

Product

Demonstrating early signs of product market fit at the Series A is paramount. In the end, this may be the single most important factor (outside of the founders) in determining a successful A raise. Investors will look for customers who “pound the table” and sticky enterprise user behavior. Beyond that, they will look at the road map to see if it is compelling and headed in a direction that matches the broader vision.

At the Series B, there are a few more product-components that matter. At this point, the product should show a clear and quantifiable ROI for the customer. There should be case studies and “customer-wide data” that demonstrate the ROI (whether it is cost savings, revenue lift or some other metric.) It also often helps if the product is developing in a way where there is a tech asset that creates a broader moat.

GTM

Relatively less attention is paid to GTM at the A. At that stage, founder-led-sales is common — though there may be some early signs of a transition to non-founder AEs. Typically the pricing and delivery model has been validated at the Series A. End-state unit economics (e.g. LTV:CAC, payback, etc.) are largely theoretical but improving quarter over quarter.

When you set out to raise the B, investors will be looking for a tighter story around GTM. They will look to see a scalable, repeatable and profitable motion in place. At this point you should have a pretty well understood sales cycle (e.g. how the funnel gets filled, how much time is spent at each point, what % convert, etc.) The unit economics that were theoretical at the A should be more proven-out at the B.

It is also really powerful if you have diversified the customer base. If moving “bottoms up,” for example, you may have a core startup-base of early adopters but now also have a strong set of mid-market logos, maybe even some 6-figure enterprise ACVs. You may have also started diversifying from one industry to several — this has become particularly important post-Covid when it has become clear that reliance on 1 vertical, even if performing well, can lead to a very false sense of security.

Metrics

Perhaps the biggest difference between the A and the B is that the availability of data makes the numbers matter a lot more. Much has been written about metrics but the most important areas to focus on at the B are:

Growth rate: demonstrating the company is on a “triple-triple-double-double-double” trajectory is commonly acknowledged as the ideal path. While that is the gold standard, the reality is most companies are not going to be on that trajectory by the time they raise a B. And different companies hit their stride at different times. A more simple goal around the B, is that you should try to be growing at least 100% yoy to attract high quality investors.

Retention: High net dollar retention is what you will ultimately be judged on because that is, in the end, what matters most. But pay attention to gross dollar and logo retention as well. Some great barometers to benchmark against, depending on the underlying GTM motion and customer base are here and here.

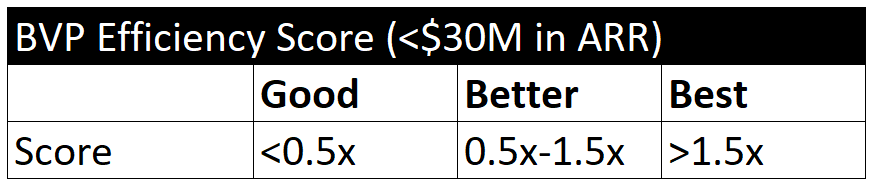

Efficiency: Both capital efficiency and sales efficiency (sub-category) are key operating levers to scale your business successfully beyond the Series B. Aim to have an efficiency score as close to 1 as possible and your magic number should likewise be around 1 as well. As I’ve written before, efficiency is even more important in today’s post-covid world.

Gross Margins: Most SaaS businesses are naturally blessed with high gross margins (80%+) — though those margins may take time to materialize. You may also have a hybrid model with multiple revenue streams. Showing high or improving gross margins at the Series B is important as it helps investors buy into the dream that your company can command high multiples at exit.

