I’ve moved back to NYC! To be more specific, the suburbs of NYC — but I think that still counts!

When Liza and I found out early last year that we were expecting a girl we knew we would have to make a decision about staying in the Bay Area or moving back east. After a bunch of conversations, we made the move in late February and have been settling in much more smoothly than I had expected.

With some time now to reflect, I’ve been thinking a ton about the differences between the two cities. For reference, I spent ~6 years in NYC (Brooklyn and Manhattan) and then ~6 years in SF. So I feel like I can credibly claim to have somewhat of a balanced view on the “great debate” of which is better. Unsurprisingly, as with many things, the truth is…it depends.

Much has been written of course about the demise of SF — homelessness, drug abuse, crime, commercial vacancies, etc. All of this is true and all of it quite sad. Each year I was in SF was more or less worse than the prior year, accelerated by the pandemic in a way that was hard to fathom at the time. But since I left, and have had some space to reflect, I find myself rooting for SF to make a comeback. And I think it will. The reality is, even now, there is no place on earth that has done more to advance technology and innovation than that ~50 miles between San Jose and the Golden Gate bridge. The talent network effects there run deep. The “builder mindset” second to none. And there are enough people still there who deeply care about the city and bringing it back to where it ought to be.

When I first started in venture in 2017 in SF, it was pretty common to take every first meeting with a founder in person. Some of my fondest memories of SF come from the hours spent walking all over Jackson Square, SOMA, FiDi and South Park between meetings to unearth opportunities. Back then the entrepreneurial community was so incredibly concentrated in a few of these neighborhoods that you could meet 50–75% of founders within a 20 min walk of Market St. There was something quaint, almost familial about the whole thing.

Of course the pandemic and ensuing years have broadened access beyond the Bay Area. And that is a very good thing as innovation should never be isolated to one area nor founders unable to access capital and resources purely based on where they live. Still, there is something very special about SF…not to mention it’s a city of immense natural beauty.

Everyone I know who left SF the last few years did so largely for “push” reasons. For us, there was certainly some of that. But deciding to move back to the NYC area had much more to do with personal “pull factors” than anything else: it’s the center of gravity for my wife’s side of the family (hooray for free child care!), the schools here are excellent, we’ve found there to be a strong sense of community, etc. And much of this is simply a stage of life thing. Having a child changed our outlook, including what we started to optimize for on location.

I’ve now been back in NYC for a little over 2 months. It’s been fun re-acclimating. As a fintech-focused investor, NYC is very clearly emerging as THE winner in financial services innovation. It’s not bigger than SF just yet in terms of outcomes, but the slope of the line, as defined by fintech startup formation and pace of growth, is incredibly steep.

When I first moved here more than 10 years ago, there was effectively one fintech company in the city that had some buzz: Betterment. There are now dozens of other examples and more forming each month. Many fintech founders are relocating from SF to NYC (or opening up a second office here). This week there are 3 major fintech-related conferences happening at the same time. It’s pretty wild.

Suffice to say I’m excited to get plugged back in here, reconnect with some old friends and make a few new ones. Looking forward to saying “hi” if you’re in the area.

As a growth stage SaaS founder with $5–10M in ARR, you have much to be proud of. You have made it to a point <1% of all startups make it to. You have achieved product-market fit, real customers find value in your software, investors believe in your vision and you have grown from a few founders sitting at a kitchen table into a rapidly scaling team with org charts, all-hands meetings, and maybe even (virtual) company retreats! Looking back at the last 3–4 years, you have accomplished a lot and avoided many “near-death” moments. There’s a lot to be excited about.

But in the back of your mind, there is the next big looming hurdle to get through — the so-called “Valley of Death” that many a great SaaS startup has succumbed too. Somewhere in that $10–50M ARR range, many good startups destined for greatness peter out. Many things can happen. Maybe it’s existential: the market you were building for is not ready for your product, turns out to be smaller than expected or you are only able to appeal to a small segment. Perhaps the unit economics are not holding as burn ramps. Or maybe it’s a people issue: a key founder quit, or the leadership team just can’t scale.

Most of the time, however, the failure point post $10M ARR occurs when the GTM machine stops working. This post, which draws on my time advising growth-stage startups as a consultant and now as an investor, examines why this happens and what you, as a founder, can do to avoid the Valley of Death.

Sales Efficiency as a Key Symptom

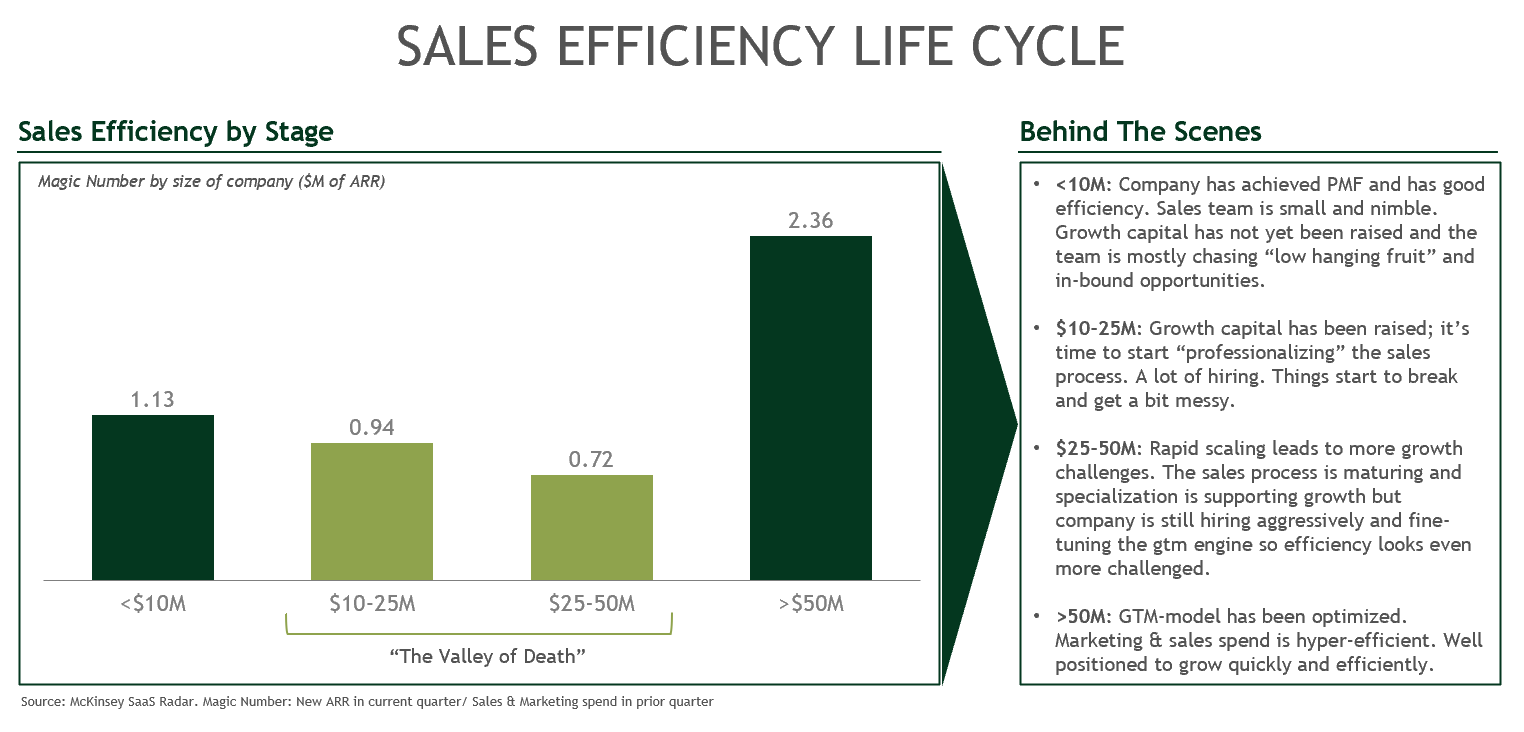

I have previously written about the importance of capital efficiency for SaaS businesses (see here.) More specifically, sales efficiency is the single most-telling operational metric for growth-stage SaaS businesses. To get through the Valley of Death, you need to maintain a high growth rate. Maintaining a high growth rate can’t happen without dollars spent leading directly to the new ARR. Sales efficiency (as measured via magic number), directly measures the ROI of sales and marketing spend on growth. McKinsey’s SaaS Radar has some great data on sales efficiency by ARR stage:

Let’s unpack what is going on here a bit further. In that “honeymoon” $5–10M ARR range, things are working very well on a micro-level. You are post-PMF and scaling efficiently for a few reasons. Your sales team is small and nimble; you are either doing founder-led sales or have a few reps who you have personally coached and have been there since Day 1. They are intimately familiar with the company and product and have high incentives to perform. Much of the opportunities you are hunting are new logos in that initial use case you designed the product for. It’s often a perfect match so the sales are easy; you may even have a fair amount of inbound based on referrals from early customers or people in your network. You have the normal startup twists and turns, but overall, things are peachy.

But somewhere around $10–25M in ARR, the sales efficiency starts to go down-hill. Part of this is a result of being in the “early growth stage” — you have raised that first growth round (see here on how to do it) and have started to invest in more sales and marketing headcount. New AEs take a quarter or two to ramp, you have to build out a real SDR program and you’re starting to think about investing in SalesOps to marry action with data. But other root causes behind this phase of growth are more troubling: perhaps that initial use case is starting to show limitations, maybe the product is hitting certain failure points thereby creating more churn, or perhaps the return on acquisition channels is worsening.

As the saying goes, it can often get worse before it gets better. The $25–50M ARR range can often look even more problematic from a sales efficiency perspective. Maybe the GTM and sales motion is starting to mature but the rapid hiring (ahead of growth) is masking the improvements. Maybe there is something external like new competitors or the TAM ends up proving to be more challenged. Regardless of the root cause, this can be a tough stage to be in — particularly since you have likely been focused on sales efficiency for at least a year or two and are not seeing the fruits of your labor.

The good news is that, if you are able to get through the $10–50M valley of death, things typically start to look a lot better on the other side of $50M in ARR. Companies that breakthrough this threshold are usually benefiting from a hyper-optimized sales & marketing engine and are able to grow quickly and efficiently. The magic number for companies that get here, on average, is greater than 2 — meaning for every dollar you are putting into marketing and sales, you are getting more than $2 in new ARR.

So the question then becomes: how do you navigate this valley of death to the hallowed lands of $50M+ in ARR? The key is to focus on high-potential levers that can improve sales efficiency.

5 Levers to Improve Sales Efficiency

There are many ways to improve sales efficiency in that $10–50M ARR range but the below 5 are likely the highest leverage actions you can take as a founder to increase sales efficiency.

(1) Hire an A+ VP of Sales/ CRO

The single highest leverage point you have as a founder to manage sales efficiency through the valley of death is to hire a strong VP of Sales or Chief Revenue Officer. Your headcount on the sales side is going to balloon and you will need a leader who can run a tight ship and work efficiently with other departments. In an ideal world, you would find someone who has all the attributes below:

He or she has lived through that $10–50M ARR window several times before and has built a career in your category or in a very close adjacent category (e.g. if you are a marketing SaaS startup, look for someone who was VP or SVP level at places like Hubspot, Marketo, Mailchimp, etc.) but is hungry to take on more ownership. This person would ideally have been a key leader in SaaS businesses that made it to $50M ARR, but if they were also with a company or two that failed to break-through that barrier that can also be useful in terms of lessons learned.

The sales leader also needs to have been responsible for building (not just managing) sales organizations from teams of 5–10 to 50+ in the past. They should know the traits needed in each role from SDR to AE to Manager and how to hire on the right cadence. If they can bring people with them from prior roles, that “followership” can help accelerate ramp time. Importantly, they should also have a healthy perspective on other key roles that could be used to support the front lines such as SalesOps and Account Management. Sales Ops, in particular, is an important data-driven role that every strong sales leader values and puts into place early.

