Towards the end of 2017, we discussed the rise of the FinTechs and briefly alluded to payments as being a key area for further innovation. The payments ecosystem is an ever-evolving space froth with opportunity and plenty of buyers with deep pockets (see Paypal’s announcement a few weeks back). Furthermore, it is a deeply intricate ecosystem with challenging technical problems, shifting regulatory components and a variety of consumer and enterprise use cases. For all these reasons, it is worth a “double click” to explore further.

We have already seen huge amounts of innovation in payments over the last few decades. In the U.S., this innovation was enabled by a few important advances. The establishment (and operation) of ACH by the Federal Reserve Banks and EPN created a much needed electronic network for financial transactions. NFC technology and POS hardware enabled mobile payments. More recently, pay-out APIs and fraud management systems have allowed developers and those working in risk to manage feature build-out while also keeping an eye out for bad actors. And we are just beginning to see some applications of crypto in the payments space — such as this.

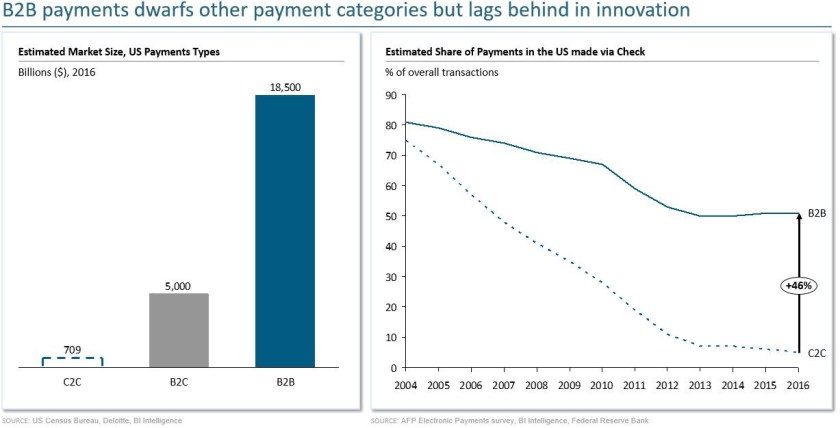

Despite these advances, most of the innovation has been focused on two areas: consumer-to-consumer payments (e.g. Venmo), business-to-consumer payments (e.g. Square) or new entrants that facilitate one of the two (e.g. Stripe). A third category, business-to-business payments, has not benefited from innovation to the same degree as the other two categories. This is particularly interesting given that the market size of B2B payments is 5–10x that of C2C or B2C payments. And yet, technology has been slower to transform the B2B payments world. Case in point, B2B payments made by the good ol’ check, as a share of overall transactions, leveled off around 2013 at a point significantly higher than C2C and have actually gone up slightly to ~51%.

Existing Challenges

In the early days of C2C and B2C payments, there were many intricacies from a technical and regulatory perspective that had to be navigated very carefully. After all, real consumer money was at play so the stakes were high. The same is true in the B2B world, with a few additional challenges that make things even more hairy:

- Transaction values are significantly higher: While the volume of B2B payments is much lower (some say in the 9:1 range compared to B2B + C2C), the value of these payments per transaction is much larger. This makes enterprise transactions prime targets for hackers, front-runners and a host of others with bad intentions. Beyond the actual financial risk, enterprises also risk having the banking information of their suppliers and customers exposed.

- There is greater complexity: In the enterprise payments context there is significantly more complexity. Let’s take the simple example of someone in procurement trying to pay a supplier. Post RFP, legal review, etc., the buyer will need to first work with the various business units and other internal stakeholder to issue a purchase order. The supplier must do the same in order to provide an invoice to the buyer. The buyer must then send a request to the card issuing bank (via p-card or some other mechanism.) The buyer’s bank must then handle settlement with the supplier’s bank. This may happen via check, credit, debit, ACH or even cash. Post-settlement, the buyer and seller must ensure that both their internal financial systems and/or ERP systems are accurately updated. Imagine the complexity involved when doing this hundreds or thousands of times per day across many different payment types (one-off, recurring, up-for renewal, etc.)

