**This post was originally published on the Oak HC/FT website here**

Last month, I joined Oak HC/FT’s San Francisco team. I could not be more excited to help identify and partner with the next generation of entrepreneurs in FinTech, building on Oak HC/FT’s strong legacy of investors and operators who have built enduring companies for decades.

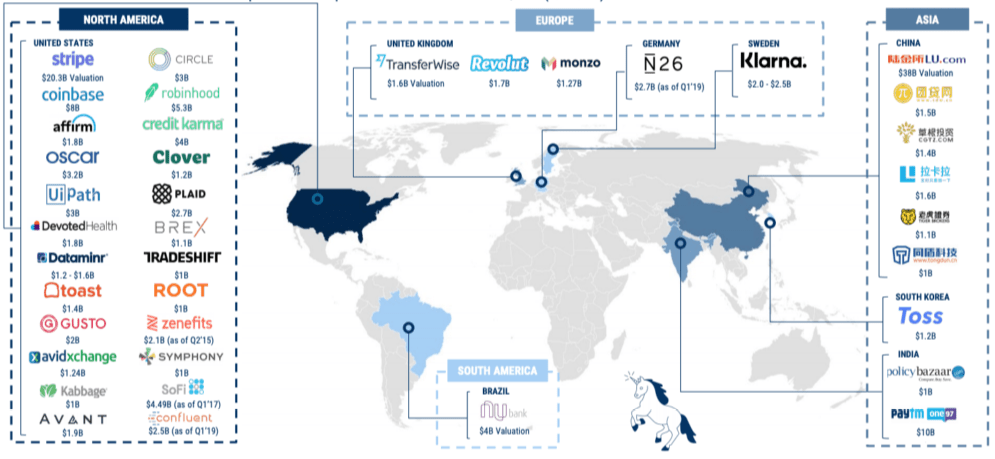

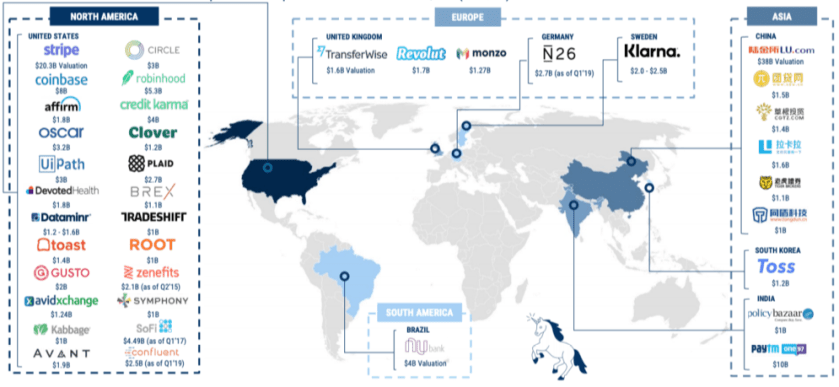

Over the course of the last ten years, FinTech has really begun to hit its stride. There are now nearly 40 FinTech unicorns globally (more than any other vertical) worth an aggregate value of nearly $150B. Not bad for a sector that didn’t have a ton of buzz when Oak first started investing in the space in 2002.

And this is just the beginning, there will be much more to come in the next 10 years. As I look to the next decade to come, I’m first and foremost eager to learn from the founders and entrepreneurs building at the fore-front of our industry. That said here are a few themes I have been thinking about deeply in recent months and am particularly excited about:

Vertical payments: We have already seen a few successful versions of this playbook including: Toast (restaurants), Flywire (travel & education) and PayIt (government.) But many more verticals could benefit from a bespoke, vertical-specific payments solution including pharma, logistics, manufacturing and more.

Next-generation commerce: Innovation in commerce in recent years has largely come in the form of new payments options (like Square, Affirm and Afterpay.) The next wave of innovation will enhance in-store commerce, logistics/ delivery/ returns, international commerce and buying via new mediums like voice, computer vision and mixed reality.

Intersection of FinTech + AI: Machine learning is already being used in financial services. Our portfolio company, Feedzai, uses machine learning to help banks and merchants fight fraud. In the years to come machine learning will stretch beyond risk and into underwriting, product discovery, predictive intelligence and a number of other use cases.

Middleware tools for developers: Stripe and Plaid have shown us that developers are the next big consumers of financial data and they require tools to access and use that data: be it payments meta-data, account information or piping infrastructure to connect with other financial institutions. As microservices and APIs continue to proliferate, developers will require more tooling to serve end customers.

Banking Applications: Many financial services incumbents suffer from manual-heavy tasks for workflows that have struggled to make the transition to digital. Our portfolio companies Kryon (robotic process automation) and Ocrolus (digitizing financial documents) are two examples of the new wave of companies focused on automation, software-enabled workflows and refined banking applications.

Back-office application software for SMBs: The software stack for most functions (e.g. marketing, sales, customer support, etc.) within an SMB certainly looks a lot better than it did 5 years ago when Oak first invested in Freshbooks. But the finance and accounting functions remain underserved. As SMBs demand better software for their back offices, new entrants will rise to the occasion, providing these businesses with a better way to close their books, pay their vendors and manage payroll.

Financial services for the underserved: Banking services have improved for many of us but there remain many demographics that are underserved. Oak has a history of investing in this category, dating back to NetSpend, which went public in 2010. I’m excited to see founders focus more on low-income Americans, immigrants, freelancers/1099s, older (and younger) generations, those with large sums of student debt, etc.

Future of real estate: Almost everything about commercial and residential real estate stands to be improved for both buyers and sellers. Moreover, the ecosystem players around them (e.g. brokers, agents, lenders, inspectors, etc.) are still mid-transition to cloud-based tools. New entrants in real estate will find ways to improve workflows for these ecosystem players or generate more economic value for buyers and sellers.

If any of this resonates with you, let’s get in touch. I’m focused on opportunities on the west coast (and that certainly includes more than just the Bay Area!) But even if you are outside the west coast, I still want to hear from you. Looking forward to finding ways to collaborate!