The right VP of Sales/ CRO will also come in with a playbook on the sales process and the tooling required to build a robust GTM machine. They should know how to translate the product and sales knowledge living in your head into systematic policy and procedure that can be adopted by the broader organization. Beyond this, the sales leader should also have strong views on pipeline stage gating, pricing/ packaging, and people development.

Lastly, and perhaps most importantly, a good sales leader is a magnet for other top sales talent — be it sales managers, AEs, SDRs, etc. Attracting a high-quality sales leader can accelerate the overall talent pool and help you get where you are going faster and with fewer “people issues” along the way.

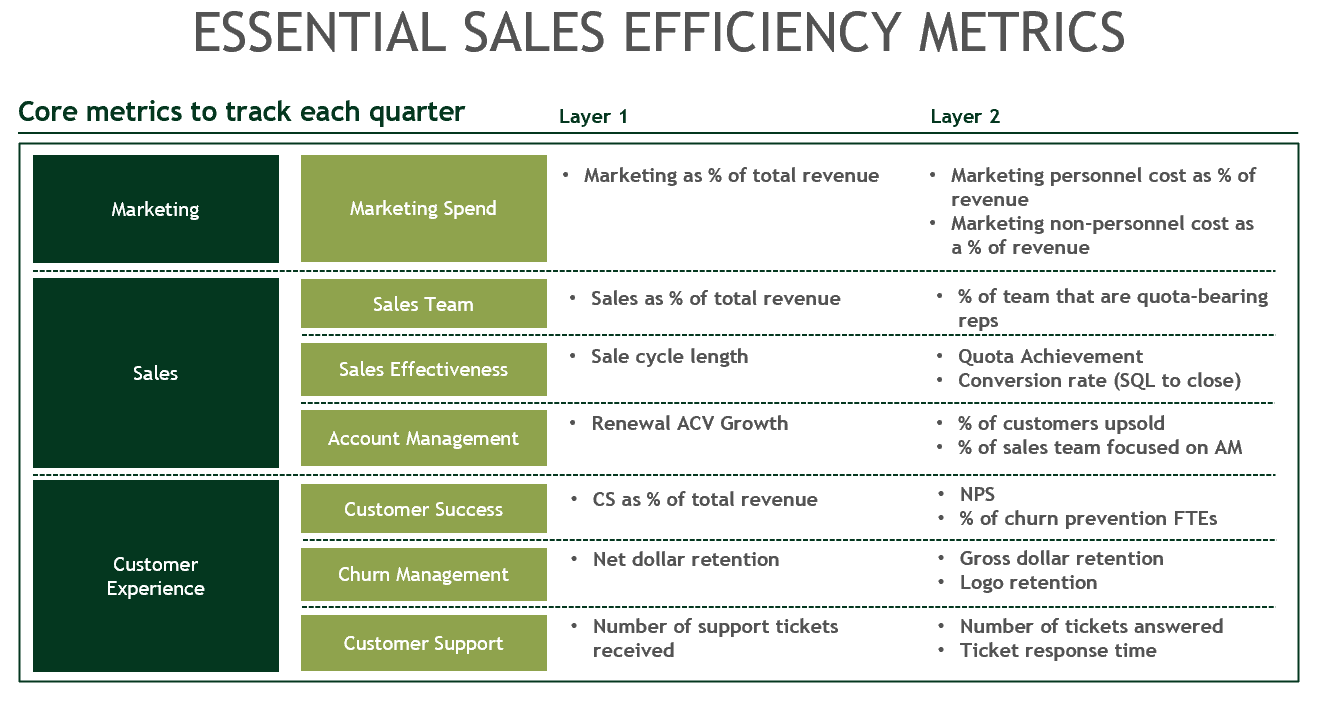

(2) Be religious about tracking core GTM metrics

Sales efficiency and more specifically magic number, in the end, is what you are trying to optimize. However, in order to do that, you really need to be tracking at least a few more layers beneath on a quarter-by-quarter basis. My suggestion is to break the GTM machine into its 3 primary orgs: marketing, sales, and customer experience. And then track at least 2–3 of the core metrics that impact sales efficiency (in addition to everything else you are tracking.)

You should also strongly consider investing in sales analytics software. Some of our portfolio companies have had great success with tools like People AI (revenue intelligence), Clari (RevOps) and Aviso (AI-powered selling.)

(3) Drive towards product-led growth + digital enabled sales

Long sales cycles, uncertain payback periods and choppy sales motions can impact sales efficiency negatively as they drive up sales and marketing costs without the benefit of incremental ARR. This can become especially magnified, early on, if you are selling to large enterprise customers, making it difficult to do other things like attract outside investors, decrease customer concentration risk and build a scalable/ repeatable playbook.

On the flip-side, if you have a bottoms-up motion, it will be pretty hard to accelerate through $50M in ARR without moving upmarket. Moving up-market works best if you have a land and expand motion (and typically with a freemium business model.) This allows the sales team to automate SMBs and move them to a self-serve/high-velocity motion (digital enablement) while refocusing the core sales team’s efforts upmarket. Nevertheless, never completely lose sight of the SMB segment as they are your growth engine and can help spur organic, word-of-mouth growth.

Regardless of where your customer base is today, every company should be focused on driving growth via product. Even the largest of enterprises, with their long sales cycles and complicated procurement processes, will accelerate their processes if they are seeing rapid adoption of their products “bottoms-up” by their employees. I saw this happen firsthand in my time at McKinsey where Slack and Box eventually upended decades-long relationships the firm had with IBM and Microsoft in the messaging and file-management categories. PLG can be a powerful force for overcoming inertia.

Digital enabled sales, which take a few different forms, can also lead to higher efficiency. Sometimes it’s a paired-down offering distributed on a self-service basis. In other situations, it is low-cost marketing and sales funnel that results in an inside sales motion. In both cases, digital sales can generate greater pipeline momentum than direct/ field sales as well as help you appeal to a broader customer base. This has never been more true than today in a post-covid world.

(4) Get as close to consumption-based pricing as possible

A close cousin of the PLG + digital-enabled sales strategy above is to push your pricing model towards consumption-based pricing. Consumption-based pricing, when done right, is the most efficient pricing model because it allows the customer to naturally expand as they consume more with very little incremental sales and marketing spend on your end. Consumption-based pricing is also the most value-based pricing scheme you can offer, which means the pricing levels tie closely with incremental value delivered. This allows for close alignment between you and your customers.

Some of the most sales efficient (and fastest-growing) SaaS companies employ consumption-based pricing. I’m including a few of my favorite examples of effective consumption-based pricing below:

Twilio: varies by product line but some examples are pricing based on the number of minutes to receive/make a call, number of SMS messages sent/received, etc.

Digital Ocean: pricing is based on the volume of data/bandwidth and the amount of time virtual machines are active

AWS: one of the original pioneers of consumption-based pricing, uses storage consumed (per GB) with volume discounts that come as you enter hire bands of data usage

Clearbit: all plans start with a $20K platform fee but thereafter pricing is based on CRM database size, web traffic, and monthly contact creation

Datadog: varies by product line but examples include per million log events, per 10k sessions, or per 10K test runs

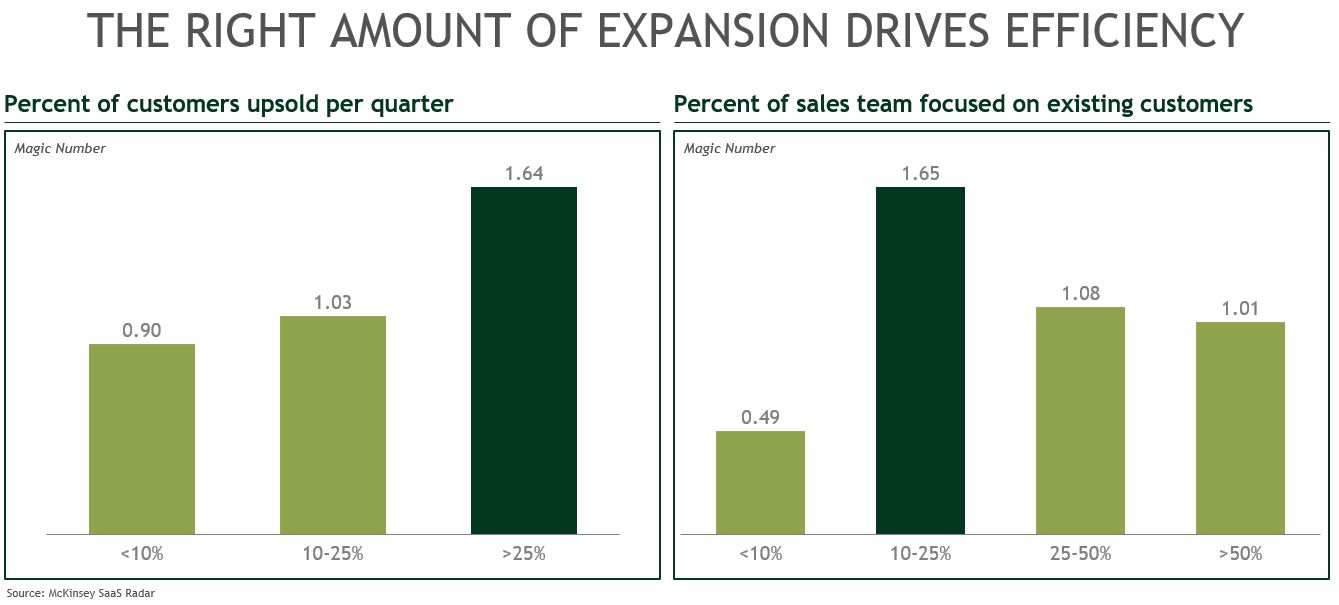

(5) Work the up-sell and cross-sell

The final strategy for improving sales efficiency is to mine existing customers. Generating incremental expansion dollars from your customer base is far less costly than acquiring a new logo. And the evidence shows that companies that expand >25% of their customers benefit from higher sales efficiency:

An important point here is that there is a “goldi-locks” level of attention that ought to be placed on the expansion of existing accounts — roughly 10–25% of your sales team should be focused on current customers. More than that and you will start to see diminishing returns and the effort is better spent on new logo acquisition.

Concluding Thoughts

Scaling through the valley of death and getting to 50M ARR is certainly no easy task. Very few SaaS businesses have made it through this phase of growth and the pitfalls that come with the territory. But hopefully, a sharp focus on sales efficiency, combined with the utilization of levers outlined above, will increase your chances of success.

As always, please reach out with any thoughts or suggestions (@MrAllenMiller). I’d also like to thank Kris Rudeegraap (@rudeegraap), Preeti Rathi (@preet1rathi), Sam East and Bill Macaitis (@bmacaitis) for their help in reviewing early drafts of this and providing invaluable feedback.

When I first landed in venture, it was with an early stage focus: predominantly Series A. The body of knowledge available to founders raising a Series A was pretty robust at the time thanks to investors demystifying a once opaque process via public blogs and forums. YC has since added even more transparency, creating a great Series A guide for founders looking to raise a Series A.

As I’ve move into a multi-stage environment (early + growth), I’ve been surprised by the dearth of information on fundraising for growth rounds, particularly that first growth round: the Series B. There are of course lots of good posts focused on metrics of all sorts, scaling in the growth stages, etc, but the existing literature doesn’t really cover how to raise a Series B — and certainly not in a tactical way.

This is particularly relevant in a post-covid world. If you look at the Pitchbook data from the last few quarters across stages, the story is quite interesting. Early stage deals (Series A) and late stage deals (Series D), saw a massive drop-off in dollars invested between Q4 ’19 and Q1 ’20 but then a decent sized recovery in Q2 ’20 (not all the way back but venture dollars returned 30%+ and the upward trend will likely continue into Q3 ’20.) Series Cs actually saw an acceleration through Covid.