- Many people are involved with any given transaction: As a result of the greater complexity, many heads are involved on both sides of the transaction. Procurement, legal, finance and the BU may all be involved at various stages. B2B payments affect the workflows of a much broader set of people than C2C or B2C payments.

- The life cycle of a payment is longer: As a result of the added complexity and multiple stakeholders, the duration of the payment is longer than in the C2C and B2C contexts. C2C payments in today’s world can clear in a matter of minutes. On the enterprise side, the payment life-cycle can have a duration of 60, 90 or even 180 days.

- The life cycle of a payment is longer: As a result of the added complexity and multiple stakeholders, the duration of the payment is longer than in the C2C and B2C contexts. C2C payments in today’s world can clear in a matter of minutes. On the enterprise side, the payment life-cycle can have a duration of 60, 90 or even 180 days.

- The U.S. is not well structured for top-down fixes to B2B payments: When Europe moved to the Euro, all the participating countries did a significant overhaul of their banking systems allowing them to make significant upgrades to the tech stack. In the process, they solved a number of the pain points above (including significant reduction/ elimination of checks). But in the U.S., the Fed does not have the authority to mandate unified standards. Lack of standardization is particularly tough in the U.S. as we have many more banks than Europe (including regional and community players) — creating a major interoperability problem with few bank-agnostic solutions. Meanwhile, the U.S. banks themselves have made little attempt to create a common solution to fix the antiquated system.

