Capital efficiency has long been a desirable trait in early/growth stage businesses. But over the last few years, an abundance of capital combined with a “growth at all cost” mindset, allowed founders to deprioritize efficiency. Ignoring efficiency, however, can lead to making cardinal mistakes like misreading true product-market-fit, over-hiring for the stage you are in and burning through too much money too quickly. Furthermore, growth rate and top-line progress are a function of how much capital a business has consumed to get to that point (i.e. getting to $10M in revenue is less impressive if you spent $50M to get there vs spending $5M to get there.)

In a post-covid world, capital efficiency has returned as king. This is especially true in SaaS (which, as a category, has outperformed almost every other category.) Many of the companies that have outperformed during this time frame have been very efficient businesses (e.g. Twilio, Zoom, Shopify, Datadog, etc.) As the fundraising markets dry up a bit and sales cycles lengthen, founders will increasingly be forced to think more about efficiency and investors will pay a premium for efficient businesses.

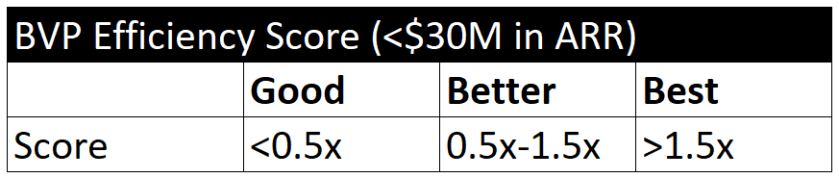

But how should SaaS founders think about efficiency? Several years ago, Bessemer put out a simple, but helpful rule-of-thumb called the BVP efficiency score. The efficiency score shows a “good-better-best” framework for thinking about capital efficiency (defined as Net New ARR / Net Burn.) They advised founders (under $30M ARR) to think about good-better-best using the table below:

While this is a great high-level framework, efficiency among SaaS businesses is a bit more nuanced depending on stage. In the formative days, finding product-market-fit can take time and money. In the early days of growth, building a scalable and repeatable playbook can require significant up-front investment. As the company moves into expansion-mode, the business benefits from clear economies of scale and an improved gtm playbook. In the later stages, the business should be humming and efficiency ought to be at an all-time high.

The point is: benchmarking efficiency in a meaningful way requires looking more closely at stage/ revenue profile. What we really need is an efficiency score for each stage. Or, put differently, a rubric showing how much capital ought to be consumed (and, yes, there is a difference between “raised” and “consumed”) to achieve various ARR milestones along the journey from $0M to $100M in ARR.

Below are two frameworks for founders to use to help answer this question. These tables were developed based on what I’ve seen in the field over the years and have been triangulated with what several other SaaS investors have also seen. The first table is simply a good-better-best framework for total capital consumed to get to different ARR thresholds. The second is a “stage-adjusted” efficiency score. These two tables are, of course, two sides of the same coin.

Bear in mind these are simple guidelines / “rules of thumb” and anecdotal in nature. Every business has its own set of nuances and unique circumstances. And there is definitely more variability earlier on depending on the nature of the product (i.e. some companies have to invest a lot more in R&D to get the product to market.) Where you land on the grid is less important than what the trend-line looks like and whether you have managed cash wisely (i.e. been a “good steward of capital.”)

To bring this to life a bit, here are a few “hall-of-fame” worthy examples of companies that scaled past 100M in ARR with record breaking efficiency. Note that we are listing capital raised here as a close proxy in the absence of public data on capital consumed:

- Veeva raised a total of $7M pre-IPO. Current market cap: $33B

- Appfolio raised a total of $30M pre-IPO. Current market cap: $5B

- Ringcentral raised a total of $44M pre-IPO. Current market cap: $24B

- Wix raised a total of $59M pre-IPO. Current market cap: $11B

- Salesforce raised a total of $65M pre-IPO. Current market cap: $162B

- Zendesk raised a total of $86M pre-IPO. Current market cap: $9B

- Realpage raised a total of $86M pre-IPO. Current market cap: $7B

It is no surprise that almost all of the above examples got going in the “good old days” of the 2000s, when capital was less plentiful, and efficiency much more in vogue. Much of this changed in the 2010s, but I suspect we will see the pendulum swing back to some degree in the decade ahead. Hopefully, this helps provide some useful data points in this return-to-efficiency world we now find ourselves in!

***

I’d like to thank Alex Kurland (@atkurland), Brian Murray (@murr), Chetan Puttagunta (@chetanp), Logan Barlett (@loganbartlett), Murat Bicer (@itsbeecher) and Parsa Saljoughian (@parsa_s) for their feedback and help in triangulating the numbers here.