The Series B round, however, while declining in a more measured way, continued a several quarter decline with almost no recovery from Q1 ’20 to Q2 ’20.

Source: Pitchbook

My hypothesis here is that the market is bifurcating around this new “ugly duckling” round — creating something like the Series A crunch of 2015. Why is that? At the Series A, investors can put in a relatively small check and get higher ownership to compensate for the risk taken. Not every Series A needs to work; high ownership in a few measured bets can return a fund making up for losses elsewhere.

In the later stage rounds (e.g. C and D), the winners start to become much clear and there is plenty of later stage capital ready to go to work into obvious winners. The returns in the later stages may not be as out-sized as at the A, from a multiple perspective, but a big check can return a sizable dollar amount at a decent IRR while ensuring investors are unlikely to take a 0 on any given investment.

But that first growth round (Series B) is becoming an increasingly difficult round for investors (and, consequently, for founders.) The company is perhaps somewhat de-risked from a PMF perspective but there are still substantial GTM and scaling questions that need to be answered. As such, Series B investors are forced to put fairly sizable checks to work ($20–$40M) without the ownership level of a Series A or the “certainty” of a later stage round. This becomes a bit more amplified in a post-covid world where there are even more unknowns.

This post is my attempt to shed some light on how to approach the Series B so that you can raise a successful first growth round.

A Quick Preface

Before we get started, because the letter of the alphabet can mean many different things to different people, I’ll begin by caveating what I mean when I say “Series B.” The profile for most companies going out to raise their first growth round (i.e. Series B) looks something like:

~$5–$10M ARR (though the range has become much wider on both ends)

To-date has raised anywhere from $5M to $25M (across angel, pre-seed/seed and A rounds)

Raising ~$20–$40M with a single lead or co-lead(s) doing the majority of the round

Has anywhere from ~2–4 years of financial history; company likely ~4–6 years old

Original founder(s) most likely still at the helm and running the day-to-day

This is, of course, overly simplistic as Series B companies have a broader range of profiles (so bear with me!) I will also assume a SaaS business model (though the learnings could be extrapolated to other B2B models, including hybrid models, which I have previously written about here.) I’ll also briefly mention that many of the lessons discussed below for the Series B also extend into later-stage rounds (e.g. Series C, D, etc.)

Building on the A

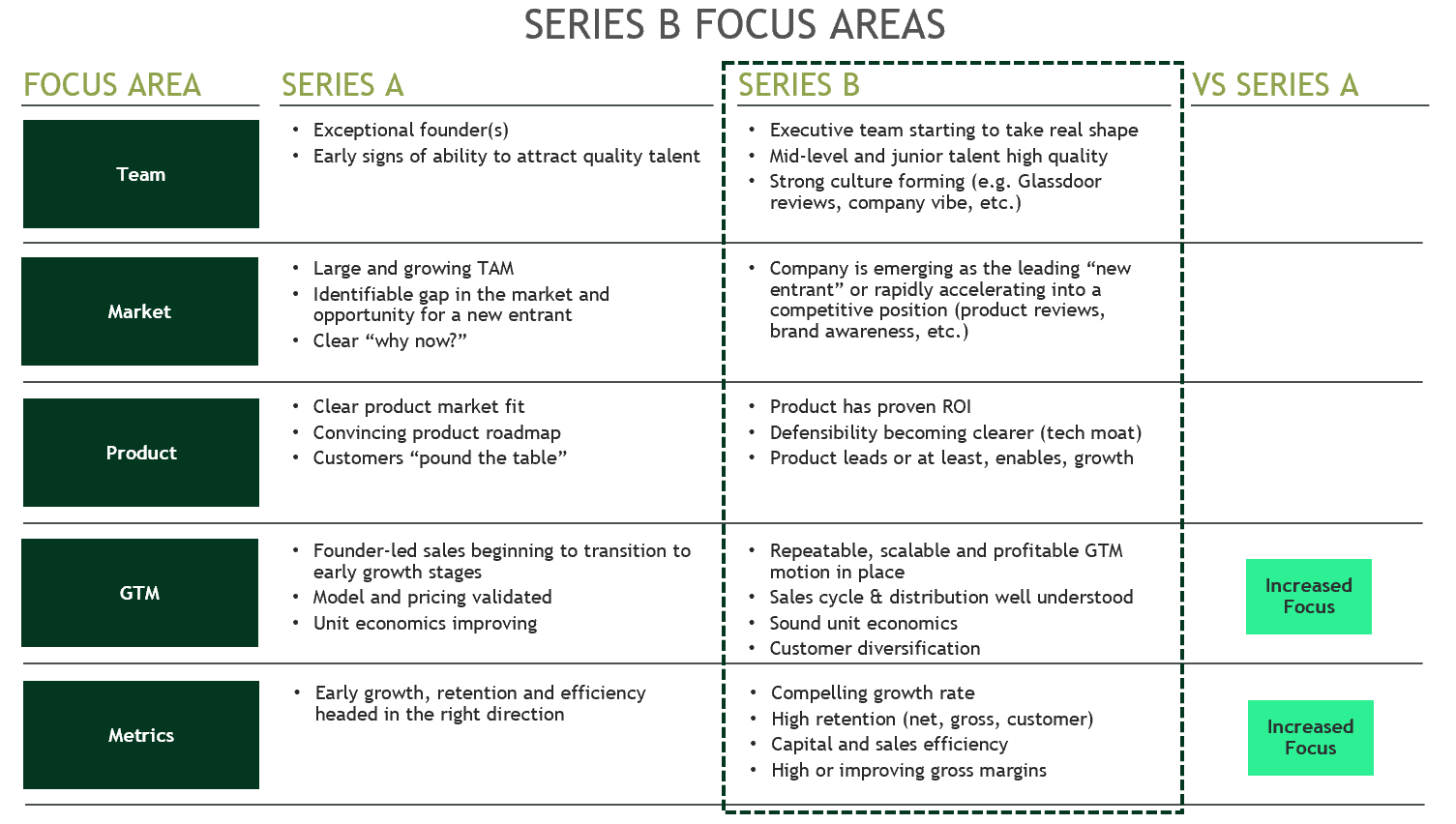

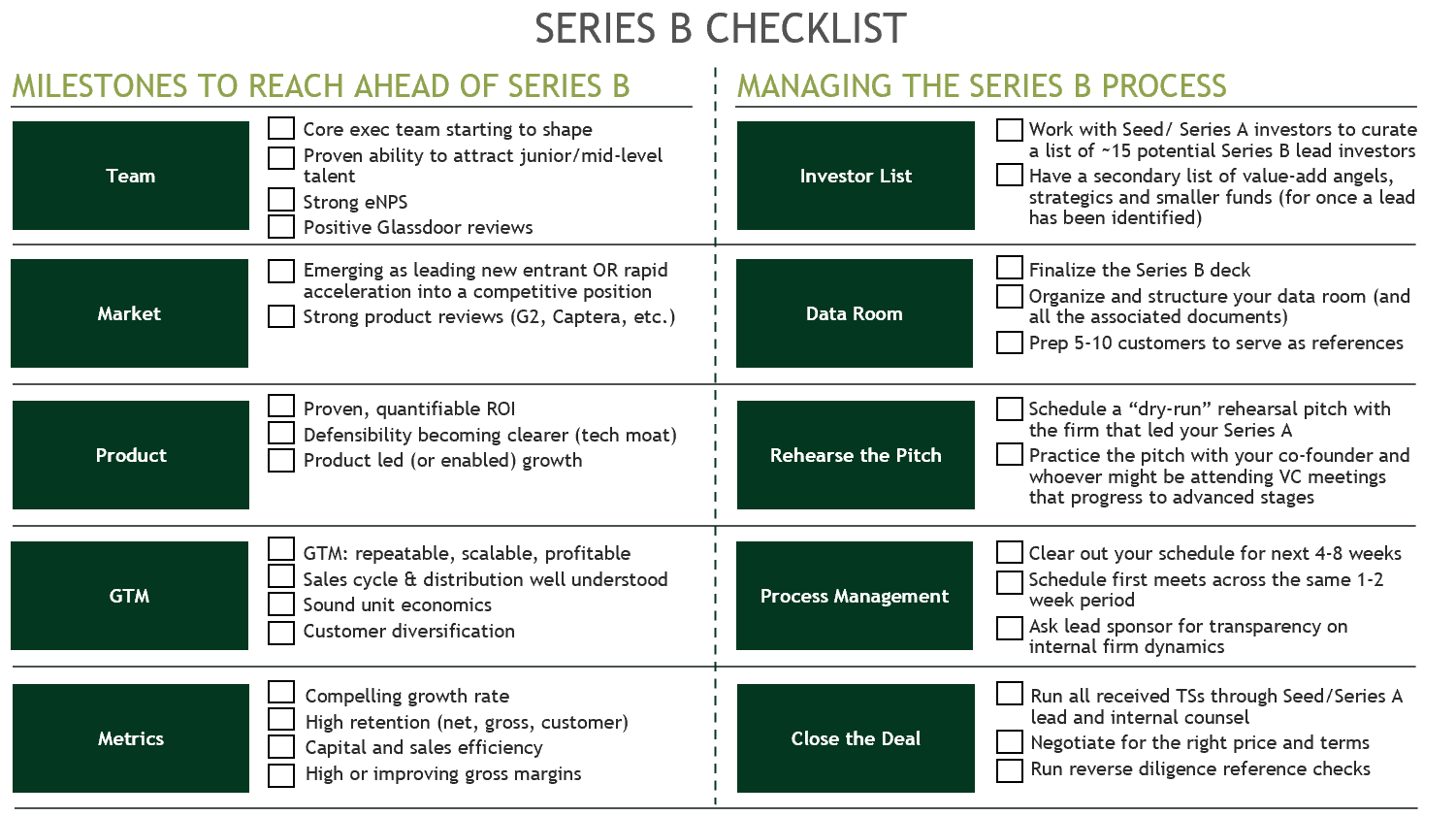

The best way to frame the Series B and how investors will evaluate your company is through the lens of “building on the A.” Most investors, generally speaking, focus on five key areas: (1) team, (2) market, (3) product, (4) GTM and (5) metrics. The first 3 have some additional features that build on what was established at the Series A while the latter two have a materially increased focus vs the Series A.

This is probably obvious: more time in the market means more data investors can analyze to assess whether a company has the potential to scale into an enduring brand. Let’s take a closer look at each of the 5 focus areas and how the Series B builds on the A.

Team

At the Series A, investors are looking for exceptional founders (passion, vision, grit, deep knowledge, charisma, etc.) There is a lot to unpack there but that is a separate post on its own! We are also often looking for early signs that the founders can attract high quality talent in the form of early team hires.

At the Series B, much more attention is paid to the broader executive team and how it is starting to shape up. In addition to assessing your ability to recruit great functional leaders, who have their own strong follower-ship, investors tend to start thinking in terms of “gaps that need to be filled” as part of the post-B phase of growth. Maybe you are at the point where you need a VP of Sales to lead GTM. Maybe the founder needs to transition product to a VP of Product to focus on other areas. Or maybe it is everyone’s favorite: time to hire that seasoned COO to support the young first-time founder!

The other area Series B investors will start to focus on is culture. Often by the B a distinct “cultural ethos” has started to form. Investors will try to glean what sort of vibe your startup has and how it is perceived in the market. This can be accomplished by spending time on-site at the office, looking closely at employee NPS and digging around to see what can be found “outside-in” via channels like Glassdoor. In a post-covid world, where in-person visits are now much harder, a company’s digital footprint will likely matter even more. Investors will also spend more time 1:1 with key executive leaders over video.