Key Opportunities

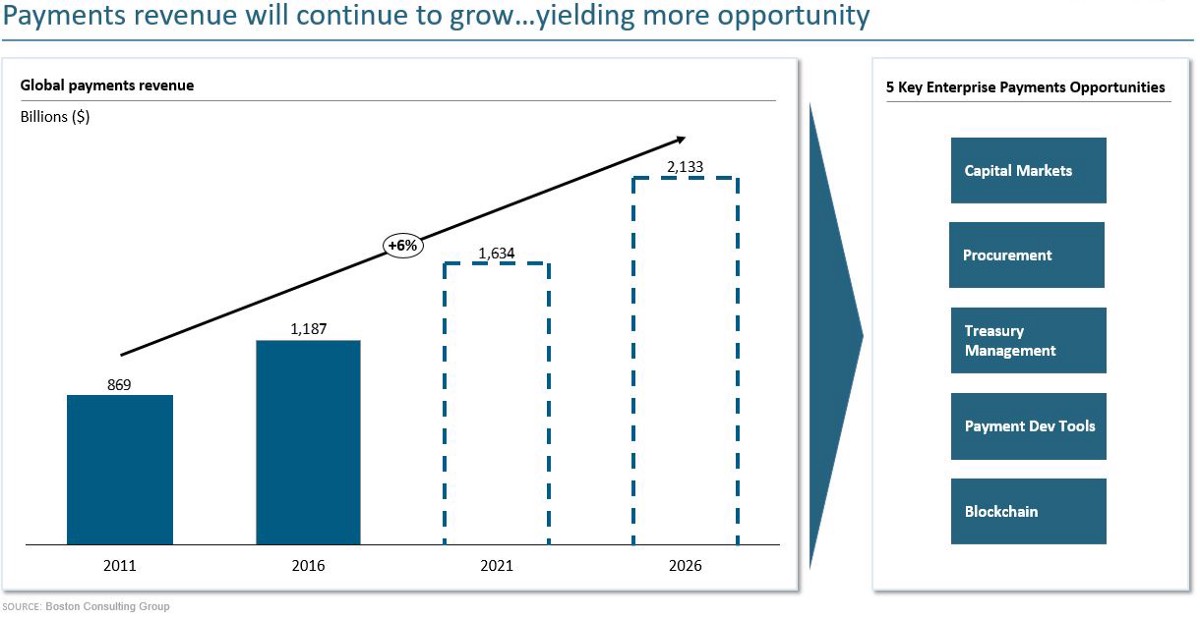

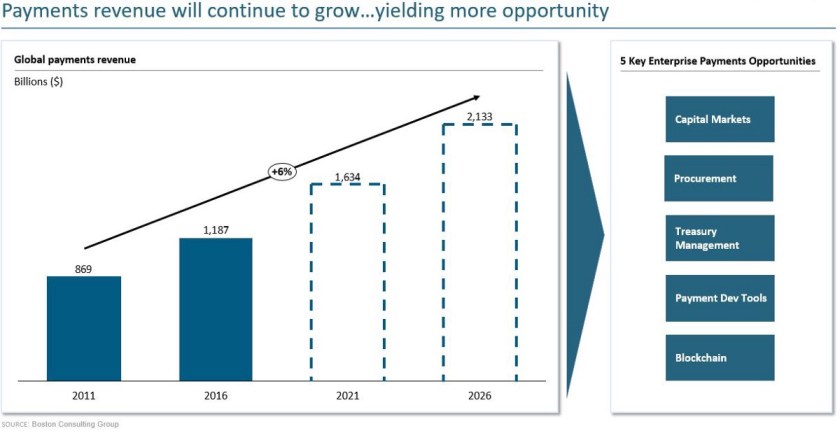

While these challenges are daunting (they most certainly are not for the faint of heart!), the good news for new entrants is that the banks and other FIs are unlikely to be the ones to fix enterprise payments. We believe FinTech startups are best positioned to make progress here, bottoms-up. More specifically, there is an enormous opportunity to capture value in enterprise payments($2.1T in payment revenue by 2026) across 5 specific subcategories: (1) capital markets, (2) procurement, (3) treasury management, (4) payment dev-tools and (5) blockchain.

- Capital Markets: Many parts of capital markets (e.g. HFT, commercial lending, etc.) send/receive very large transactions each day. Most of the time these payments are slow, expensive and require manual reviews to ensure they are valid. In the HFT world, for example, every minute matters when making a trade and fees add up. Payments solutions that focus on speed and automation, without sacrificing security will do well here.

- Procurement: In procurement, enterprises and their suppliers face the problem of trying to integrate procurement software tools, with ERP systems and antiquated payment processes. This problem is particularly challenging with services and in the “long-tail” spend, where some enterprises have to pay tens of thousands of suppliers each year. Solutions that integrate with existing software solutions, simplify the enterprise’s workflow and get the money to the supplier faster (e.g. lower DSO) will have the most success here.

- Treasury Management: Initiating and managing ACH payments to other businesses, auditing those payments and then closing the books at the end of the month is still not straightforward. Software tools that provide solutions for both the finance and the tech team to navigate this process have a shot at building a must-have for anyone trying to get a grip on treasury management. Particularly for SMBs who don’t have the luxury of simply throwing more people at the problem.

- Payment Dev Tools: Companies like Stripe and Plaid have created great APIs and financial plumbing tools. But they are largely focused on C2C and B2C payments. B2B developer tools / APIs that work for the IT and risk departments of enterprises and address the complexity therein will do well. Certainly a hairy problem to figure out but there is a lot of spend here for the right solution.

- Blockchain: In the short run, blockchains have enough technical issues (e.g. scaling, interoperability, etc.) to work through. But in the long-run distributed ledger technology can provide a single database of truth between two enterprises, eliminating the need for ledgers on both sides and making verification/ security a bit more manageable. The real question from a B2B payments perspective is not “if” but “when.”

At Matrix Partners we are deeply interested in backing the next generation of enterprise payments companies. We focus primarily on Seed/ Series A investing here in the U.S. Please let us know if you are building something interesting here — would be great to meet up and learn more!