Running the Series B Process

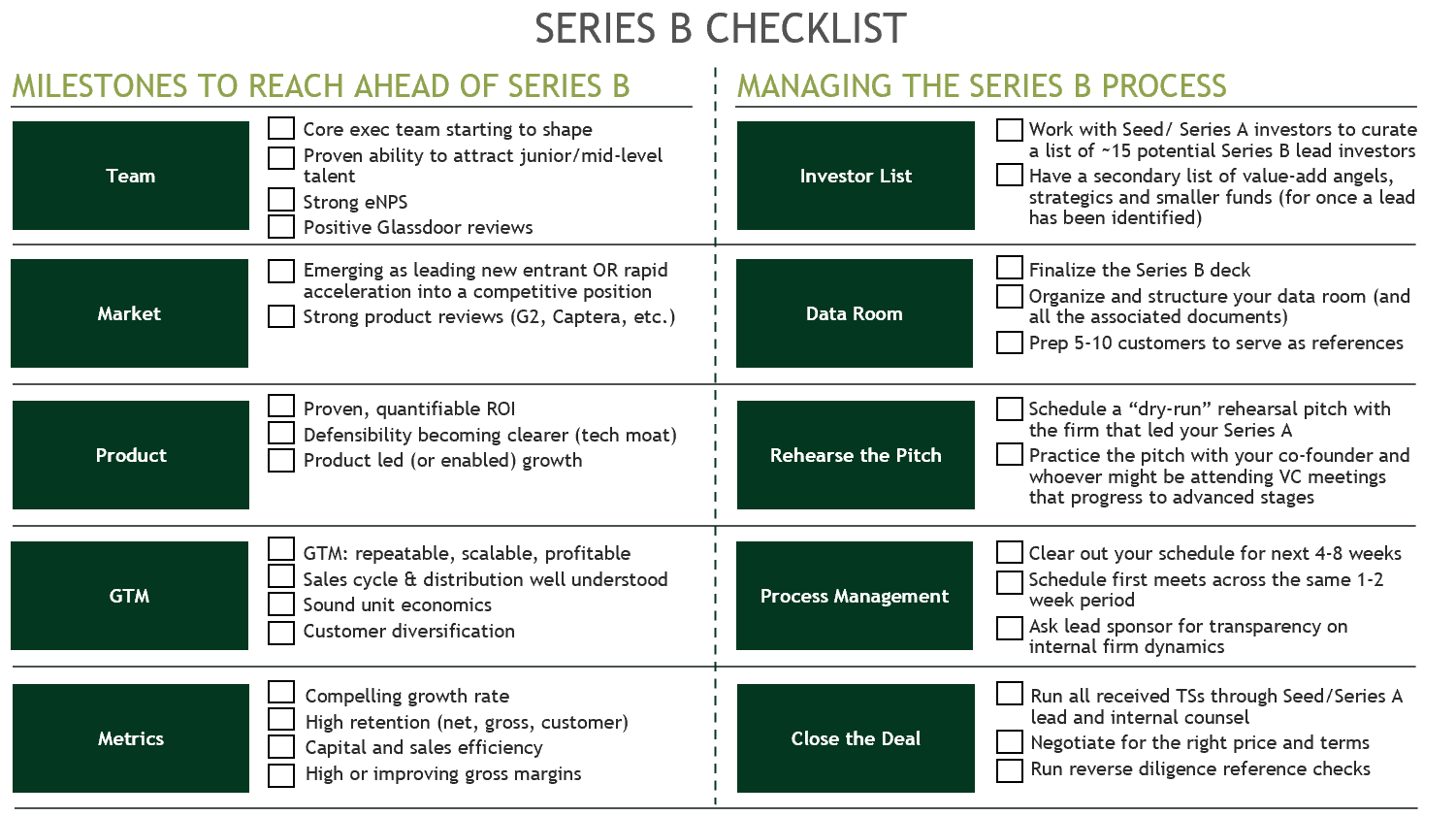

Now that we have covered the fundamentals of what you will be evaluated against at the B, let’s turn our attention to how to run an effective process. Don’t under-estimate the importance of running a tight and well-managed process. A successful raise is more likely to happen with careful planning.

Note: If you are 1–6 months out from raising a Series B, skip this first section and move to the next section: “Build the Right List of Investors.”

Backwards Plan

The first thing to realize is that as soon as the Series A closes, the “clock starts ticking” for the B round, which typically happens 18–24 months after the Series A — though timelines may stretch a bit longer in this current environment. When the Series A closes, start thinking about where you want to be when you raise the B. Some questions to ask:

What is the top-line ARR goal for a compelling B?

How much capital will be consumed between now and then?

What does net retention need to look like (and broader cohort trends?)

What is the target gross margin?

What are the key exec-level hires that need to be made?

What product milestones need to be hit?

Once you have the Series B goals written down and aligned with your team and Board, figure out the quarter-by-quarter plan to get there. Be thoughtful about what you aim to accomplish each quarter and hold yourself accountable to the quarterly milestones. The plan will change, but you are much more likely to have a successful Series B raise if you are deliberate about planning the journey to get there.

Build the “Right” List of Investors

Another important thing to do shortly after the Series A is to build a list of the right set of investors. Many founders end up wasting time talking to investors that are just not going to be the right fit for reasons that are “strategy-related” (e.g. stage or category.) For example, many Series A focused firms do not invest in Series Bs — check size is too high, ownership too low or valuation not in range for their strategy. Other, later stage firms, don’t do Series Bs — it’s just “too early.” If a firm is not investing out of a fund of at least $250M, they are unlikely to lead a Series B round of $20M+.

Some firms have areas they won’t touch (i.e. “we don’t do consumer.”) Others will only follow once a lead is identified. Corporate VCs/ strategics can add a lot of value, but may also take much more time. As a founder, you may also be inundated with inbound from various firms who are simply prospecting or doing research on a space. Bear in mind most firms invest in <1% of the companies they talk to. So taking meetings with lots of firms can be time consuming and distracting from the core business.

My suggestion is to “go deep, rather than broad.” Work with your existing Seed and Series A investors to craft a highly targeted list of ~10–15 firms worth getting to know more intimately. If you don’t have an existing relationship with those firms, have one of your investors provide you with a warm intro.