Market

When raising the Series A, the market story needs to be one of a large ($10B+) and growing (5%+ CAGR) TAM. There also needs to be some story around a gap in the market or a greenfield opportunity enabled by sleepy incumbents underserving some portion of the market (e.g. SMBs, developers, a new function like SalesOps, etc.) Articulating a clear “why now?” is also a very important part of the fundraise story.

At the Series B, investors will look for validation of the story you told at the Series A and whether the early momentum backs up that story. It is most compelling if your company is very clearly emerging as the market-leading new entrant. Investors will validate that by speaking with customers, reading product reviews from G2 and digging around on sources like Pitchbook and Google trends, to understand brand awareness and signal.

Product

Demonstrating early signs of product market fit at the Series A is paramount. In the end, this may be the single most important factor (outside of the founders) in determining a successful A raise. Investors will look for customers who “pound the table” and sticky enterprise user behavior. Beyond that, they will look at the road map to see if it is compelling and headed in a direction that matches the broader vision.

At the Series B, there are a few more product-components that matter. At this point, the product should show a clear and quantifiable ROI for the customer. There should be case studies and “customer-wide data” that demonstrate the ROI (whether it is cost savings, revenue lift or some other metric.) It also often helps if the product is developing in a way where there is a tech asset that creates a broader moat.

GTM

Relatively less attention is paid to GTM at the A. At that stage, founder-led-sales is common — though there may be some early signs of a transition to non-founder AEs. Typically the pricing and delivery model has been validated at the Series A. End-state unit economics (e.g. LTV:CAC, payback, etc.) are largely theoretical but improving quarter over quarter.

When you set out to raise the B, investors will be looking for a tighter story around GTM. They will look to see a scalable, repeatable and profitable motion in place. At this point you should have a pretty well understood sales cycle (e.g. how the funnel gets filled, how much time is spent at each point, what % convert, etc.) The unit economics that were theoretical at the A should be more proven-out at the B.

It is also really powerful if you have diversified the customer base. If moving “bottoms up,” for example, you may have a core startup-base of early adopters but now also have a strong set of mid-market logos, maybe even some 6-figure enterprise ACVs. You may have also started diversifying from one industry to several — this has become particularly important post-Covid when it has become clear that reliance on 1 vertical, even if performing well, can lead to a very false sense of security.

Metrics

Perhaps the biggest difference between the A and the B is that the availability of data makes the numbers matter a lot more. Much has been written about metrics but the most important areas to focus on at the B are:

Growth rate: demonstrating the company is on a “triple-triple-double-double-double” trajectory is commonly acknowledged as the ideal path. While that is the gold standard, the reality is most companies are not going to be on that trajectory by the time they raise a B. And different companies hit their stride at different times. A more simple goal around the B, is that you should try to be growing at least 100% yoy to attract high quality investors.

Retention: High net dollar retention is what you will ultimately be judged on because that is, in the end, what matters most. But pay attention to gross dollar and logo retention as well. Some great barometers to benchmark against, depending on the underlying GTM motion and customer base are here and here.

Efficiency: Both capital efficiency and sales efficiency (sub-category) are key operating levers to scale your business successfully beyond the Series B. Aim to have an efficiency score as close to 1 as possible and your magic number should likewise be around 1 as well. As I’ve written before, efficiency is even more important in today’s post-covid world.

Gross Margins: Most SaaS businesses are naturally blessed with high gross margins (80%+) — though those margins may take time to materialize. You may also have a hybrid model with multiple revenue streams. Showing high or improving gross margins at the Series B is important as it helps investors buy into the dream that your company can command high multiples at exit.

Running the Series B Process

Now that we have covered the fundamentals of what you will be evaluated against at the B, let’s turn our attention to how to run an effective process. Don’t under-estimate the importance of running a tight and well-managed process. A successful raise is more likely to happen with careful planning.

Note: If you are 1–6 months out from raising a Series B, skip this first section and move to the next section: “Build the Right List of Investors.”

Backwards Plan

The first thing to realize is that as soon as the Series A closes, the “clock starts ticking” for the B round, which typically happens 18–24 months after the Series A — though timelines may stretch a bit longer in this current environment. When the Series A closes, start thinking about where you want to be when you raise the B. Some questions to ask:

What is the top-line ARR goal for a compelling B?

How much capital will be consumed between now and then?

What does net retention need to look like (and broader cohort trends?)

What is the target gross margin?

What are the key exec-level hires that need to be made?

What product milestones need to be hit?

Once you have the Series B goals written down and aligned with your team and Board, figure out the quarter-by-quarter plan to get there. Be thoughtful about what you aim to accomplish each quarter and hold yourself accountable to the quarterly milestones. The plan will change, but you are much more likely to have a successful Series B raise if you are deliberate about planning the journey to get there.

Build the “Right” List of Investors

Another important thing to do shortly after the Series A is to build a list of the right set of investors. Many founders end up wasting time talking to investors that are just not going to be the right fit for reasons that are “strategy-related” (e.g. stage or category.) For example, many Series A focused firms do not invest in Series Bs — check size is too high, ownership too low or valuation not in range for their strategy. Other, later stage firms, don’t do Series Bs — it’s just “too early.” If a firm is not investing out of a fund of at least $250M, they are unlikely to lead a Series B round of $20M+.

Some firms have areas they won’t touch (i.e. “we don’t do consumer.”) Others will only follow once a lead is identified. Corporate VCs/ strategics can add a lot of value, but may also take much more time. As a founder, you may also be inundated with inbound from various firms who are simply prospecting or doing research on a space. Bear in mind most firms invest in <1% of the companies they talk to. So taking meetings with lots of firms can be time consuming and distracting from the core business.

My suggestion is to “go deep, rather than broad.” Work with your existing Seed and Series A investors to craft a highly targeted list of ~10–15 firms worth getting to know more intimately. If you don’t have an existing relationship with those firms, have one of your investors provide you with a warm intro.

Allocate some amount of your time (but definitely <5%) to building deeper relationships with these firms over the course of 1–2 years — and specifically with the person at that firm who would be sponsoring the investment. This will allow you the opportunity to really assess whether they would be a good long-term partner. It also allows the investor to get to know you and to socialize the opportunity internally so that you are a “known entity” when it comes time to formally raise.

Create the Data Room

In the weeks before you decide to kick-off the formal raise process, you will want to have your data room fully structured and ready to go. Do not start the process before you have this in place! Frequently founders underestimate the pain caused when they prematurely kick-off a process and have 10–15 firms asking for different data items.

Create a single, well-structured data room with everything a firm could possibly want to know and have that ready to go. You will come off as more structured/together and will also limit the back and forth requests and internal scramble that comes with being less prepared. See below for an example of how to structure your data room and the items to put in each folder.

Another best practice is to have a “go-to” list of 5–10 customers who can serve as reference checks for investors. Have these customers prepped in advance of your fundraise. Try your best to spread the customer references around as no customer wants to spend their whole day talking to VCs — no matter how much they love your product!

Rehearse the Pitch

In the few weeks before you go out to formally raise, focus on practicing the pitch. This includes understanding timing (you will typically have 30–60 minutes) depending on where you are in the process with any given firm. You’ll have to understand pacing and how to deliver concise responses. We are also in a hybrid environment right now, so be prepared for a mixture of phone, video and (perhaps) some in-person.

Another important dimension is who to bring to the meeting. In the early parts of the process the founder/CEO should be doing the meetings 1:1 but as you progress, you’ll likely need to bring in co-founders and other key exec team members. Have a plan of who you are going to bring in and at what point in the process. The firms you are speaking with may make suggestions as you progress through their process. To minimize disruption to the team, ask for the level of “seriousness” before taking team member’s time away from the business.

I also highly recommend that before you go out to formally raise, practice the pitch with your earlier investors. When you do this, ask for a sub-group of the broader firm to round-out the perspective of your lead sponsor with fresh eyes. A good way to think of this is a 60-minute pitch session where you pitch the team on doing their pro-rata. Have your lead sponsor collect the feedback from the team and share it with you. Incorporate the feedback before you go out.

Manage the Process

Once you formally go out to raise, realize that this is your full-time job and will require 100% of your time/ energy to succeed. You will also likely need to designate someone on your team as a “diligence-point-person” (e.g. VP of Finance, COO, etc) to field requests from potential investors. So make sure to have a process in place internally.

In addition, be sure to create a timeline of when first meets happen, when you want to receive term sheets by and the steps in between. Try to keep all the firms you are working with on a similar schedule. If a few jump the gun, that could create a forcing function for others to catchup and accelerate their process, but it could also result in some firms getting turned-off by a fast process. Never create a false sense of urgency or exaggerate where you are in the process.

While there is a loosely similar process across firms, each firm runs their “deal pipeline” slightly differently. When it comes to getting a decision, there is an even broader spectrum (in some firms it’s totally up to the sponsor, in other firms there is a vote and at some places there is just 1 decision maker.) As you move further into the process with any given firm, ask the lead sponsor (your original point of contact) for clarity on process and how decisions get made. This will help you a) understand the steps to a TS and b) allow you to best position yourself to navigate internal dynamics.

In general, black swan events notwithstanding, good Series Bs happen in ~4–8 weeks from intro session to TS in-hand. Sometimes things can move much quicker — especially if you have an existing relationship with a firm. If the round is taking longer than that, there is likely low interest and you may need to re-think the strategy. Explained “Nos” (if you actually get an honest explanation) can be helpful in terms of adjusting the strategy. At the same time, don’t read too far into a pass because there are a thousand reasons for passing that are well beyond your control. For example, a firm has decided they have already made 1 bet in your space and don’t want to do another.

There are differing opinions on valuation, but in my experience, it is never a good idea to throw out a number when pitching VCs. If the number you suggest is too high, you can quickly turn-off an investor who might otherwise be interested. If an investor asks you what valuation you are looking for say something to the effect of: “We care more about finding the right long-term partner than optimizing around a specific number. We have made considerable progress since the Series A and hope for the Series B valuation to reflect the value accrued, but we will let the market set the price.”

Close the Deal

Once you have succeeded in getting a few term sheets, it’s time to evaluate and make the right decision. Remember you are going to be working with the firm you choose for the next 5–10 years, so choose wisely. The first thing to do is a hygiene check on all the terms. Have your legal counsel and Series A investor take a look and make sure there aren’t any problematic terms.

Many founders get caught up in maximizing valuation but be careful here — the highest price isn’t necessarily going to be the right fit long term. It’s totally fine to use the leverage of optionality but pick your battles wisely and make sure to prioritize accordingly.

You should also run your own diligence on the firm you are working with. Ask for the firms you are evaluating to provide founder references but also do your own back-channel diligence. Get on the phone and spend time understanding how the firm has historically behaved. How involved are they? Do they contribute meaningfully? Do they operate with a steady hand through the highs and lows of company building? Do other founders like working with them? Ask for examples — the more specific the better.

Concluding Thoughts

Raising money is almost never a fun thing for founders. But the right founder/VC pairing can be a powerful acceleration to help you achieve your vision. Understanding what Series B investors look for and how to manage your fundraise is the key to success. Hopefully with a lot of careful planning and a little bit of luck, you will end up with a successful Series B outcome.

As a final parting thought, I’ve aggregated the thoughts above into a packaged view (“Series B checklist”) of the things to do before you raise your first growth round. Remember, you don’t necessarily need to have all of these checked off. But the more you do, the more compelling the round will be.

As always, please reach out with any thoughts or suggestions (@MrAllenMiller). I’d also like to thank Kris Rudeegraap (@rudeegraap), Michelle Palleschi, Rishi Taparia (@taps), Ricky Pelletier (@RickyPelletier), Parsa Saljoughian (@parsa_s), Preeti Rathi (@preet1rathi) and Lenny Rachitsky (@lennysan) for their help in reviewing early drafts of this and providing invaluable feedback.

