It’s been a few years since I’ve written extensively about education technology and the opportunities that exist in the space. Since my last set of posts back in December of 2012, the space has continued to be a fast growing sector with much opportunity. Back in 2012, the sector was a $4.1T industry globally. That number just topped $5T in 2015 with a 7% CAGR. Unsurprisingly, the education sector remains the second largest industry, trailing only healthcare in terms of global market size.

Likewise, venture capital investment has picked up substantially in the last 3 years. In 2012, Series B investments totaled just $159M—that number is expected to top $500M in 2015 once the final numbers are published. Similarly, deal activity across all stages has picked up. In 2012, the total number of deals across VC/PE was ~500 deals—that number will reach nearly 800 deals by end of year 2015.

Most importantly, exits have finally begun to provide some hope for returns. A scarcity of exits has long been one of the big problems for entrepreneurs and investors considering EdTech. Indeed M&A activity has historically been slow (<1% of all M&A exits from 2002-2012) and IPO showings have often been abysmal (e.g. Chegg which fell 23% during its IPO debut and now has a market cap of just ~$620M, half of its opening day valuation.)

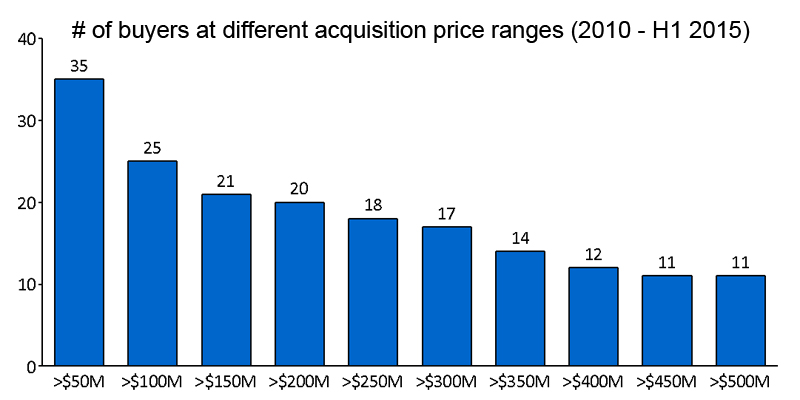

In the last three years, however, there have been a handful of successful EdTech IPOs including companies like 2U and Instructure. Others, such as Coursera, Udacity and Edmodo, are all not far behind in the IPO pipeline. M&A activity likewise has been quite strong. In fact, U.S. EdTech companies tend to command higher revenue multiples than the average tech exit—3.2x for EdTech companies vs. 2.5x for the broader tech industry. Furthermore, M&A exits themselves over the last 5 years have been fruitful with 25 buyers spending more than $100M on U.S. EdTech companies.

Source: EdSurge

Source: EdSurge

Yet despite this progress, there remain a wide array of inefficiencies and unsolved problems. Specifically, I see 6 promising near-term opportunities for entrepreneurs to take advantage of and for investors to invest in. In no particular order here are a few thoughts of what we will see beginning in 2016.

1) Cloud SaaS will finally replace on-prem at the school district and system admin level

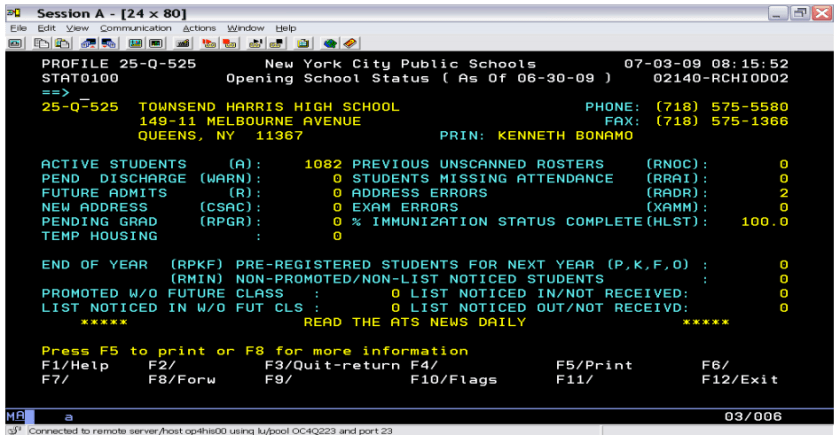

Having spent time working at the district level in education policy, I was always amazed at how archaic many of the tools districts and school systems use at the city-wide/admin level. Software tools that track important mission-critical information such as attendance, student demographics, building information, zone data, etc. across schools within a district are still often hosted on-premise, using archaic databases and outdated software with GUIs that look like they were designed in the ‘90s. Below is an example of what the NYC DOE ATS currently looks like:

Source: NYC Department of Education

Source: NYC Department of Education

I suspect that in 2016, as much of the IaaS and PaaS layers begin/complete their moves to the cloud through services provided by the likes of AWS, Azure, SoftLayer, etc, we will begin to see more B2B SaaS applications layered on top to replace the traditional on-prem software solutions. This will bring much needed functionality, analytics and a cleaner user experience to the education world. This in turn will increase productivity for educators working at the district and administrative level across school systems.

2) Learning content will be far more personalized

Recent survey data showed that less than 50% of teachers reported having digital resources that could be used to meet teaching standards. Moreover existing technology solutions often are not tailored to individual students and their specific needs. The next generation of student-centric software tools (across grade levels and subjects) will provide high levels of granularity and insight into the specific needs of individual students allowing for an end-to-end customized experience across lesson planning/ delivery, class activities and periodic assessments. This will be even more important for special needs students in ICT, 12/6:1 or similar learning environments. Personalizing learning content will ultimately allow for a more tailored learning experience and better long-term knowledge retention.

3) K-12 teacher development will rely more heavily on software platforms and tools

As it stands today, professional development for teachers is largely untouched by software tools and applications. At the district level, spend on professional development for K-12 teachers in the U.S. is ~$3B and usually takes 1 of 4 forms: (1) periodic school-wide workshops, (2) observation of other teachers, (3) coaching (usually by a more experienced teacher) and (4) generic online research.

In 2016, we will begin to see more PD content move to the cloud as doing so makes training teachers: (a) less expensive, (b) more accessible and (c) more personalized. Horizontal HR solutions like Workday, Cornerstone OnDemand and PeopleSoft will be re-built / tailored for the education sector enabling professional development in education to be more sophisticated and effective.

4) Higher education software tools will focus more on degree completion

As the Baby boomer generations’ offspring (Gen X) move beyond the college-age window, the college enrollment growth rate will begin to slow and the focus for many higher-education institutions, from a revenue perspective, will shift away from recruitment/ matriculation and towards retention/ graduation. As of 2012, ~50% of all college students were in at least 1 remediation course.

In the years ahead, there will be a greater focus on retention and remediation of students already admitted into colleges. Software tools will increasingly be used for (1) recruiting the right type of student to admit, (2) providing BI and predictive analytics platforms for identifying and tracking high at-risk students and (3) supporting remediation instruction for at-risk students to get them back “on track.”

5) Online courses and degrees will become more relevant

While online courses (including MOOCs) and degree programs will never replace the off-line experience, these offerings will increasingly be used to supplement off-line instruction as well as provide a new delivery format to non-traditional segments (such as continuing education students). Two important trends are happening that will accelerate the pace at which this happens in 2016: (1) online courses and degrees are becoming more socially acceptable (many programs have been accredited, employers are increasingly hiring graduates from these programs, etc.) and (2) the infrastructure (managing enrollment, handling payment, providing tech support, hosting platforms, etc.) to provide these offerings is cheaper and more readily available.

As such, we will see a greater number of higher education institutions join the ranks of UNC, USC, ASU and many others that provide courses and degrees online. This trend will create a range of software opportunities across: video collaboration, course development and delivery, student / faculty services and recruitment / retention.

6) Demand for software tools that teach skill-based training will increase

As colleges increasingly charge exorbitant tuition fees while failing to equip graduates will real skills, demand for skill-based programs, vocational certifications and other alternative teaching tools will increase. In 2013, the number of vocational certificates granted was nearly 1M—up 35% from 2005. Similarly, from 2013 to 2015, the number of graduates who graduated from coding programs (such as Codecademy) increased 630%+.

In 2016, we will see an even greater emphasis on tools for skill-based training. Some of this will be purely software delivered via the cloud and some will be more hybrid: software mixed with in-person training. Companies like Lynda (acquired by LinkedIn), Udacity, General Assembly and Udemy have already made significant dents in this space. We will see much more of this in the upcoming year.