Allocate some amount of your time (but definitely <5%) to building deeper relationships with these firms over the course of 1–2 years — and specifically with the person at that firm who would be sponsoring the investment. This will allow you the opportunity to really assess whether they would be a good long-term partner. It also allows the investor to get to know you and to socialize the opportunity internally so that you are a “known entity” when it comes time to formally raise.

Create the Data Room

In the weeks before you decide to kick-off the formal raise process, you will want to have your data room fully structured and ready to go. Do not start the process before you have this in place! Frequently founders underestimate the pain caused when they prematurely kick-off a process and have 10–15 firms asking for different data items.

Create a single, well-structured data room with everything a firm could possibly want to know and have that ready to go. You will come off as more structured/together and will also limit the back and forth requests and internal scramble that comes with being less prepared. See below for an example of how to structure your data room and the items to put in each folder.

Another best practice is to have a “go-to” list of 5–10 customers who can serve as reference checks for investors. Have these customers prepped in advance of your fundraise. Try your best to spread the customer references around as no customer wants to spend their whole day talking to VCs — no matter how much they love your product!

Rehearse the Pitch

In the few weeks before you go out to formally raise, focus on practicing the pitch. This includes understanding timing (you will typically have 30–60 minutes) depending on where you are in the process with any given firm. You’ll have to understand pacing and how to deliver concise responses. We are also in a hybrid environment right now, so be prepared for a mixture of phone, video and (perhaps) some in-person.

Another important dimension is who to bring to the meeting. In the early parts of the process the founder/CEO should be doing the meetings 1:1 but as you progress, you’ll likely need to bring in co-founders and other key exec team members. Have a plan of who you are going to bring in and at what point in the process. The firms you are speaking with may make suggestions as you progress through their process. To minimize disruption to the team, ask for the level of “seriousness” before taking team member’s time away from the business.

I also highly recommend that before you go out to formally raise, practice the pitch with your earlier investors. When you do this, ask for a sub-group of the broader firm to round-out the perspective of your lead sponsor with fresh eyes. A good way to think of this is a 60-minute pitch session where you pitch the team on doing their pro-rata. Have your lead sponsor collect the feedback from the team and share it with you. Incorporate the feedback before you go out.

Manage the Process

Once you formally go out to raise, realize that this is your full-time job and will require 100% of your time/ energy to succeed. You will also likely need to designate someone on your team as a “diligence-point-person” (e.g. VP of Finance, COO, etc) to field requests from potential investors. So make sure to have a process in place internally.

In addition, be sure to create a timeline of when first meets happen, when you want to receive term sheets by and the steps in between. Try to keep all the firms you are working with on a similar schedule. If a few jump the gun, that could create a forcing function for others to catchup and accelerate their process, but it could also result in some firms getting turned-off by a fast process. Never create a false sense of urgency or exaggerate where you are in the process.

While there is a loosely similar process across firms, each firm runs their “deal pipeline” slightly differently. When it comes to getting a decision, there is an even broader spectrum (in some firms it’s totally up to the sponsor, in other firms there is a vote and at some places there is just 1 decision maker.) As you move further into the process with any given firm, ask the lead sponsor (your original point of contact) for clarity on process and how decisions get made. This will help you a) understand the steps to a TS and b) allow you to best position yourself to navigate internal dynamics.

In general, black swan events notwithstanding, good Series Bs happen in ~4–8 weeks from intro session to TS in-hand. Sometimes things can move much quicker — especially if you have an existing relationship with a firm. If the round is taking longer than that, there is likely low interest and you may need to re-think the strategy. Explained “Nos” (if you actually get an honest explanation) can be helpful in terms of adjusting the strategy. At the same time, don’t read too far into a pass because there are a thousand reasons for passing that are well beyond your control. For example, a firm has decided they have already made 1 bet in your space and don’t want to do another.

There are differing opinions on valuation, but in my experience, it is never a good idea to throw out a number when pitching VCs. If the number you suggest is too high, you can quickly turn-off an investor who might otherwise be interested. If an investor asks you what valuation you are looking for say something to the effect of: “We care more about finding the right long-term partner than optimizing around a specific number. We have made considerable progress since the Series A and hope for the Series B valuation to reflect the value accrued, but we will let the market set the price.”

Close the Deal

Once you have succeeded in getting a few term sheets, it’s time to evaluate and make the right decision. Remember you are going to be working with the firm you choose for the next 5–10 years, so choose wisely. The first thing to do is a hygiene check on all the terms. Have your legal counsel and Series A investor take a look and make sure there aren’t any problematic terms.

Many founders get caught up in maximizing valuation but be careful here — the highest price isn’t necessarily going to be the right fit long term. It’s totally fine to use the leverage of optionality but pick your battles wisely and make sure to prioritize accordingly.

You should also run your own diligence on the firm you are working with. Ask for the firms you are evaluating to provide founder references but also do your own back-channel diligence. Get on the phone and spend time understanding how the firm has historically behaved. How involved are they? Do they contribute meaningfully? Do they operate with a steady hand through the highs and lows of company building? Do other founders like working with them? Ask for examples — the more specific the better.

Concluding Thoughts