Global FinTech investment in 2017 was unprecedented with $16.6B of capital (+20% compared to 2016) deployed across 1,128 deals. Despite this, some have argued that FinTech’s days are numbered and that it is less clear how much opportunity still remains for future innovation. Proponents of this line of thought argue that most traditional financial services have already been unbundled and that large startups that dominate areas like payments, lending, and investing have even begun to re-bundle services. Moreover, despite the uptick in investment into the sector, the early-stage portion of overall financing dropped to a 5-year low which has further supported the belief that most of the innovation in FinTech has already happened.

At Matrix, we believe that we are still in the early innings of the financial services disruption. While FinTech startups have done very well in the last decade, there is still room for more great companies to be built. As a follow-up to our previous article where we introduced the Matrix FinTech Index, we have put together a corollary to that piece where we specify 7 tailwinds that have powered FinTech innovation for the last 10 years, discuss key drivers for future innovation, and identify the subcategories we believe are most promising.

Review of 7 important tailwinds for innovation in FinTech the last 10 years

Mobile has been leveraged as an enabler: Companies like Squareleveraged mobile as a way to reduce the cost of doing business for merchants by allowing for new features like secure payments via mobile applications.

The financial crisis created unmet demand: Incumbent’s unwillingness to lend to credit poor individuals and high-risk SMBs created a window of opportunity for companies like Lending Club and OnDeck to fulfill this unmet demand.

The payments infrastructure opened up to developers: APIs and developer tools made available by companies like Braintree and Stripeallowed developers to integrate payment processing into their websites without the need to maintain a merchant account.

Online banking penetration unlocked important customer data: Deeper penetration of online banking has made it possible for companies like Yodlee to allow users to see all their banking information on one screen and others like Credit Karma to provide credit monitoring services.

Core financial services have been unbundled: Many sub-segments traditionally handled solely by the banks have been unbundled. For example, SoFi is helping with borrowing, Xoom with money transfers and Mint with financial management.

The cloud provided a new distribution channel to serve SMBs: Companies like Kabbage, which provides loans to SMBs, can now justify serving lower life time value customers like SMBs due to the lower customer acquisition costs associated with the cloud.

Digital disintermediation provided greater value to consumers: Companies like Wealthfront, Betterment and Robinhood all reduce the fees charged by brokerages and traditional investment managers providing greater alpha to retail investors.

Key drivers for innovation in the next 10 years

Many of these 7 trends will continue to play a role in FinTech innovation moving forward. But we have identified 3 additional drivers for innovation in FinTech going forward.

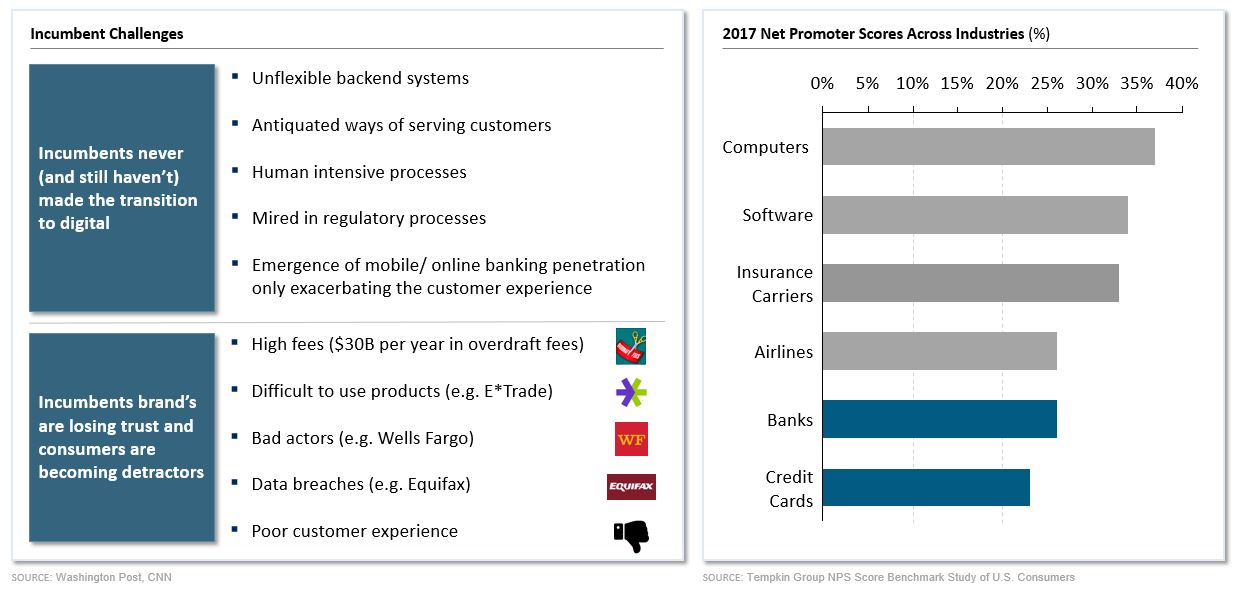

1. Incumbent failures are really coming into focus.

Traditional financial institutions are anachronistic. They serve their customers with antiquated products and are often slow to innovate due to both their size and regulatory burdens. Moreover, financial products have historically not been customer-centric, as banks devote most of their resources to optimizing their data and analysis and boosting their bottom line. Consequently, incumbents in financial services have largely failed to meet the needs of consumers, and the emergence of FinTech has put their shortcomings under the spotlight.

While financial services as an industry has been notorious for low consumer trust levels, consumer trust has plunged even further in the wake of fraud, scandals, and data breaches (e.g. Wells Fargo and Equifax). Additionally, poor customer experience has left consumers with limited loyalty to their financial services providers.

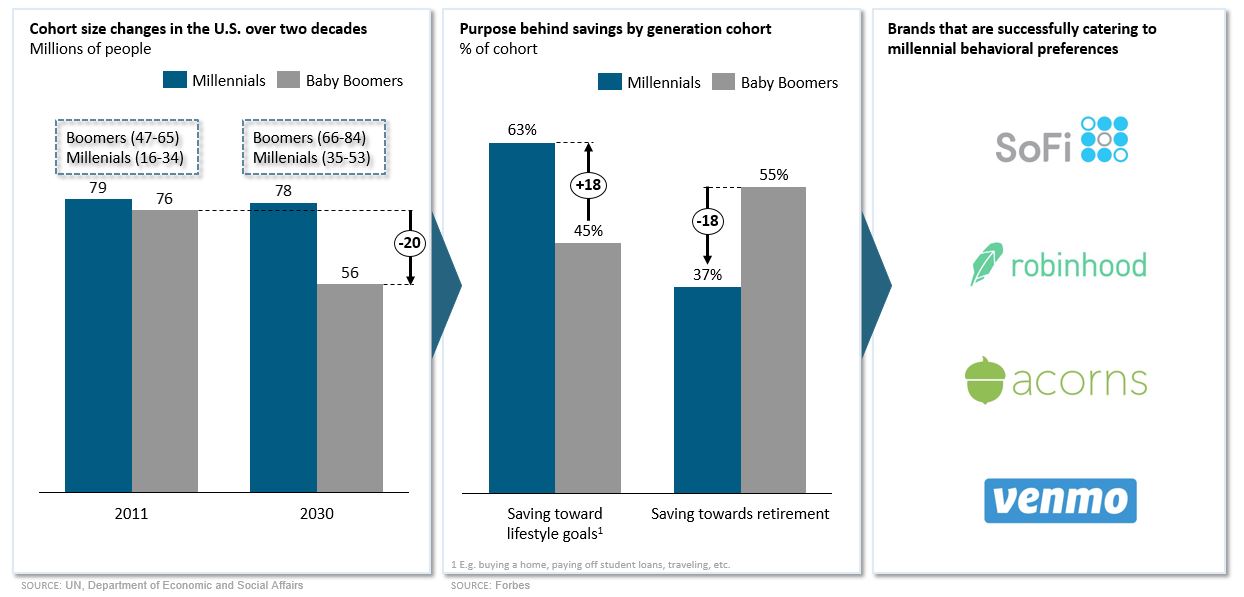

2. Millennials are emerging as the new source of spending power.

Millennials are the largest generation in American history consisting of over 70 million people born between 1980 and 2000. Millennials are digital-first users who grew up distrustful of banks and are generally more inclined to try FinTech applications. Furthermore, while traditional financial services has focused on large pools of wealth characteristic of older generations, FinTech innovation is making financial services and products much more accessible to younger generations.

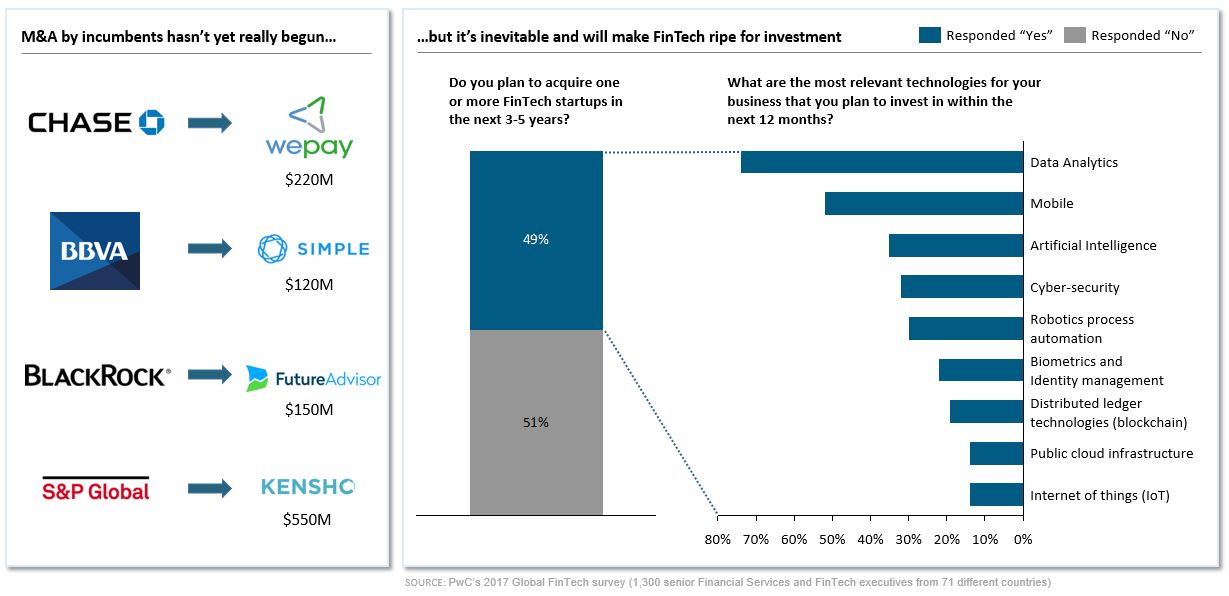

3. Due to the transition of profit pools, incumbents are going to become a lot more acquisitive in the coming months.

Incumbents have begun to acquire FinTech companies as a means to compete against innovative startups and other acquisitive incumbents. Many of the acquisitions so far have been centered around automation of basic tasks. In the last 5 years, 18 FinTech startups have been acquired by banks, with 8 acquisitions occurring since the beginning of 2017. We believe that there is much more opportunity and incentive to acquire — especially for technologies that go beyond automation.

5 subcategories we are most excited about

Ultimately we believe the incumbents will continue to lose ground to the FinTechs and that there is plenty of opportunity for entrepreneurs to build enduring companies in the sector. Great companies will certainly be built across the entire financial services industry, but here are a few sub-categories within FinTech that we think are particularly exciting:

Payments: Even with all the innovation to date in payments, there continue to be pain points throughout the category and many customer demographics remain underserved. In order to be successful in this category, new entrants will need to build on-top of existing payment rails, serve large TAMs and go after new use cases.

Investing / wealth management: Despite recent innovation by players like Wealthfront, Betterment, Robinhood and others, wealth management remains dominated by the incumbents. This reality makes the category a ripe one for entrepreneurs as there are large TAMs, poor customer experiences and a new generation (i.e. millennials) that have unmet needs. Success here will require intuitive design, low fees and efficient customer acquisition.

Infrastructure Apps: Financial institutions suffer from bloated cost structures in the middle and back office for tasks like fraud/ risk management, collections, invoice management and customer support. There’s an opportunity for entrepreneurs to provide software tools that reduce costs and allow for more efficient work flows if they can manage the lengthy sales cycles and procurement processes.

SMB tools: Companies like Gusto and Namely, have begun to serve SMBs in areas like payroll and benefits administration. Even so, SMBs remain largely underserved compared to larger enterprises. FinTech companies that can acquire SMBs efficiently and provide enterprise-level experiences will be able to generate enough value to their customers to create large outcomes.

B2B Lending tools: On the consumer side, lending has become pretty crowded with some of the winners already declared. But on the enterprise side, the category is very ripe. The opportunity for entrepreneurs is in leveraging data at cloud scale combined with advances in machine learning to allow enterprises to better assess borrower risk and drive higher yield.

The author would like to thank Sreyas Misra for his contributions to this piece.

In this fourth episode of Focus on the Founder, Jon Stein, Co-founder & CEO of Betterment joins us to discuss his career journey, experience starting Betterment while in business school and thoughts on wealth management and investing more broadly.

Jon Stein (Founder & CEO, Betterment)

Achieving Personalization At-Scale

Betterment is a robo-advisor platform that provides investment advice and wealth management at a low price point. The wealth management space is fiercely competitive. Startups like Betterment, Wealthfront, and Robinhood as well as incumbents like Vanguard and Schwab have all entered the space, competing to provide personalized, low-cost advice to consumers.

Since Betterment launched in 2010, their assets under management have grown rapidly, reaching almost $12 billion earlier this month. During this conversation, Jon discusses his experiences growing Betterment, and how Betterment has succeeded in such a competitive environment through truly putting the customer first. As always, you can find the full podcast episode on SoundCloud, iTunes, and Google Play.

Key Thoughts from Jon on…

The reasons behind founding Betterment:

While working for the First Manhattan Consulting Group, Jon advised some of the world’s largest banks and brokerages. In the process, Jon gained an insider’s perspective on how banks operate and serve their customers. His product-development engagements with banks typically involved working on the key aspects of their products such as default rates and internal transfer pricing. Notably, these larger players paid almost no attention to their customers during the product-development process, as they focused much more on optimizing their data and existing flows, which Jon found perplexing. While working in Australia, Jon encountered user-centric financial products not available in the US at the time, such as the mortgage-offset account which combines a traditional mortgage and deposit account.

These experiences helped frame the problem that Betterment aims to solve — that “the old way of managing money is broken.” Investment management should be held to a higher standard — one which focuses far more on consumers.

Building a team:

Jon committed to starting Betterment before starting his MBA at Columbia Business School. In the early days, building Betterment was a two-fold challenge — building the actual product and navigating the regulatory challenges of being an investment advisor.

Sean Owen, Jon’s roommate at the time, provided much of the early engineering expertise. Sean was a software engineer at Google who studied computer science at Harvard, and built the back-end of Betterment while Jon worked on the front-end. Jon eventually met Eli Broverman during a weekly poker game. Eli, who was then a securities attorney, provided the legal expertise and helped Jon navigate through complex regulatory landscape. Sean and Eli’s skillsets were diverse and congruent with the early challenges that Jon needed to solve.

The fundraising journey:

Betterment launched at TechCrunch Disrupt in 2010, where they competed against 500+ entrants, many of which had already raised some amount of funding. Betterment went on to win the competition, giving him crucial exposure to customers and investors. Immediately following the competition, Betterment signed up 400 new customers, who helped drive Betterment’s initial organic growth by way of referrals. The boost in credibility from the event made it easier to hire new employees, and helped Betterment rapidly grow from what was at the time a four-person team.

Just as important, preparing for the Disrupt presentation helped Jon and his team internalize their story and understand how to best pitch the idea. A month following the TechCrunch competition, Jon was able to raise $3 million from Bessemer Venture Partners.

How Betterment puts customers first:

Since the initial investment from Bessemer, Betterment has secured $275 million in funding and has grown significantly in employee count and AUM. In this period of growth, Jon doubled down on the theme of bringing the voice of the customer into every interaction. This focus has helped Betterment withstand the test of time and compete effectively against a host of startups and incumbents offering similar services.

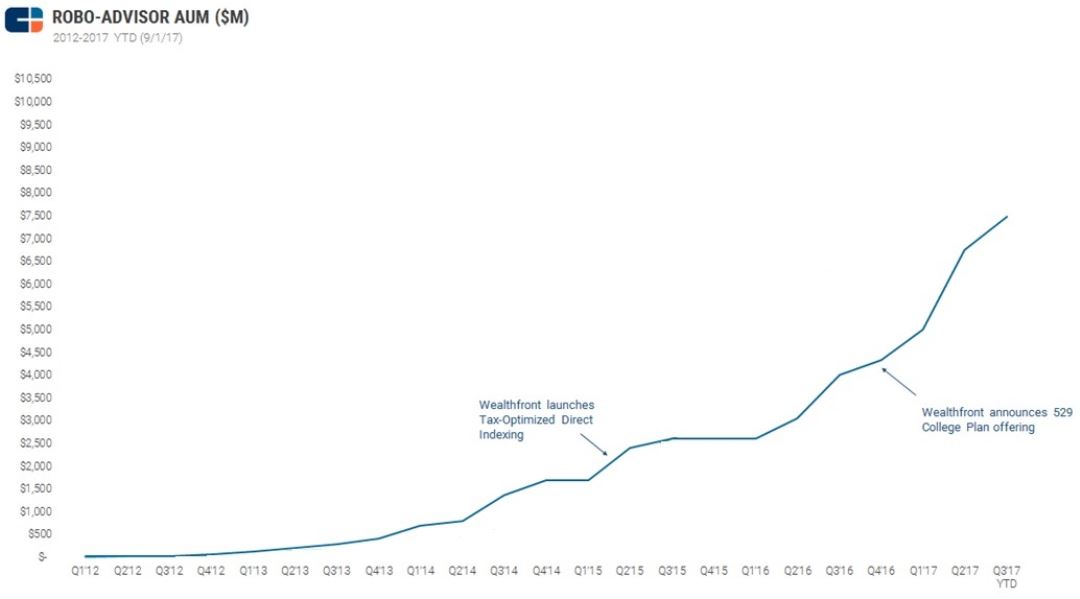

Private Robo-Advisors in the Wealth-Technology Category

Source: CB Insights

Betterment puts the customer first by:

1. Personalizing advice

Betterment’s vision is to provide excellent financial guidance that is easy to understand and available to everyone. Betterment is unique in that it offers a spectrum of interaction-types: customers who prefer human interaction can receive hybrid-robo solutions through Betterment’s unlimited text messaging and premium telephone access services. By prioritizing the education of their end-user, Betterment offers a suite of solutions to improve consumer-access to financial markets.

2. Building trust

Financial services as an industry has historically had a low NPS. Betterment strives to build trust with its customers as both an ethical obligation and a means of differentiation. In addition to investment advice, Betterment publishes scores of articles helping consumers understand their personal finances, navigate through tax reform, and manage their expenses. Betterment also has no holdings of their own; thus, they eliminate many of the conflicts of interest present in most banks.

3. Combining responsibility with wealth creation

Betterment offers a way for consumers to hold well-diversified portfolios that are also socially responsible through their socially responsible investing (SRI) portfolio. Social responsibility doesn’t just afford Betterment an additional dimension of personalization; it also reflects well on their brand as an ethical investment advisor.

The future of investment management:

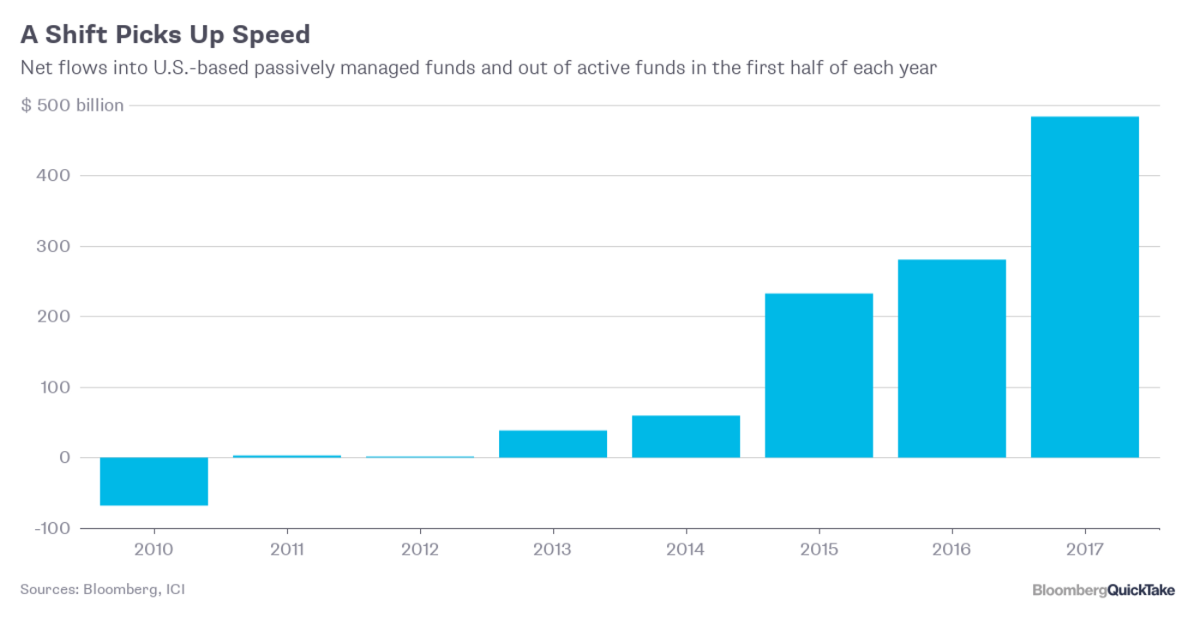

In this bull market, massive amounts of capital have been pushed into indices and ETFs, which represent a little over 10% of the global equity market capitalization. In fact, these indices and ETFs, spearheaded by firms like BlackRock and Vanguard, have outperformed an overwhelming majority of hedge funds.

Net flows into U.S.-based passively managed funds and out of active funds in the first half of each year

Source: Bloomberg, ICI

Jon explains that Betterment is here to stay even in increasingly likely bear market scenarios, as the same principles of minimizing cost and managing tax burdens that currently power Betterment’s platform still apply during downturns. Through careful risk-management, alternative investment strategies, and optimizing customer behavior to prevent market panic, Betterment aims not only to protect its customers in bear markets but also provide them competitive returns.

In the third episode of Focus on the Founder, I sat down with Shivani Siroya, the Founder and CEO of Tala. Shivani’s background comprises a unique mix of experiences in global health at the UN Population Fund and traditional investment banking at Credit Suisse, UBS, and Citi. In 2012, Shivani started Tala, then known as InVenture, to address some of the economic challenges she observed in Africa and Asia while working for the UN.

Shivani Siroya (Founder & CEO, Tala)

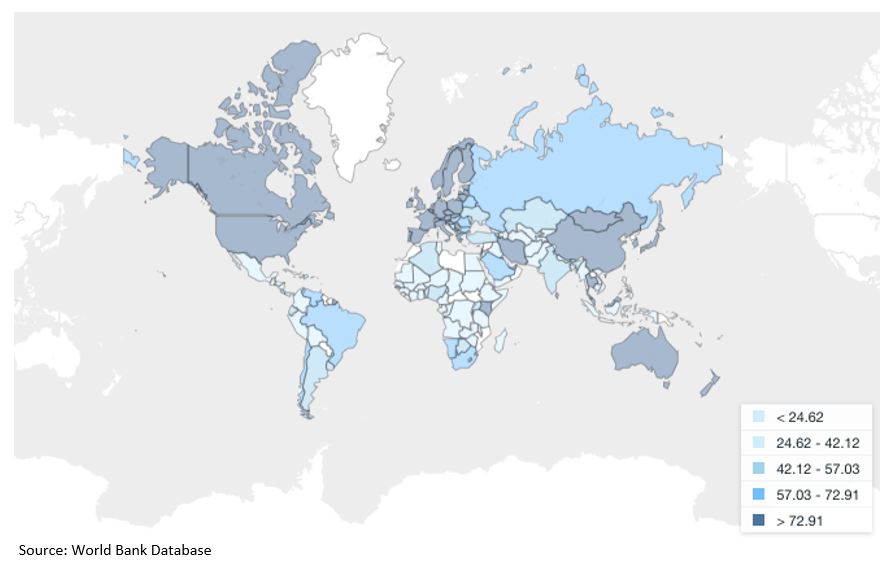

Tala as a Solution to a Global ProblemTala is a mobile-technology startup based in Santa Monica, CA that enables underserved people in emerging markets to access conventional financial services. Targeting an estimated population of 2 billion people, Tala’s smartphone-lending app delivers credit to borrowers with little-to-no financial history by using thousands of mobile data points to calculate an alternative credit score. The company has already disbursed over $225M in credit via 4.6 million microloans to borrowers across East Africa and the Philippines, and has plans to expand into Latin America and Southeast Asia.Percentage of population (% ages 15+) with bank accounts, by countryIn this conversation, Shivani discusses her experience growing Tala and the challenges and opportunities of bringing financial services to the underserved. YYou can find the full podcast episode on SoundCloud, iTunes, and Google Play.

Key Thoughts from Shivani on the…

Reasons behind founding Tala:

Shivani created Tala to solve a real problem. While at the United Nations Population Fund, she helped develop costing models and conducted thousands of interviews across multiple countries in Africa and Asia. Over this period, she witnessed the same problem occur: large populations of responsible, hard-working people who were unable to take out a loan due to lack of any financial history. Her decision felt “almost unconscious” simply because this was a huge problem that someone had to solve.

Creation of a new market:

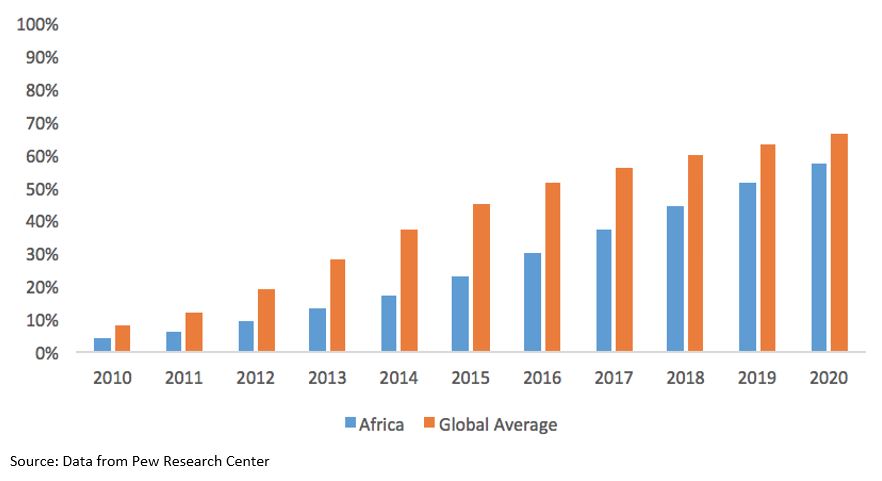

Because Tala attracts customers that are largely not covered by credit bureaus and lack access to traditional banking, Shivani explains that Tala’s Total Addressable Market (TAM) is about 2x that of a traditional lending company. Furthermore, by allowing borrowers to register with their smartphone and receive credit in a matter of minutes, Tala’s transformative user experience takes advantage of rapidly rising smartphone usage in emerging markets.

A Projected Upsurge in Smartphone Ownership in Emerging Markets

When choosing early adopter regions, Tala takes into account factors like political infrastructure, regulatory concerns and currency fluctuations — in addition to smartphone penetration.

Benefits and challenges of leading a distributed team:

Tala employs 165 people divided across three offices in Santa Monica, Manila and Nairobi. Because Tala has a global vision and is a customer-centric company, Shivani explains that Tala is required to have a distributed team to stay close to the customer. Hiring both engineers and customer-facing employees across all locations, Tala is able to track and serve the needs of an incredibly diverse user base. Proximity has proven especially critical to acquiring customers in close-knit communities. While Tala’s primary acquisition channel is digital (e.g. Facebook, Google AdWords, and Twitter), their organic traffic has been largely driven by referrals, radio, comment boards, and offline campaigns. Thus, a distributed team-structure has helped Tala achieve above 90% month-over-month growth in loan origination across all markets.

Leading a distributed team does not come without challenges. Research has found that distributed teams often suffer from communication barriers, differential knowledge bases, and inconsistent value systems. To overcome these hurdles, Shivani has:

Instituted a core-set of founding principles that pervades across all three offices

Required that all employees contribute to user research and be transparent about customer insights

Conducted all final-round interviews to ensure a common cultural thread between all hires

Made office managers travel quarterly to the other company locations

Split between balance-sheet and marketplace lending:

When Tala enters a new market, the company lends off of its own balance sheet as they gather customer data and develop and localize their credit models. As data is gathered and Tala’s models become more predictive, Tala moves more toward lending from a debt facility backed by traditional institutional investors and high net worth individuals.

Data-driven approach to Loan Financing:

Tala collects 10,000+ different data-points from a user’s smartphone to calculate an alternative credit score. Users are debriefed on how their data is utilized and can limit how much they share with Tala by toggling privacy options by data-category.

Shivani argues that tracking metrics as varied as financial transactions, social network diversity, and relationship stability, paint a more complete picture of a borrower’s riskiness compared to traditional credit-score inputs. Moreover, while some microfinancing options have been known to offer exploitative interest rates, Tala carefully customizes loan sizes and terms to their customer’s financial needs and risk tolerances. In addition, Tala differentiates on the speed dimension — approvals are instant, and most customers receive credit in less than 5 minutes. As a result, Tala has kept their repayment rates above 90 percent, and more than 95% of Tala’s first-time borrowers return for additional loans.

In addition to individual-level factors, Tala also considers macro-effects such as unemployment rates, purchasing power, GDP, and political instability.

Penetration of crypto-currencies and blockchain in the developing world:

Shivani explains that while the markets in which Tala is involved have not experienced much penetration by cryptocurrencies, Tala has started to investigate crypto as a means of currency exchange and moving capital. Furthermore, Shivani envisions that blockchain might play a crucial role in allowing Tala’s users to transition from a country-specific to a global financial identity.

The full overview of the Matrix FinTech Index is available on TechCrunch here.

Over the course of the last few years, FinTech as a category has really taken off. Five years ago the term ‘FinTech’ was not something most people had heard of other than a few early players in the startup ecosystem.

Today, FinTech is ubiquitous. In fact, the term has become synonymous with innovation in financial services — it’s hard to imagine a world without Paypal, Venmo, Square and many others. The Google Trends chart below describes this explosion in FinTech interest best.

Definition: Matrix considers “FinTechs” to be (a) technology-first companies that leverage software to compete with traditional financial services institutions (e.g. banks, credit card networks, insurers, etc.) in the delivery of traditional financial services (e.g. lending, payments, investing, etc.) or (b) software tools that better enable traditional finance functions (e.g. accounting, point-of-sales systems, payments, etc.)

Methodology and Results

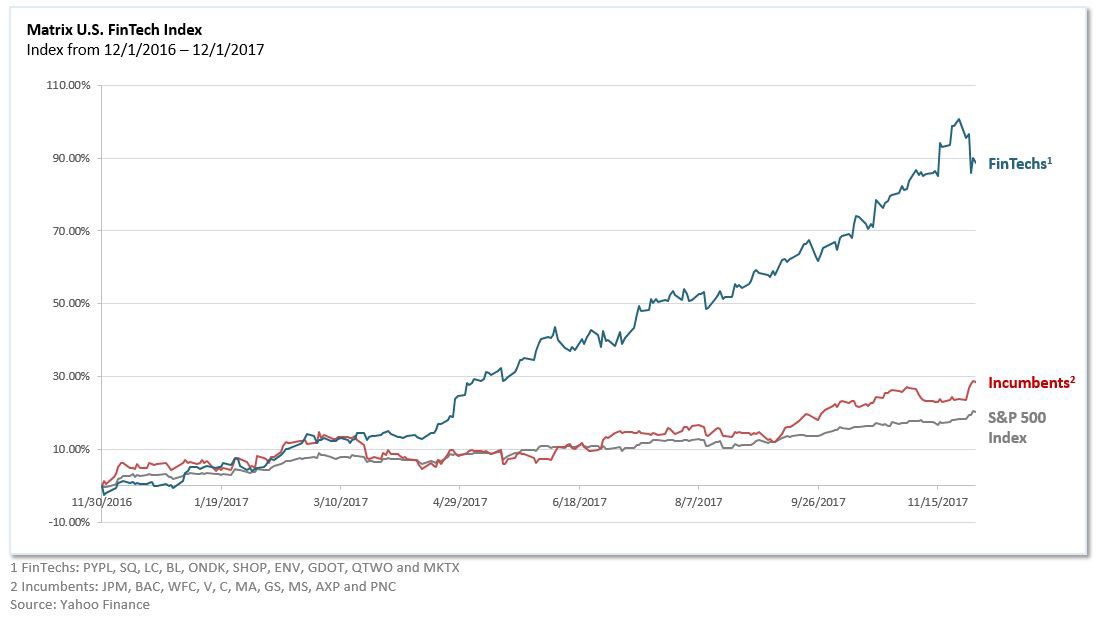

With an eye towards tracking the progress of disruption in the financial services space, we’re excited to release the Matrix U.S. FinTech Index today.

This market-cap weighted index tracks the progress of a portfolio of the 10 leading public FinTech companies over the course of the last year (beginning in December of 2016). For comparison, we have also included another portfolio of the 10 largest financial services incumbents (companies like JP Morgan, Visa and American Express) as well as the S&P 500 index.

As seen below, the Matrix FinTech Index shows a clear win for the FinTechs, who have collectively delivered 89% returns in the last 12 months. This is 60 percentage points higher than the 29% returns delivered by the incumbent portfolio and well above the S&P 500 Index.

Additional Data Now Available

Our hope in the coming months is to provide periodic updates to this Index. In addition, we are releasing a data package that anyone can download here that has a range of other helpful information on both the FinTechs and the incumbents. More specifically, the package includes:

Market cap and stock price data over the last year for the companies in the index

Comp sheets that include financial metrics on the public companies

Summary data on private FinTech companies valued at over $1B

Finally, this index is dynamic — we fully anticipate that it will be tweaked and refined in the coming months. Please feel free to send us your thoughts and feedback as we refine the process and methodology.

In this second episode of Focus on the Founder, I sat down with Ashley Johnson the COO/ CFO of Wealthfront. Ashley has a really interesting career as both an investor and operator. The first part of her career was spent largely as an investor at Morgan Stanley and then at General Atlantic, where she sourced investments in ServiceSource and RenRen. Both of these companies are now publicly traded. Ashley then ended up joining ServiceSource, where she held the CFO and CCO roles, before joining Wealthfront as COO/ CFO.

* * *

Wealthfront’s Growth Trajectory

Wealthfront has been on a very solid growth trajectory since its founding nearly a decade ago. The rob-advisor, which was founded by Andy Rachleff and Dan Carroll in 2008, now manages over $7B in AUM and has well over 100,000 accounts. And they are very well funded, having raised a total of $130M with a valuation (from 2014) of $700M.

During this conversation, Ashley discusses: the arc of her career, her initial priorities as the new CFO at Wealthfront back in 2015, the recruiting strategies the company employs and much more. The full podcast episode is available on SoundCloud, iTunes & Google Play.

* * *

Key Thoughts from Ashley on the…

Qualities she was looking for in potential investment opportunities

Two of Ashley’s more notable investments were ServiceSource and RenRen. In both cases the companies’ combined three key elements that she (and General Atlantic) really valued in potential investment opportunities: (1) extremely passionate founders, (2) clear product-market fit and (3) a highly defensible business modelwith high gross margins.

The capital General Atlantic provided then went towards very specific uses that accelerated growth and allowed for great outcomes. In the case of ServiceSource, the capital went to building out a sales team. In the case of RenRen, the capital injection was used to do a number of small acquisitions.

Areas where she was able to add value as an investor

The key value General Atlantic was able to bring to ServiceSource was expertise in understanding how to build out a really strong Sales team. This included bringing Jim Madden, a global leader in inside sales, customer success and growth, onto the board of the company.

At RenRen, the company’s leadership in China was able to benefit from the lessons learned by General Atlantic’s knowledge of the US social media market. General Atlantic was also able to help RenRen navigate regulatory hurdles — namely ensuring licenses were current with the various ministries in China, which provided the company with a big competitive advantage over other early players in the space.

Transition from investor to operator

Ashley compares the transition as going from an individual sport (investing) to a team sport (operating). One of the first lessons she learned, while trying to determine sales comp as ServiceSource (which she joined after General Atlantic’s investment) is that you can’t operate in a vacuum when running a business as you might be able to do to do as an investor. Instead, you need to apply a 360 degree approach around communication across teams. Otherwise the outcome, as she experienced first hand (and elaborates on in the podcast), isn’t great.

Key priorities for her when she first assumed the CFO role at Wealthfront

When Ashley joined Wealthfront in 2015, the company had just blown by $1B in AUM and was growing quickly but lacked the key processes and structures of a more mature company. Her first order of business was to build out a team for the finance organization. The second priority was to turn their venture funding ($100M on the balance sheet at that point) into a strategic asset and put in real structures in place around how to think through the uses of that cash and how to best allocate it across the organization.

Recruiting during periods of rapid growth

At Wealthfront, recruiting is viewed as a strategic function and they have invested heavily in building out a strong internal recruiting team. When evaluating candidates, the #1 most important criteria is excitement and passion for the Wealthfront mission.

The five operating principles they have maintained at Wealthfront, enabling them to maintain a strong culture during this period of hyper-growth, include:

1. Work with a sense of urgency

2. Ensure that decisions, even if tough, are made quickly

3. Debate and disagree initially but commit to a single path in the end

4. When disagreeing, do so respectfully

5. Always assume the best intent

Competing with the incumbents in wealth management

Wealthfront knows that it can always be outspent by the incumbents from a paid-marketing perspective. Moreover, one of the key metrics they look to adhere to is a 2-year payback period, which makes excessive marketing impossible. Instead they focus on leveraging millennial’s disdain for the incumbent brands, a superior product and a better overall customer experience to win against the incumbents.

Cryptocurrency market and Wealthfront’s position from a product perspective

If you’re hoping to add bitcoin to your Wealthfront portfolio, you will be waiting for quite some time. While many of Wealthfront’s customers are invested in crypto currencies, the firm is largely bearish on these assets in the long run. So don’t expect any exposure to crypto currencies from them anytime soon.

The gender gap in saving and investing

Women, especially in the 18–33 demographic, are less likely to save and invest than their male counterparts. In fact, Ashley wrote an article in Fortune a few years back encouraging more women to start taking saving seriously.

Her belief is that the lower savings rate is driven by 3 components: (1) lack of awareness, (2) lower confidence in finance related topics and (3) patronizing messaging in the industry. Wealthfront aims to be more inclusive by making their messaging universally relatable and accessible.

* * *

The conversation we had around Wealthfront and FinTech more broadly was certainly enriched by Ashley’s wealth of experiences on both sides of the table. A big thank you to Ashley for joining us — we look forward to seeing what’s in store from Wealthfront in the coming year. Happy listening!

Over the years, we’ve heard from our founders here at Matrix that some of the best learning opportunities they’ve had has come from 1:1 conversations with other entrepreneurs. And while there is no shortage of resources for entrepreneurs (including content we have built at Viewpoints and forEntrepreneurs), there are very few public forums where successful founders and operators speak candidly about their career journeys and discuss what has/ has not worked for them as they’ve scaled their businesses.

That is why we are excited to announce ‘Focus on the Founder’ – a podcast series that will do exactly what it sounds like—bring the focus back on the founder. In the coming months, we will be releasing a series of episodes where we ask successful founders and operators questions about their journey into entrepreneurship, how they’ve gone about making critical decisions (e.g. hiring, fundraising, etc.) and what they would do differently looking back.

The initial focus will be on founders and senior execs in FinTech—though this may evolve over time. We will keep the episodes short, informal and frank. The very first episode is with Ryan Williams the CEO and co-founder of Cadre. You can find the podcast episode on SoundCloud, iTunes & Google Play.

In this episode you will learn about…

How Ryan went from selling headbands at age 13 to flipping houses in college to launching Cadre. Or as he puts it “Headbands to Houses to High Rises”

When the real “Aha” moment came for Ryan that led him to believe that there was a big opportunity in real estate technology

What Ryan believes is the single most important characteristic behind the success of companies like Amazon, Airbnb and Fidelity and how Cadre has embraced that characteristic

How Ryan works with his investors and the value they have provided to him beyond the obvious capital injection

The crucial metrics and KPIs that Cadre tracks and measures

What other areas Ryan is excited about and would explore if he were not building Cadre…hint some of them are pretty controversial in the venture world today

Earlier this week I attended Money2020 in Las Vegas. In just over 5 years, Money2020 has become the leading industry conference for everything to do with FinTech. It’s a jam-packed but valuable 4 days of expert panels, startup pitches, networking events and keynotes from industry leaders. I was there for just under 24 hours, which meant the experience was even more of a blur. This post is my attempt to capture twelve of the biggest learnings from the conference.

Lesson 1: Money is still the #1 biggest stressor for most Americans, understandably so. Dan Wernikoff from Intuit was one of the keynote speakers Tuesday morning and some of the data points he surfaced on consumer behaviors around money are sobering:

44% of Americans cannot come up with $400 for an emergency.

49% of Mint users spend more than they make.

Intuit customers on average paid $1,700 a year in interest.

Lesson 2: Most financial institutions are not adequately meeting the needs of their customers. Despite the potential opportunity created by the high stress around money, banks and other financial institutions really struggle to provide the experience their customers need. This is in part because most financial institutions are product centric not customer centric. The result has been notoriously low NPS scores and a disenchanted end user. Even more alarmingly, most customers of the leading banking brands distrust their banks:

Lesson 3: Among an already pretty unhappy customer base, millennials are the most disenfranchised of all. As Philippe Dintrans, Chief Digital Officer at Cognizant put it, most financial institutions are totally missing the mark with millennials. That is in part because millennials exhibit fundamentally different behaviors than earlier generations around things like savings. 63% of millennials are focused on saving towards desired life goals (e.g. getting out of student debt, purchasing a home, etc.) as compared to 45% of gen Xers and baby boomers. 55% of gen Xers and baby boomers are focused on developing savings towards retirement, where only 37% of millennials are planning for retirement

Lesson 4: FinTech startups have capitalized on the failures of incumbents by addressing specific pain-points with carefully designed products. The examples are smattered across financial services but a few examples that stand-out:

Wealth management was traditionally a confusing and fee-heavy landscape to navigate. Betterment created a beautiful and educational product that reduced fees and enabled a better user experience.

Peer-to-peer money transfers traditionally required a manual process that took days and trips to the bank. Venmo made it simple, quick and fun to do P2P payments.

SMBs used to have to use clunky check-out payment methods that locked them into a set location and required back-end processing to reconcile the books. Stripe enabled any merchant anywhere to accept payments with ease using an iPad.

Applying for, managing and refinancing loans was historically a painful process for most students. SoFi provided students with an easy way to apply for and refinance their loans all with the promise of a lower interest rate.

Lesson 5: Barriers to entry have never been lower to starting a FinTech business. It’s not just that the cost of starting a business in tech has been dramatically reduced (which has been well documented). In FinTech, there are also important industry-specific enablers allowing startups to enter and compete with the incumbents:

Insurgents don’t need a large balance sheet to open business. For example, marketplaces like LendingClub and Prosper connect borrowers and lenders without underwriting any of the loans.

Regulatory hurdles, for almost every sub-category within FinTech (with the exception of Blockchain / crypto assets), have been removed thanks to early pioneers like PayPal.

Platforms and developer tools like Stripe and Shopify have reduced development costs and time-to-market dramatically enabling SMB merchants to sell with the same ease as larger enterprises.

Lesson 6: Large and enduring companies have been and will continue to be built in FinTech. In two decades, PayPal, the “original” FinTech startup has reached a market cap of $84B. By comparison AMEX, which was founded a 167 years ago, has a market cap of $82B. Many more enduring companies will be built in FinTech in the years to come.

Lesson 7: There is no shortage of venture money. As of today there are 36 FinTech unicorns globally – that number represents 17% of the total share of unicorns. The venture market has realized the breadth of opportunity in FinTech and more money has poured into FinTech than ever before. In 2008, the number of FinTech companies funded was just over 200. In 2016, the number of FinTech companies receiving venture capital exceeded 5,000. In the same time period, venture funding from a dollar perspective climbed from <$1B to close to $60B.

Lesson 8: Great companies are being built across categories. With this increase in FinTech funding, great new companies are being built and entire sub-categories, from payments to insurance, are being served in new ways. Some of the really big winners of today either didn’t exist or were in their infancy 10 years ago. A few examples include publicly traded companies (LendingClub, Square, etc.), unicorns (Stripe, Sofi, GreenSky, CreditKarma, AvidXchange, Gusto, etc,) and several others that are well on their way (Betterment, Affirm, Plaid, etc.)

Lesson 9: Many think that the big area of opportunity for FinTech is in Blockchain/ crypto assets but that may not necessarily be true. Blockchain/ crypto assets are certainly getting all the attention right now but there are plenty of other areas that are just as interesting on both the B2C and B2B sides of the table. Some areas that are particularly exciting include:

Consumer: (1) personal financial management, (2) insurance, (3) real estate and (4) investing / wealth management

Lesson 10: Blockchain – lots of noise but few clear signals. Bitcoin today is trading at $5,500+ per coin and the total market cap of all cryptocurrencies is $170B. ICOs meanwhile have raised $8B in 2017 to-date. In the midst of this some things are clearer than others. What is clear today is that crypto assets have a definite use case as a store of value. What’s less clear is how we get from there to the end goal of software with no central operator, which is the big promise behind blockchain. The big advantage to blockchain, as Adam Ludwin from Chain put it, is “censorship resistance” (access is unfettered and transactions are unstoppable) but we have yet to see killer applications that can cannibalize existing practices.

Lesson 11: It’s not all about the U.S. ~1/3 of today’s FinTech unicorns are outside the U.S. (Asia + Europe). U.S. FinTech companies can likely learn a bit from their peers in other geographies. Behavioral and cultural differences certainly exist but there are a few clear examples of this that came up during one of the payment-focused panels. For example, in China, WeChat is using messaging capability to allow social payments. Stan Chudnovsky, the Head of Product for Facebook’s Messenger, revealed during one of the payments sessions that Facebook is developing this and expects it to be a key use case in the next 18-24 months. But in this space we are certainly followers not leaders.